Before You Leave the US for the UK: The Financial Checklist (Not the One About What to Pack)

Claire moved to London for a role she'd wanted for three years. She was meticulous. She sorted the relocation package, the flat, the Oyster card. She opened a Barclays account in week two. Six weeks later, she found out she'd missed a window worth more than her sign-on bonus.

The UK introduced the Foreign Income and Gains (FIG) regime in April 2025. New UK residents can elect to exempt foreign income and gains from UK tax for up to four years. The election must be made in the first UK tax year. Claire arrived in October. The UK tax year ends on April 5. She had roughly six months to make the election. She didn't know it existed.

This checklist is organized by deadline. The decisions before you leave the US are different from the decisions in your first 30 days in the UK, which are different from the ongoing work. Some close permanently. Some you can address whenever you get to them. Knowing which is which is the point.

The FIG election window and the ISA decision are the two items most Americans miss. Both have consequences that compound over years.

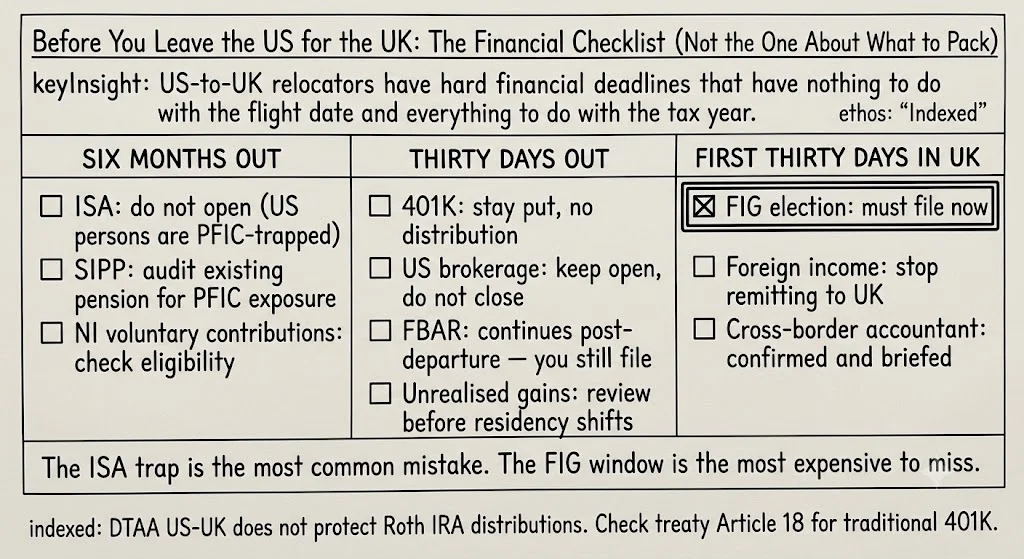

Six Months Before Departure

UK ISA: Understand Before You Open One

Your UK colleagues will tell you to open a Stocks and Shares ISA. It's what people do. ISA gains are tax-free in the UK. That's true. For UK residents who are not US persons, the ISA is one of the best savings vehicles available.

For US citizens and green card holders, the ISA is not tax-free. The IRS does not recognize the ISA wrapper. Gains in a Stocks and Shares ISA are US-taxable as ordinary income (not capital gains rates). You pay UK tax at 0% and US income tax at your full marginal rate. The ISA advantage disappears. You've created an account that requires additional US reporting for no benefit.

Decision: do not open a Stocks and Shares ISA if you're a US person. A Cash ISA (interest-bearing savings account) has a smaller implication but is still subject to US reporting. Keep your investment assets in your US brokerage account. This is the right answer even though it is counterintuitive.

SIPP and Workplace Pension

If you have a UK pension from a previous stint in the UK (or if your UK employer will contribute to a workplace pension), understand the US reporting implications before you let the pension accumulate.

UK Self-Invested Personal Pensions (SIPPs) can have PFIC exposure if the underlying funds are UK-domiciled investment trusts or unit trusts. The PFIC regime on underlying pension assets is a significant compliance burden. The US-UK treaty Article 17 covers pensions, but the interaction between the treaty pension provisions and PFIC rules for the underlying assets is unsettled.

