Leaving the US for the UK: The Financial Decisions That Have Hard Deadlines Before Your Flight

Olivia had planned the move to London for four months. She'd sorted the visa, the flat, her child's school enrollment, and the health insurance gap between her US policy ending and the UK NHS waiting period starting. She landed on a Sunday.

She started her new job on Monday. Her manager was good. Her flat was a 20-minute walk from the office. The first six weeks felt settled.

In week seven, a colleague mentioned something called the Foreign Income and Gains regime. She looked it up. The UK had introduced it in April 2025. It exempted foreign income and gains from UK tax for new UK residents for up to four years. The election had to be made in the first UK tax year.

Olivia had been a UK tax resident from day one. The window to make the FIG election was 30 days from the start of UK tax residency, and she was in it. She'd been a UK tax resident for 38 days. The window had closed five weeks ago.

She had a significant US brokerage account. She had unvested RSUs from a US company that would continue vesting over the next three years. She had income from a US rental property. All of it was now subject to UK tax that it didn't need to be for up to four years.

The financial decisions that have hard deadlines when moving from the US to the UK happen before the moving truck arrives, and in the first 30 days after you land. Some of them cannot be recovered once missed.

The FIG Regime: The Highest-Value Election Almost Nobody Knows to Make

The UK introduced the Foreign Income and Gains (FIG) regime in April 2025. It replaced the older remittance basis system with a cleaner structure: new UK residents can elect to exempt their foreign income and gains from UK tax for up to four years of residency. The election must be made in the Self-Assessment tax return for the year of arrival.

The practical deadline: the UK tax year runs from April 6 to April 5. If you arrive in the UK on any date in the tax year, the election must be included in the Self-Assessment return filed for that year (deadline January 31 of the following year). If you miss the return deadline without the election, HMRC's position is that the FIG election for that year is forfeited.

What FIG exempts: foreign income (dividends from US stocks, income from a US rental property, US freelance income, interest from US accounts) and foreign capital gains (gains from selling US-listed stocks, proceeds from selling a US property). UK-sourced income and gains do not benefit from FIG. Your UK salary does not benefit. But the US portfolio you've spent years building is potentially sheltered from UK tax for four years.

The FIG election has a trade-off

Making the FIG election means you cannot claim the UK personal allowance (approximately £12,570) or the annual exempt amount for capital gains (approximately £3,000) in years where you elect FIG. For most US-to-UK movers with significant foreign income or gains, this trade-off strongly favors the FIG election. The personal allowance savings are small relative to the UK tax avoided on a US brokerage portfolio. But for those with minimal foreign income, the allowance may be worth more than the FIG exemption. Run the numbers for your specific situation.

What Olivia missed: four years of UK tax exemption on US portfolio dividends, US rental income, and US brokerage gains. Given the size of her US portfolio, the annual UK tax she'll now pay on those income streams runs to five figures. The window was 30 days. She missed it by 8 days. Nothing she can do about it now.

What you can do: make the election in the Self-Assessment return for your year of UK arrival. If you use an accountant, tell them about FIG explicitly. It is new enough (2025) that not every UK accountant is thinking about it proactively for inbound Americans.

The FIG election is the single highest-value financial decision for most US-to-UK movers. The window is the first UK tax year. Miss it and you cannot recover it.

Decisions to Make Before You Leave the US

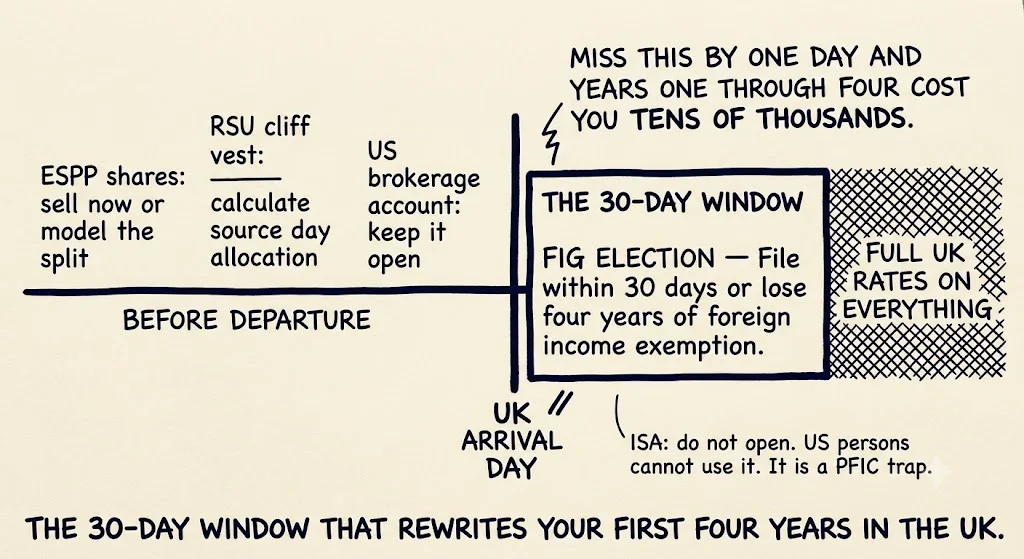

ESPP Shares: Sell Before You Board

If you have Employee Stock Purchase Plan shares in a US employer's stock, sell them before you leave the US. Once you're a non-resident alien, the IRS withholds 30% on proceeds from US securities sales. ESPP shares sold while you're still a US resident are taxed at capital gains rates (usually 15% for most tech workers at the time of sale).

