The H-1B Financial Playbook: What the Tax Firms Cover and What They Leave Out

The CPA's job is to report what happened. Nobody's job is to tell you what to decide before it happens.

Arjun had been at Stripe for six years. Senior engineer, L5, managed a team of four. He knew about FBAR because a Blind thread three years ago had scared him into filing. He had a CPA who sent a PDF in early February and a DocuSign in late March. He felt covered.

Then his manager left. The org re-orged. His skip-level was now someone he'd never met. The team's H-1B sponsorship sat under a cost center that was being "evaluated." For three weeks in October, nobody could tell him with certainty whether his transfer would go through before his current petition expired.

He didn't panic about immigration. He'd been through enough renewal cycles to know the process. What he did, for the first time in six years, was look at his finances as someone who might have to leave.

He had $180K in a 401K. He'd been maxing it since year two. He knew the balance but had never modeled what happened to it if he left the US before retirement age. He had $60K in Indian mutual funds, three different schemes, all auto-reinvesting. He'd never told his CPA about them. Not deliberately. He just hadn't known they were relevant. He had RSUs on a three-year cliff, $200K unvested at current price. He'd assumed, without actually checking, that he'd have some grace period to sort it out if things went sideways.

The transfer went through. His new manager was reasonable. He went back to his desk and forgot about the three weeks.

But the questions didn't go away. He'd looked at his finances as a leaving scenario and found three holes he couldn't close. His CPA had never asked about any of them as a connected picture. Not once in six years.

This post is for Arjun. And for the version of him that exists at every H-1B company in the country.

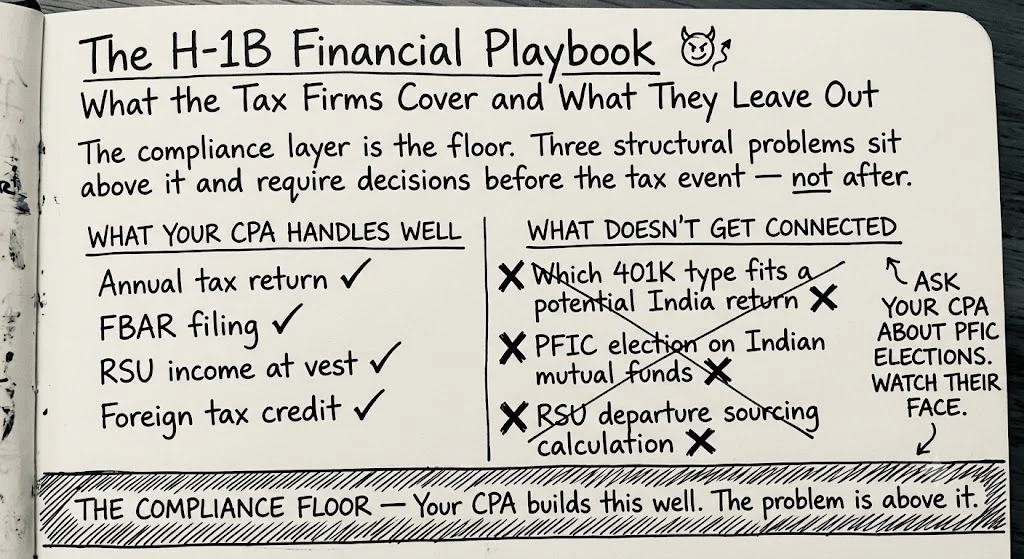

What Your CPA Actually Covers

Your CPA covers compliance. That is their job and they do it well. They report your income correctly. They file your FBAR if you have foreign accounts over $10,000 aggregate. They handle your W-2, your RSU income at vest, your Schedule B for any foreign interest. If you have a complex year, they navigate it. You pay them. They file. You're legal.