If your UK employer's workplace pension defaults to UK-domiciled funds, ask whether you can substitute US-domiciled alternatives. Some workplace schemes allow fund selection. Others don't.

UK National Insurance: The Voluntary Contribution Window

If you've ever worked in the UK before (summer jobs, a prior job, any period of employment), you may have National Insurance contribution years on record. Those years count toward your State Pension entitlement (35 qualifying years for the full new State Pension in 2026).

You can voluntarily top up NI gaps, and the Class 2 voluntary contribution rate (available for people working abroad with existing self-employment NI history) is significantly cheaper than the Class 3 rate available to ordinary voluntary contributors. The Class 2 rate in 2026 is approximately £3.45 per week. Class 3 is approximately £17.45 per week. The difference is substantial over many years.

Apply for NI voluntary contributions via form CF83. The form can be completed while abroad and is how you lock in the discounted rate. Once you're living and working in the UK, you're automatically contributing through employment. The voluntary contribution opportunity is most relevant if you're approaching the move but haven't started yet.

30 Days Before Departure

401K: Keep It in the US

Your 401K stays in the US. Do not roll it out. Do not try to transfer it to a UK pension. There is no mechanism for rolling a 401K into a UK pension that doesn't involve a full taxable distribution. A full distribution triggers US income tax at ordinary income rates plus a potential 10% early withdrawal penalty. The UK pension you'd fund from the proceeds would be funded from after-tax dollars, destroying the pre-tax advantage of the 401K.

The 401K continues to compound tax-deferred in the US. When you eventually take distributions, the US-UK treaty Article 17 applies. For a UK resident, the UK has the primary right to tax pension distributions. US withholding is reduced or eliminated under treaty provisions with proper documentation.

ESPP: Sell Before the Flight

If you have Employee Stock Purchase Plan shares, the tax treatment on sale is significantly better as a US resident than as a non-resident alien. Non-citizen visa holders who become non-residents face 30% US withholding on US securities sales. US citizens don't face this issue (US citizens are taxed as US persons regardless of residence).

If you're on an H-1B or other non-citizen visa, sell ESPP shares before departure. The capital gains rate as a resident is 15% or 20% for most. The NRA withholding rate is 30%. The difference is material.

Foreign Account Balances: Document Them Now

FBAR (FinCEN Form 114) requires reporting the maximum balance in each foreign financial account during the year. If you open UK bank accounts in the first few months of the year, the maximum balances will appear on your FBAR for that year.

Document your balances in all existing foreign accounts (Indian accounts, Canadian accounts, any other country) as of departure. This is the baseline from which your first FBAR with UK accounts will be filed.

First 30 Days in the UK

The FIG Election: Do Not Miss This

Contact a UK cross-border accountant in your first week in the UK. Tell them you're a new UK resident with US investments and you want to understand the FIG regime election.

The FIG election exempts foreign income and gains from UK tax for up to four years of UK residency. "Foreign income" includes US dividends, US rental income, interest from US accounts, and income from US freelance or consulting work. "Foreign gains" includes gains from selling US stocks, US property, or other non-UK assets.

The election is made on your UK Self-Assessment return for the year of arrival. The deadline for filing that return is January 31 of the following year. However, planning the election (understanding what income and gains you want to shelter, whether the personal allowance trade-off makes sense) should happen in the first weeks, not in January.

What you give up to make the FIG election

Electing FIG in a given year means you cannot claim the UK Personal Allowance (approximately £12,570 in 2026) or the Capital Gains Annual Exempt Amount (approximately £3,000). For someone with meaningful US investment income or US gains, the FIG exemption is worth far more than the personal allowance. For someone with minimal foreign income and a significant UK salary generating UK tax at high rates, the personal allowance may matter more. Do the math for your specific situation.

UK Tax Code: Check Your First Payslip

Your UK employer will deduct income tax and National Insurance from your first paycheck under the PAYE system. HMRC issues a tax code that governs how much is withheld. In your first payslip, check the tax code.

