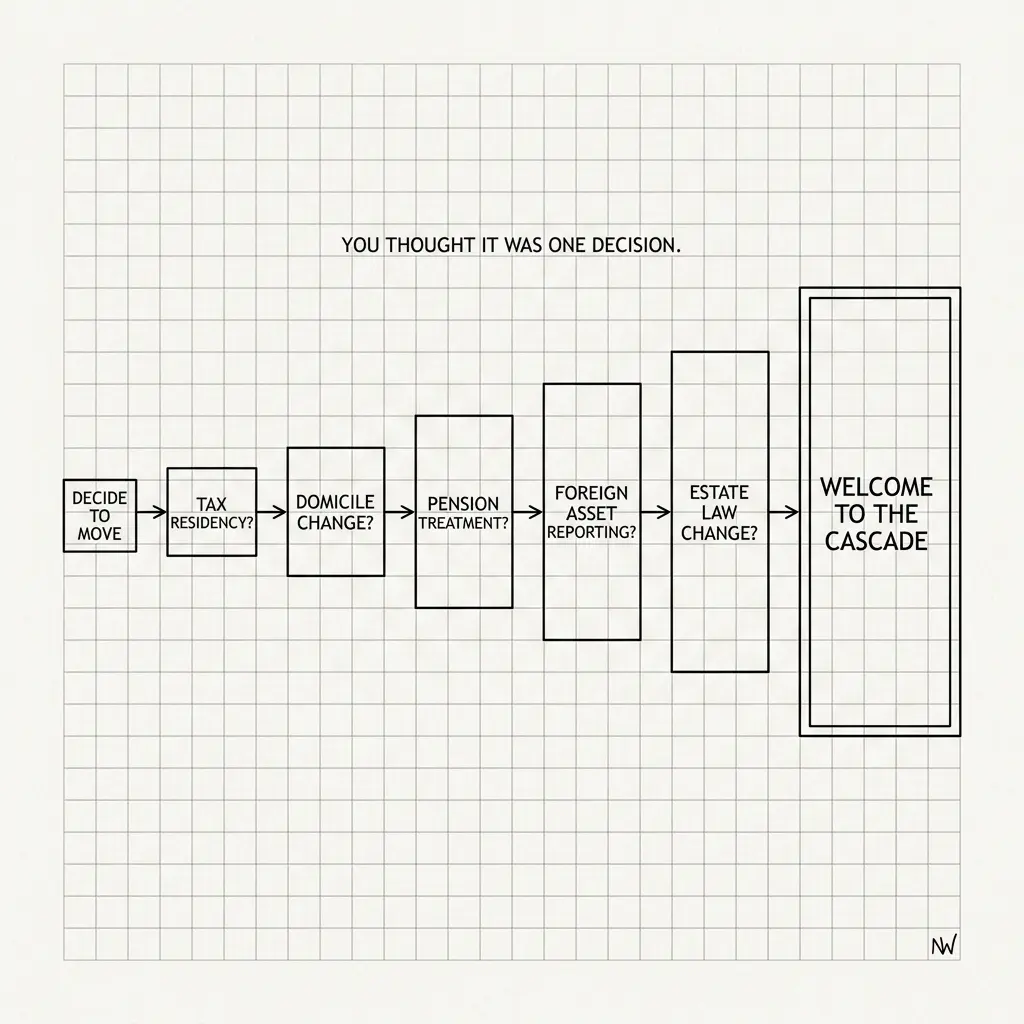

You left the US. The tax bill didn't. Neither did the rules.

The US taxes citizens and green card holders on worldwide income regardless of where they live. Your brokerage may restrict non-US residents. Your ISA, TFSA, or foreign funds may create PFIC issues. Your foreign pension, FBAR, FATCA, RSUs, estate plan, and possible exit tax exposure all need to be seen together.

✓US brokerage restrictions, foreign pension balances, and local accounts consolidated in one base currency

✓FBAR, FATCA Form 8938, PFIC, ISA/TFSA, and estate planning exposure flagged before filing season

✓401K, RSU sourcing, foreign tax credits, exit tax risk, and treaty questions modeled in one picture

Your Cross-Border Financial Picture

4 minutes. Your full picture across every country. No advisor who only knows one side.