The math: on $50,000 of ESPP shares sold before departure, you pay $7,500 in capital gains tax (at 15%). On the same shares sold after becoming a non-resident, you pay $15,000 in withholding. You also need to file for a refund if you're overwithheld. The window is before your flight.

One nuance: if you're a US citizen (not just a green card holder or H-1B holder), non-resident alien withholding does not apply to you. US citizens are taxed as full US residents regardless of where they live. ESPP timing matters less for US citizens than for non-citizen visa holders leaving the US.

RSU Vesting: Understand the Split Before You Leave

Unvested RSUs that vest after you land in the UK are subject to both US and UK taxation. The US taxes the US-sourced portion (US workdays between grant and vest, divided by total vesting days). The UK taxes the rest. The UK taxes through PAYE (your employer will withhold UK income tax and National Insurance Contributions). The US taxes via withholding on the US-sourced portion.

Before leaving, ask your employer's equity team: how will you calculate and withhold on RSU vests that happen while I'm UK-based? You want to understand whether they're applying the sourcing allocation correctly. Employer payroll systems frequently get this wrong, either withholding too much US tax (treating the vest as if you're still a US employee) or too little (treating the vest as entirely UK-sourced).

Also: if you have a large unvested cliff approaching within 6 months of your planned departure, consider whether it's worth accelerating the departure date or delaying it to capture the vest before the tax situation becomes two-jurisdiction. You're not required to leave on any particular date. The vest date and the departure date can both be variables.

US Brokerage: Keep It. Don't Touch the UK Equivalent.

Keep your US brokerage account open. Do not close it. Do not try to transfer assets to a UK-based brokerage or open a UK Individual Savings Account (ISA).

UK ISA accounts are tax-exempt in the UK for UK residents. For US persons (US citizens or green card holders), ISA gains are fully US-taxable as ordinary income in many cases, because the ISA wrapper is not recognized by the IRS. You'd be paying UK tax-free rates in the UK while paying full US income tax rates on the gains. The ISA advantage disappears entirely and becomes an administrative burden.

UK-domiciled investment funds (UK unit trusts, OEICs) are classified as Offshore Funds under UK law for US persons, which subjects them to UK income tax rates on gains rather than capital gains rates. They're also potentially PFICs under US law. Don't buy UK-domiciled funds. Keep US-listed ETFs in your US brokerage account.

Within 30 Days of UK Arrival

The FIG Election: Make It Now

If you have foreign income or gains (US brokerage, US rental income, US dividends), contact a UK cross-border accountant immediately. The FIG election needs to be planned and included in your Self-Assessment filing. The election itself is made on the return, but the planning (understanding what to elect, what income it covers, and whether the trade-off on personal allowance makes sense) takes time.

Do not wait until January when the return is due. Accountants are overloaded at filing time. Contact them in the first 30 days.

UK Employer Tax Code Setup

Your UK employer will set up UK PAYE (Pay As You Earn) from your first paycheck. HMRC will issue a tax code that determines how much income tax and National Insurance is withheld from your salary.

In your first year, HMRC may not have all the information it needs to set the correct code. Check your payslip: if you're on an emergency tax code (suffix M or W, or code BR), contact HMRC to get the correct code applied. Emergency codes overtax you. You'll eventually get a refund, but it's better to have the cash during the year than wait until the following April.

UK Bank Account

Open a UK bank account immediately. You need it for salary, for UK bill payments, and for day-to-day expenses. Do not use this account for investment assets. Keep your US brokerage, 401K, and long-term savings in the US. The UK bank account is for spending.

Opening a UK bank account as a new arrival

Most UK high-street banks require proof of UK address and proof of UK employment to open an account. As a new arrival, you may not have both immediately. Monzo, Starling, or Revolut offer UK accounts with a faster verification process and are accepted by most employers for salary payments. Open one of these first, get your first paycheck, then open a traditional Barclays or HSBC account once you have a UK address document (a utility bill or council tax letter).

Within 90 Days

401K: Leave It Where It Is

There is no requirement to move your 401K when you become a non-resident. Leave it in the US. It continues to grow tax-deferred under US rules. When you eventually take distributions, the US withholds and the US-UK tax treaty (Article 17) applies to reduce withholding and allocate taxing rights.