What they don't do, because it's not their job, is sit across from you and say: given your situation, given the specific timeline uncertainty of your visa status, given that you might stay 20 years or might leave in two, here is how you should be structuring your retirement contributions, here is what your Indian accounts are doing to your US tax picture, and here is what happens to your unvested equity under different departure scenarios.

They work on the past year. You need to think about the next five.

The compliance layer is real and important. If you're not filing FBAR, fix that first. If you haven't been reporting NRE account interest, that's an urgent problem. But the compliance layer is the floor. It's where you stop being in trouble. It is not where you start making good decisions.

The FBAR threshold, precisely

FBAR (FinCEN Form 114) is required if your aggregate foreign financial account balances exceeded $10,000 at any point during the year. Aggregate means across all accounts combined, not each account individually. A single month where your NRE and NRO balances together crossed $10K triggers the requirement for the entire year. The penalty for willful failure to file starts at $10,000 per year and can go significantly higher. This is not a filing you defer.

Most H-1B holders at tech companies are compliant on the basics. They file. They report their RSU income. They pay what they owe. What they haven't done is ask whether they're making the right decisions before the tax events happen.

Three problems. They're connected. Most H-1B holders have all three and have never seen them framed together.

The Three Problems the Compliance Layer Never Connects

The first problem is your 401K. Specifically, whether you're contributing to the right type, given that you might not retire in the US.

The second problem is your Indian accounts. You probably know they need FBAR reporting. What you may not know is that your NRE interest has been taxable in the US since your first day as a US tax resident, and that your Indian mutual funds have a specific legal classification that changes how any gains get taxed. Dramatically.

The third problem is your RSU sourcing. When you leave the US before your RSUs finish vesting, the tax bill doesn't stay in the US. It follows the workdays. Most people who've never been through a cross-border vest have never heard of this calculation.

None of these problems are unfixable. But they're much cheaper to fix before the event than after.

The compliance layer is the floor. These three problems sit above it and are cheaper to fix before the event than after.

The 401K Question Nobody Asks on H-1B

You're contributing to your 401K. Max, probably, because you've been told to. Your employer matches some percentage. The contribution is pre-tax. Your taxable income goes down. This feels right because it is right, for someone who retires in the US.

For an H-1B holder who might return to India, the traditional 401K math changes in a specific way.

The US-India Double Taxation Avoidance Agreement (DTAA) covers pensions and retirement income under Article 20. India has the right to tax 401K distributions received by Indian residents. The treaty prevents you from paying both US and Indian tax on the same distribution. It does not prevent India from taxing you. It just allocates the taxing right.

So if you return to India and start taking 401K distributions, India taxes them as ordinary income at your Indian marginal rate. The US withholds 10% under the treaty. India gives you a credit for that. But India's marginal rates above a threshold are 30%. You pay 10% in the US, 20% more to India. Your effective rate: 30%.

If you were contributing traditional 401K in the US and saving tax at a 32% or 35% rate, that math still works. You saved at a high rate and pay at a lower combined rate. But if your Indian retirement income puts you in a lower bracket, the spread narrows. And the "tax deferral" you've been building for decades turns out to be smaller than it looked.

Now the Roth question. Roth 401K contributions are post-tax. The growth and distributions are tax-free in the US. But the US-India DTAA does not recognize Roth accounts. India has no equivalent of the Roth concept. For Indian residents receiving Roth distributions, India treats them as ordinary income. You already paid US tax on the contributions. You now pay Indian tax on the distributions. You've paid twice.

The Roth trap for India returnees

If you return to India and retire there, Roth distributions are likely taxable in India as ordinary income under current Indian tax law. There is no treaty protection. You paid post-tax money in, it grew tax-free, and then India taxes the distributions. The Roth benefit disappears. Traditional 401K is usually the better vehicle for people with a real possibility of retiring in India. The 10% US withholding under the DTAA is the ceiling, not a floor.

There's one more piece to this. The RNOR window.

