Cross-Border Job Move: Tax Planning for Expat Equity

Quick Answer

When you move across borders, your tax residency changes. Your equity compensation treatment changes. Your retirement account access rules change. Your filing obligations multiply. Most people don't realize these complications exist until they're already in them. For a tech exec moving from China to Hong Kong (or any similar cross-border move), the first year can surface $20,000–$100,000 in missed tax refunds, double taxation, and planning mistakes simply because nobody warned you that the rule changed on Day 1 of your move.

The tax year doesn't match the calendar year. Nobody tells you that until the tax bill arrives.

A friend accepted a role in Hong Kong. Same company, same responsibilities, different office. Simple move. Straightforward opportunity. He'd been in Beijing for three years. Time for a change.

His company's HR didn't brief him on tax residency. His tax accountant back in the US didn't mention it. He assumed taxes would work the same way, just with a different country.

On August 15th, he moved. New apartment. New office. New visa.

By April (next calendar year), he had a discovery: He owed taxes to two jurisdictions for the same income. He'd missed a refund window. His equity compensation treatment had changed retroactively. And because the Hong Kong tax year runs on a different calendar than the US tax year, the math was a nightmare.

A move that looked simple on the org chart turned into a three-year tax puzzle that cost him more than the salary difference.

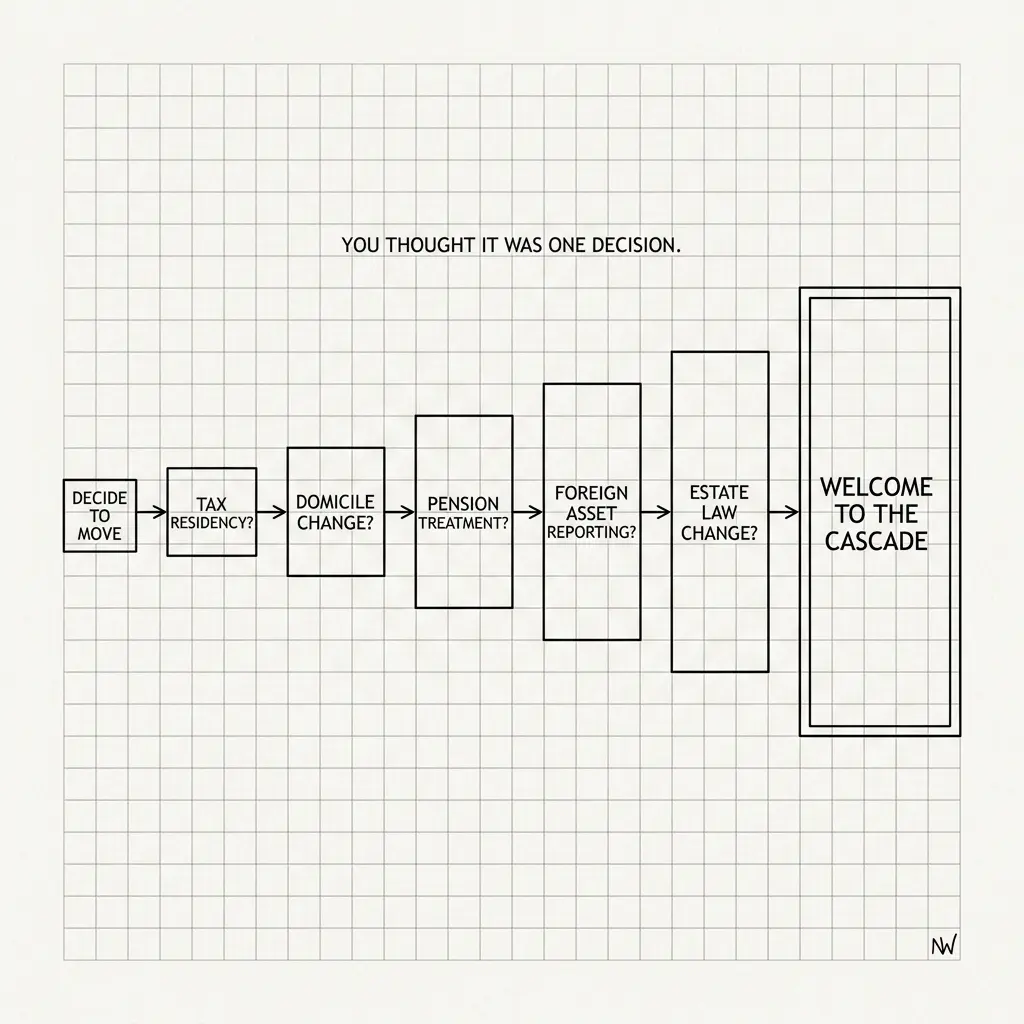

The Cascade of Complications

Here's what changes when you cross a border with equity compensation:

Tax Year Mismatch

Beijing: Calendar year (Jan 1 – Dec 31) for tax purposes. Hong Kong: Fiscal year (April 1 – March 31). If you move in August, you're now in two tax years simultaneously: one partial year in Beijing, one partial year in Hong Kong, plus ongoing US filing obligations if you're a US citizen.