15-day trial · No card required

You're probably in one of these situations

In the UK

Your US brokerage is still open. Your Stocks and Shares ISA gains are US-taxable — the IRS doesn't recognize the ISA wrapper. Your SIPP has treaty questions nobody has resolved. And you still file a US return every April.

In Singapore

There is no US-Singapore income tax treaty. FEIE can shelter your salary but not your RSU income from a US employer. CPF contributions don't help your US tax picture. You're paying more US tax than you expected.

In the UAE

The UAE has no income tax. The US taxes you anyway. Zero foreign tax means zero foreign tax credit to offset your US liability. Every dollar of income above the FEIE exclusion is fully exposed to US rates.

In the Netherlands, Germany, or Canada

The 30% ruling reduces Dutch tax — not US tax. German tax rates are high but the treaty interaction with your 401K isn't as clean as you think. In Canada, the TFSA you heard about will create a US reporting problem.

If any of these are you, this was built for your situation specifically.

$132,900

Foreign Earned Income Exclusion for 2026 — shelters salary abroad, not RSU income or investment gains

IRS Rev. Proc. 2025-28

$10,000

FBAR aggregate threshold — applies to US citizens abroad, same as US residents. One account or twenty.

FinCEN / 31 USC 5314

9M+

Americans living abroad who remain subject to US worldwide income taxation regardless of residence

Yes. The US taxes citizens and green card holders on worldwide income regardless of where they live — this is almost unique globally. The Foreign Earned Income Exclusion (FEIE) can shelter up to $132,900 of foreign earned income in 2026, but this does not cover RSU income from a US employer, investment income, or rental income. The Foreign Tax Credit is the alternative: instead of excluding income, you credit taxes paid to a foreign government against your US liability. Which approach is better depends on your income mix, country of residence, and whether you hold equity compensation.

Do I still need to file FBAR if I'm living abroad?

Yes. FBAR (FinCEN Form 114) is a US person obligation, not a US resident obligation. If you are a US citizen or green card holder with foreign financial accounts whose aggregate value exceeds $10,000 at any point during the year — including accounts in your country of residence — FBAR is required by April 15 (automatically extended to October 15). The penalty for non-willful failure is up to $10,000 per account per year. Accounts include: bank accounts, brokerage accounts, pension plans in some cases, and any account where you have signature authority.

What should I do with my 401K while living abroad?

Generally: keep it open, keep it in US-domiciled investments, and do not try to roll it into a local pension. No other country accepts 401K rollovers — the transfer would be treated as a taxable distribution by the IRS. 401K earnings continue to grow tax-deferred regardless of where you live. Distributions are taxable in the US. Whether your country of residence also taxes the distributions depends on the relevant tax treaty — the US-UK, US-Canada, and US-Germany treaties each have pension provisions; the US has no income tax treaty with Singapore or the UAE.