When you return to India after an extended time abroad, you typically qualify as a Resident but Not Ordinarily Resident (RNOR) for two to three years. During this period, foreign-sourced income is largely exempt from Indian income tax. That includes 401K distributions taken during the RNOR window: you pay the 10% US withholding under the DTAA, and India does not pile additional tax on top.

This is one of the most valuable financial planning levers an India returnee has. But it requires knowing it exists, returning with a plan, and timing your distributions to hit the RNOR window. Most people find out about it two years after returning, which is often inside the window but after they've already taken distributions the wrong way.

The decision question on 401K contributions isn't "should I max out?" It's "traditional or Roth, given my realistic probability of retiring in India versus the US?" If there's a genuine 40% or higher chance you'll end up in India, traditional is almost certainly the answer. If you're highly confident you'll stay in the US, the standard Roth analysis applies.

Your Indian Accounts Are a US Tax Liability

You probably have a sense that your Indian accounts need to be reported. You file FBAR. Maybe you know about FATCA. What many H-1B holders don't have is a clear picture of what exactly is taxable and why.

Start with NRE accounts. The NRE (Non-Resident External) account is one of the more useful financial structures for NRIs: you can repatriate the principal and interest freely, and India exempts the interest from Indian income tax. That's the India side. The US side is different. From the moment you became a US tax resident, the interest earned in your NRE account is taxable in the US. It goes on Schedule B. Every year.

This isn't a gray area. Interest income earned by a US resident alien is US taxable regardless of where the account is held or what India says about it. If your NRE account earned 6% interest on a ₹50 lakh balance last year, that's roughly $3,600 in interest income that belonged on your US return. Most H-1B holders have never reported it because they assumed "NRE = tax-free" applied everywhere.

NRO accounts work differently. NRO accounts hold Indian-sourced income: rent from property back home, dividends from Indian stocks, interest from Indian FDs. India withholds TDS on this income. When that income shows up in your NRO account and you're a US resident, you owe US tax on it too. You can take a foreign tax credit for the Indian TDS you already paid, but you have to file Form 1116 to claim it. It doesn't happen automatically.

Now the harder problem: Indian mutual funds.

Under US tax law, a foreign mutual fund or investment vehicle in which a US person holds shares is generally classified as a Passive Foreign Investment Company (PFIC). This classification exists specifically to prevent US taxpayers from deferring gains offshore. The rules that apply to PFICs are punitive by design.

If you hold Indian mutual funds as a US resident and do nothing special, the default PFIC tax treatment applies. Any gains are taxed at the highest ordinary income rate (currently 37%) plus an interest charge calculated from the year the gains accrued. The interest charge can be substantial on funds held for several years. The effective rate on PFIC gains under the default rules often exceeds 50% by the time the interest charge is included.

What to do about your Indian mutual funds

There are three elections available for PFIC holders: the default (worst, as described above), mark-to-market (you report gains and losses annually as ordinary income, simpler but taxed every year), and Qualified Electing Fund (QEF, best outcome, but requires the fund to provide an annual PFIC statement, which most Indian mutual fund houses do not provide). In practice, for most H-1B holders with Indian mutual funds, the cleanest path is to liquidate the funds before or shortly after becoming a US resident, pay the Indian exit tax (if applicable), and reinvest in US-domiciled vehicles. The PFIC reporting burden and the punitive default tax treatment make ongoing Indian mutual fund ownership as a US resident genuinely painful.

One more account type worth flagging: PPF. The Public Provident Fund earns interest that accrues annually. Once you're a US resident, that interest is US-taxable income in the year it accrues, even though you cannot withdraw it. Most H-1B holders earning PPF interest have never reported it.

The Indian accounts problem has a diagnostic that's worth running. Pull together every Indian account you hold. For each one, ask: (1) Is the balance over $10K at any point this year? If so, FBAR applies. (2) Is it generating income? If so, is that income on your US return? (3) Is it a mutual fund or investment vehicle? If so, you have a PFIC question.