The problem: Your income doesn't align. Your equity vesting is on the calendar year. Your Hong Kong taxes are on the fiscal year. Your US taxes are on the calendar year. Same equity event. Three different tax years.

Tax Residency Determination (the invisible line)

Tax residency status changes your effective tax rate and your filing obligations. In Hong Kong, you become a tax resident if you spend 180 days in the jurisdiction during the tax year. In mainland China, it's 183 days or "economic interest" tests. These are different thresholds with different clocks.

The problem: You might be a non-resident in Hong Kong for tax purposes in Year 1 (if you didn't spend enough days there), but a full resident in Year 2. Your tax treatment flips. Nobody warns you about this in advance.

Equity Compensation Tax Treatment Change

Hong Kong has favorable tax treatment for equity compensation. RSUs are taxed on vesting in both jurisdictions, but Hong Kong offers relief for "Approved Share Schemes"—if your company qualifies. The US has Section 83(b) elections that don't translate to Hong Kong.

The problem: Your March vesting event was taxed under Beijing rules. Your April vesting event is taxed under Hong Kong rules. Same equity instrument. Different tax treatment. Nobody connected those dots for you.

Treaty Interaction (if applicable)

The US has tax treaties with many countries. But they don't cover everything. Capital gains treatment varies. Employee stock purchase plans don't have consistent treatment. Some equity instruments get tax relief; others don't.

The problem: You need to file foreign earned income exclusion (FEIE) forms if you qualify. Or file as a foreign tax credit candidate. Or file under treaty provisions. Each path leads to different tax outcomes. You pick wrong once, and you've committed to that path for three years (the amendment statute of limitations).

Refund Windows That Close Quietly

China has a refund window if you've been over-withheld. Hong Kong has a similar window. But they run on different calendars. You have until December 31st in China to claim a 2025 refund. You have until November 30th (fiscal year ending March 31) in Hong Kong. If you file wrong in one jurisdiction, you miss the refund window in the other.

The problem: My friend filed the Hong Kong refund too late because he was waiting to see his full US tax picture. By then, the Beijing refund window had already closed.

The Specific Mistake

Here's what happened to my friend:

Year 1 (the move year)

August 15: Moves to Hong Kong. W-2 income continues. RSU vesting is daily. He's withholding taxes to his Beijing employer at the Beijing rate.

December: His accountant says, "You're probably going to owe more in total taxes because Hong Kong tax is complicated." True, but unhelpful.

Action: He does nothing. Waits to see the full picture.

Year 2 (the reckoning)

April (Hong Kong fiscal year end): His Hong Kong accountant tells him he's owed a refund—but only if he files by May 15th (the Hong Kong deadline).

May: He's still working with his Beijing accountant on the Beijing refund, which requires knowing his US tax situation. By the time they coordinate, the Hong Kong filing deadline has passed.

December: His Beijing accountant finally files the Beijing return, claiming a refund. But the Beijing refund was due by December 31st of the *following year* of earnings—and my friend has already moved to Hong Kong. The Beijing office can't easily amend the claim after the fact.

Outcome: He misses both refunds. ~$28,000 in missed returns.

The downstream effect

Because he didn't file the Hong Kong return correctly (and missed the deadline), he also didn't claim the "Approved Share Scheme" relief for his equity. That means his RSUs in Year 2 were taxed at the full rate instead of the preferential rate. Additional tax: ~$12,000.

Because the filing was late, he also couldn't amend it to claim relief retroactively. He's locked into the higher rate.

Total cost of the cross-border complication: ~$40,000 in the first year. Plus ongoing complexity for five more years.

None of this was obvious until after he'd already moved.

What's Actually Happening

The cross-border tax system isn't designed for people. It's designed for governments that want to collect tax from every angle:

- Worldwide taxation: The US taxes its citizens on worldwide income, regardless of residency. So you're filing US returns even though you live in Hong Kong.