Emergency tax codes (often suffix M or W, or code BR) indicate HMRC does not have your full income information yet. Emergency codes typically overtax. Contact HMRC or ask your HR department to sort the correct code. You will receive a refund for any overtax, but it's better not to lose cash flow during the year.

HMRC Self-Assessment Registration

If you have income beyond your UK employment (UK rental income, foreign income, capital gains above the annual exempt amount), you must register for Self-Assessment and file an annual return. Register at HMRC's online portal. The deadline to register for the tax year just ended is October 5 of the following year.

If you're making the FIG election, you must register for Self-Assessment and file a return even if your only income is your UK salary. The FIG election is reported on the return.

Ongoing: The Annual Rhythm

FBAR: Still Required if You're a US Citizen

US citizenship carries FBAR obligations regardless of residence. If you're a US citizen living in London, your UK bank accounts are foreign financial accounts for US purposes. If the aggregate balance in all foreign accounts (UK accounts plus any other non-US accounts) exceeds $10,000 at any point during the year, FBAR is required.

FBAR is due June 15 for overseas filers (automatic extension from the April 15 deadline). There is a further automatic extension to October 15. File it. The penalties for willful non-filing start at $10,000 per year.

US 1040: Still Required

US citizens file a 1040 reporting worldwide income regardless of where they live. Your UK salary, UK investment income, and US investment income all appear on your US return. The Foreign Tax Credit (Form 1116) allows you to credit UK income tax paid against your US liability on the same income.

For most US citizens in the UK, the Foreign Tax Credit is more valuable than the Foreign Earned Income Exclusion. UK income tax rates are high enough to generate substantial credits that offset most or all US tax liability. This is different from living in a low-tax jurisdiction like UAE or Singapore where there's no foreign tax to credit.

RSU Vests: Track Your Workdays

Each time an RSU vests while you're UK-based, the income is split between US-sourced and UK-sourced based on the ratio of US workdays to total workdays during the vesting period (from grant date to vest date). You need to track which days you worked in which country.

Keep a calendar or log that tracks your country of work each day. Annual totals are not sufficient. If HMRC or the IRS audits your sourcing allocation, you need the daily record. Travel days, conference days, and remote work days in a country count as workdays for that country.

The accountant setup that makes this manageable

The two-return system (US 1040 + UK Self-Assessment) looks overwhelming at first. In practice, it is manageable with the right professional setup. You need a cross-border accountant who files in both jurisdictions, or two accountants (one each side) who coordinate on treaty positions. Expect to pay more than for a single-country return. Budget approximately £2,000 to £4,000 per year in accountant fees depending on complexity. This is the cost of two-country professional life. It is not optional if you have US investments, RSUs, or US rental property.

Related Reading

- Leaving the US for the UK: The Financial Decisions That Have Hard Deadlines Before Your Flight

- The Expat Financial Checklist: What Mid-Senior Professionals Get Wrong Before They Relocate

- The Cross-Border Moment: What Changes Financially When You Move Between Countries

- The H-1B Financial Playbook: What the Tax Firms Cover and What They Leave Out

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

Leaving the US for the UK: The Financial Decisions That Have Hard Deadlines Before Your Flight

Olivia landed in London on a Sunday and started work on Monday. Week seven: she found out about the UK's Foreign Income and Gains regime — introduced April 2025, exempts foreign income from UK tax for four years, must be elected in the first UK tax year. She'd missed the 30-day window by five weeks. This is what she should have known before she boarded the flight.

Before You Leave the US for the Netherlands: The 30% Ruling Doesn't Do What You Think It Does

Sarah moved from New York to Amsterdam and was excited about the 30% ruling. Then her US CPA explained: the ruling reduces Dutch income tax — which reduces the Dutch foreign tax credit she can apply against her US liability. In some income bands, the US takes more, not less. And the ruling application window is exactly 4 months from day one. Miss it permanently.

Before You Leave the US for India: The RNOR Window, the 401K Decision, and Everything Else

Vikram had spent 11 years at Microsoft. He knew about the RNOR window — he found out about it 14 months after returning to Pune. The first two 401K distributions had already been taxed at India's full marginal rate. The RNOR window had been open. He hadn't known what to do with it. This checklist is for the version of Vikram who's still in the US.