Under the US-UK treaty, the country of residence (UK, once you're resident there) generally has the primary right to tax pension income. US withholding on periodic 401K distributions is reduced to 0% under the treaty if you're a UK resident (you claim the treaty reduction on Form W-8BEN). Lump-sum distributions are taxed differently. If you take the 401K in a lump sum, check the treaty provisions for your specific situation.

Do not roll your 401K into a UK pension scheme. The US does not permit rollover to foreign pension plans. You would be required to take a full distribution (paying US income tax plus potential early withdrawal penalty) and then contribute to the UK scheme from after-tax funds. This destroys the tax deferral advantage.

US State Tax Residency: Confirm Your Exit

If you lived in a high-income-tax state before leaving (California, New York, New Jersey, Massachusetts), that state may attempt to tax your income after you've left. California in particular is aggressive about claiming residents who have not clearly severed ties.

The steps to clearly exit state residency: close state-specific accounts if possible, update your driver's license, register your new UK address as your primary address with the IRS (Form 8822), and avoid maintaining a home available for your use in the state. You should not owe state income tax on UK-earned income if you've properly established non-residency.

If you own US rental property in a high-tax state, that income remains state-taxable regardless of where you live. Moving to the UK does not exempt you from state tax on California-source rental income.

FBAR and FATCA: They Continue

If you're a US citizen, FBAR (FinCEN Form 114) applies to your foreign financial accounts regardless of where you live. Living in the UK does not end the FBAR obligation. If your UK bank accounts exceed $10,000 aggregate at any point during the year, you must file FBAR.

FATCA (Foreign Account Tax Compliance Act) requires your UK bank to report your account information to HMRC, which shares it with the IRS. The IRS will know about your UK accounts. Report them correctly and you'll have no problem. The issue is taxpayers who assume foreign account reporting ends when they leave the US.

If you're a green card holder who abandoned your card before leaving, your FBAR obligation ends with your last year as a US resident.

The Ongoing Reality of Two-Country Taxation

The US-UK tax treaty is the most comprehensive treaty the US has with any country. It covers most income types, allocates taxing rights clearly, and prevents most double taxation. But it does not eliminate the filing complexity.

You will file a US return (1040 if you're a citizen, 1040-NR if you're a non-citizen non-resident after leaving) and a UK Self-Assessment return annually. The treaty tells you which country has primary taxing rights on each income type. The Foreign Tax Credit (Form 1116 on your US return) allows you to credit UK tax paid against US tax owed on the same income.

For US citizens in the UK, the Foreign Tax Credit is usually more advantageous than the Foreign Earned Income Exclusion (FEIE). The UK's higher income tax rates generate credits that can fully offset US tax on most income types. This is different from the UAE or Singapore calculation, where there's no foreign tax to credit.

Work with a cross-border accountant who files in both jurisdictions. Do not use a UK-only accountant for your US return or a US-only accountant for your UK return. The treaty implications require someone who understands the interaction.

The thing Olivia should have known

The FIG regime was introduced in April 2025 as part of the UK spring budget. It replaced the non-dom remittance basis system. It's a significant change. It's also new enough that not every UK accountant knows to bring it up with inbound Americans. If you're moving to the UK, search for "FIG regime UK 2025" before your flight and ask your UK accountant specifically about it. Don't assume they'll bring it up. The cost of asking is zero. The cost of not asking, if you have meaningful foreign income, can run to tens of thousands of pounds per year for up to four years.

Related Reading

- Before You Leave the US for the UK: The Financial Checklist

- The H-1B Financial Playbook: What the Tax Firms Cover and What They Leave Out

- The Cross-Border Moment: What Changes Financially When You Move Between Countries

- The Expat Financial Checklist: What Mid-Senior Professionals Get Wrong Before They Relocate

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

Before You Leave the US for the UK: The Financial Checklist (Not the One About What to Pack)

Claire moved to London meticulous about logistics. Six weeks in, she found out she'd missed the UK's Foreign Income and Gains election window — the one that exempts US portfolio income from UK tax for up to four years. The window is 30 days from arrival. This is the checklist organized by deadline.

Before You Leave the US for India: The RNOR Window, the 401K Decision, and Everything Else

Vikram had spent 11 years at Microsoft. He knew about the RNOR window — he found out about it 14 months after returning to Pune. The first two 401K distributions had already been taxed at India's full marginal rate. The RNOR window had been open. He hadn't known what to do with it. This checklist is for the version of Vikram who's still in the US.

Before You Move to the US from India: The Financial Checklist Your CPA Won't Give You

Preethi kept her NRE account when she moved to San Jose — her Indian CA said it was tax-free. It is, in India. From the day she became a US resident alien, the interest was US income. Three decisions have hard deadlines before your flight: your Indian mutual funds (likely PFICs the moment you land), your PPF contribution strategy, and the Roth vs. Traditional 401K choice that has a specific non-obvious answer if you might ever return to India.