- Residency-based taxation: Hong Kong taxes residents on Hong Kong-source income (mostly). So you're filing Hong Kong returns based on where you live.

- Source-based taxation: Beijing taxes people on China-source income. So you're filing a final return in Beijing to wrap up your prior residency.

- Different year definitions: Each jurisdiction has a different tax year, so the same income gets reported in different years to different countries.

This creates a mathematical nightmare: The same dollar of compensation gets reported in three countries, in three different years, under three different rules. The tax systems expect you to figure out the overlaps and claim relief manually (through foreign tax credits or exclusions).

What Most People Get Wrong

People think cross-border taxation is about understanding one rule better. They hire an "international tax specialist" and hope that person coordinates across jurisdictions.

The actual problem is that cross-border taxation isn't a single rule. It's the *interaction* of three separate rule systems with different calendars, different definitions of residency, different treatment of the same instrument. You need someone who understands all three *and* the interaction effects. Most tax specialists understand one jurisdiction deeply and the others superficially.

The Questions That Matter

If you're considering a cross-border role, does anyone have a checklist?

Not a vague "taxes are complicated" warning. A specific list: tax residency implications, equity treatment changes, refund deadlines, filing obligations, treaty considerations. If your company's HR can't provide this, you need an advisor who can.

Have you mapped out your tax calendar for the next three years?

Not just "I'll file taxes in April." Calendar year vs. fiscal year differences. Refund windows. Deadlines for elections or amendments. If you can't draw a timeline showing when each jurisdiction's deadline hits, you're operating blind.

Does your tax advisor specialize in the specific jurisdictions you're moving between?

An accountant who handles "international taxes" but specializes in UK-to-US moves won't be useful if you're moving from China to Hong Kong. Specialization matters.

If you move, who owns the problem of coordinating between your old accountant and your new one?

Most people assume "I'll switch accountants." But your old jurisdiction still needs a return filed. Those two accountants need to coordinate on the same income. If nobody owns that handoff, money falls through the cracks.

The Path Forward

If you're considering a cross-border move, you need planning *before* the move happens, not after:

1. Tax Calendar Mapping

Create a timeline for the next 24 months showing: tax residency status determination dates, refund deadlines, filing deadlines, decision windows for elections/amendments. See the overlaps before they hurt you.

2. Equity Treatment Pre-Analysis

Understand how your specific equity instruments (RSUs, ISOs, NSOs, QSBS) are taxed in your current jurisdiction vs. your destination. Some are more portable than others. Some create traps based on when you move.

3. Accountant Coordination

Before you move, introduce your old accountant to your new one. Make sure they agree on how to handle the transition year. Make someone explicitly responsible for the handoff.

4. Move Timing Optimization

Some moves are better mid-year than others. Some moves trigger early refund opportunities. Timing your move relative to vesting schedules and refund windows can save thousands.

The cross-border moment isn't just a career move. It's a tax structure change. Treat it like one.

The difference between a smooth transition and a $40K surprise is whether you understand the tax calendar *before* you move.

Most people learn this lesson after they've already moved. You can learn it before.

The opportunity in a cross-border role is real. The financial complications are real too. You need to know both before you sign.

A great move can look like a disaster if you don't see the tax structure underneath.

For US persons moving to specific destinations, the corridor-specific guides cover the hard deadlines before departure: leaving the US for Singapore, leaving the US for UAE, leaving the US for the UK. Each corridor has different treaty protections (or lack thereof), different FEIE and FTC dynamics, and different equity treatment rules.

If you're considering a role in a different country with equity compensation—

The tax implications are hiding in the details. You need to surface them before you move.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

The 15-Year Tax Setup I Wish Someone Had Told Me

Rohit pulled up his 2009 W-2 not to look at the number — to look at the decisions he hadn't made yet. Wrong account type. Wrong entity structure. Wrong equity exercise timing. None of it was illegal. All of it was expensive. And none of it was fixable once the window closed.

The Transition Year Tax Map: Planning for the Income Gap

The first 12 months post-exit are a tax minefield. Sequence your income, deductions, and Roth conversions to avoid the 'Success Tax' that burns 10-20% of your final payouts.

Liquidity Event Sequencing: Pre-Exit Tax Planning for Founders

Real exit tax savings (15-25% of proceeds) come from decisions 12-18 months before close. Master charitable structures, entity optimization, QSBS timing, and option planning.