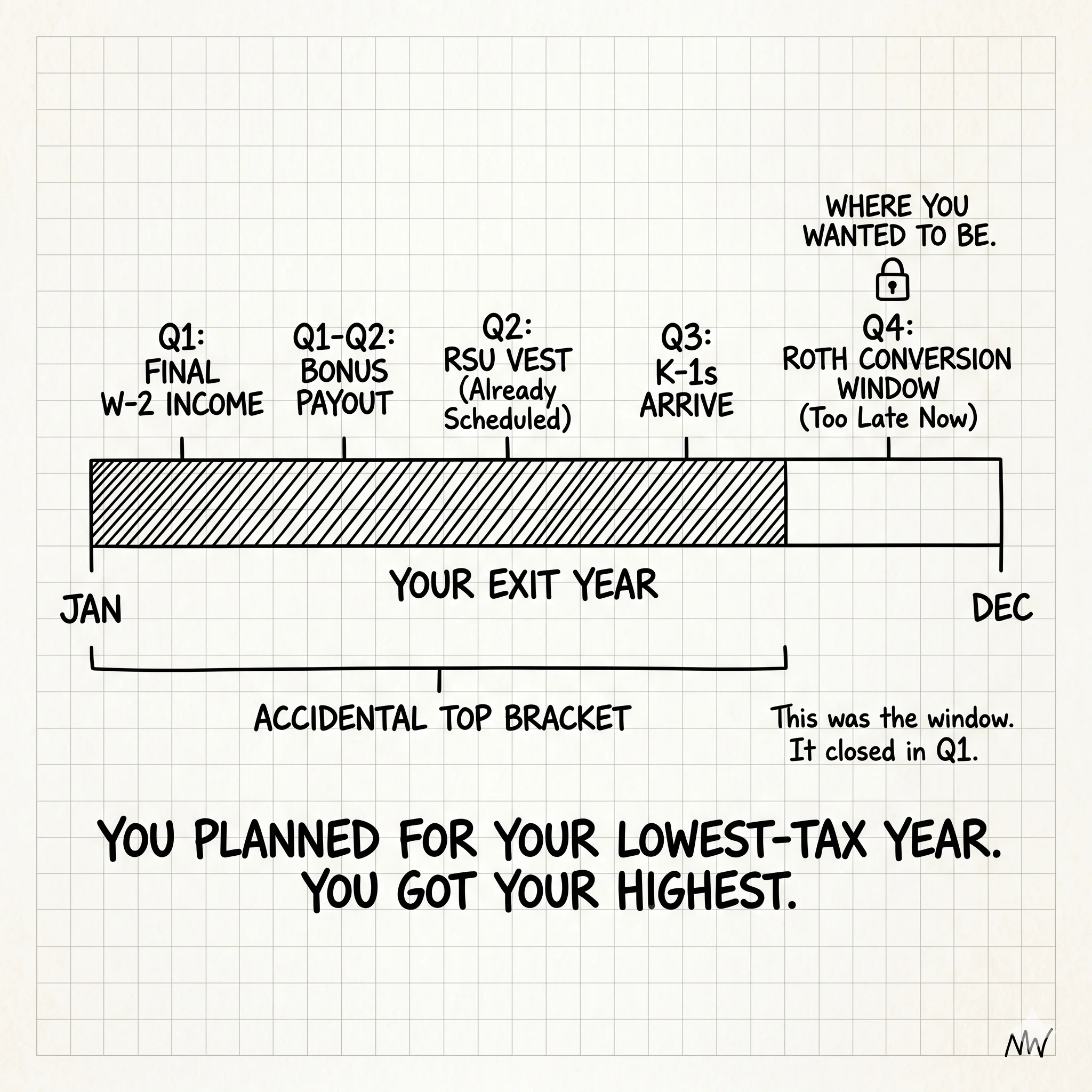

How are my RSUs taxed when they vest while I'm living abroad?

RSUs from a US employer that vest while you live abroad are subject to 'sourcing allocation' — the US taxes the portion of the vesting gain corresponding to workdays spent in the US during the vesting period. Your country of residence may also tax the same vest event. The US-UK treaty (Article 14) and US-Netherlands treaty have specific allocation rules; the US has no income tax treaty with Singapore or the UAE, so those residents face US tax at their full marginal rate on the US-sourced portion with limited ability to avoid double taxation. The practical implication: do not assume 'I'm abroad so the US won't tax this vest.' They will.

Is my UK ISA taxable in the US? What about a SIPP?

Yes — a Stocks and Shares ISA is not recognized by the IRS. The ISA tax-free wrapper exists under UK law; the IRS does not honor it. Gains inside an ISA are US-taxable as ordinary income (not capital gains), reported annually. UK SIPPs may be treated as pensions under the US-UK treaty (Article 17), potentially providing some tax deferral for US purposes — but this depends on the SIPP structure and whether the treaty pension provisions apply. Many US-UK dual-filers hold both an ISA and a SIPP without realizing the ISA creates annual US income and the SIPP requires careful treaty analysis. Both count toward FBAR reporting thresholds.

Your data stays yours. We help you make sense of it.

4 minutes. Your full US and international picture. 15-day trial, no card required.