Most H-1B holders who do this exercise for the first time find at least one item they haven't been handling correctly.

The RSU Sourcing Problem

When your RSUs vest, your employer withholds taxes and you see the net shares or the net cash. The tax event feels complete. What most H-1B holders don't know is that the US tax obligation on RSUs isn't limited to the moment you're a US resident. It follows the workdays.

Here's how RSU sourcing works. The IRS sources RSU income to the services performed between the grant date and the vest date. The percentage of that income attributable to the US is: US workdays between grant and vest, divided by total workdays between grant and vest.

Practical example. You received an RSU grant of $200,000 vesting over four years. You worked in the US for two of those four years, then left. Of the $200,000 in income, 50% ($100,000) is US-sourced because half the vesting period was in the US. When the RSUs vest after you've left, you still owe US tax on the $100,000 that was sourced to US workdays. This isn't optional. The income follows the workdays.

For H-1B holders who leave before a cliff, the math compounds. You've been working toward a $300,000 four-year cliff vest. You leave at month 30. The RSUs don't vest. You forfeit them. But if you had a separate grant that does vest with workdays split between US and your home country, you're filing a non-resident return in the US for the US-sourced portion.

The 30% problem. When you become a non-resident alien, your employer is supposed to withhold at 30% on US-sourced income (or the applicable treaty rate). The US-India DTAA can reduce this, but the reduction isn't automatic. Your employer's payroll system may not handle the treaty rate correctly. You can end up over-withheld (less common) or under-withheld (more common), creating a filing obligation in a year when you thought you were done with US taxes.

The specific calculation your employer may not be running

Your equity team has a workday sourcing allocation responsibility for any employee who moves countries during a vesting period. Many employers run this correctly. Many don't. To verify yours: take any grant where your work location changed between grant date and vest date. Calculate total calendar days (or workdays) in the grant-to-vest period. Calculate what percentage fell in the US. That percentage of the vest value is US-sourced income. If your W-2 or your 1042-S (the form for non-resident alien withholding) doesn't reflect this split, something may be off.

The decision question on RSUs for H-1B holders with genuine departure uncertainty is: what's my best approach given that a forced departure before vesting isn't zero probability? The options range from holding and accepting the sourcing complexity if you leave, to understanding the sourcing calculation deeply enough to know what your tax bill would look like in various scenarios, to having a clear-eyed view of which vest tranches matter most relative to your timeline.

None of this requires you to act differently until you have to. But it requires knowing the mechanics before the situation forces the question.

The Accounts You're Probably Not Using

A brief digression from problems to opportunities. H-1B holders are resident aliens for US tax purposes. This means you're eligible for accounts that many H-1B holders assume they can't access.

Roth IRA: you can contribute if your MAGI is below the phase-out threshold ($161,000 for single filers in 2026). You have earned US income. You are a US resident alien. You qualify. The caveat for India returnees is the one above: Roth distributions are probably taxable in India. If you're staying in the US, Roth IRA is straightforwardly useful.

HSA: if you're enrolled in a High Deductible Health Plan, you can contribute to a Health Savings Account. $4,150 for an individual in 2026, $8,300 for family. It's pre-tax going in, grows tax-free, and is tax-free coming out for qualified medical expenses. The balance is yours if you leave. It can be invested in index funds after a certain threshold. Most H-1B holders who are enrolled in HDHPs and not contributing to HSAs are leaving a significant tax benefit on the table.

Taxable brokerage: straightforward but worth stating. US-domiciled index funds in a taxable brokerage account are significantly cleaner than Indian mutual funds for US tax purposes. They're not PFICs. They get long-term capital gains treatment. They're portable. If your current India-side investment strategy involves auto-reinvesting Indian funds, the question is whether that makes sense relative to the PFIC complexity it creates.

The Questions to Ask Your CPA That They Won't Volunteer

Your CPA responds to information you give them. They can't optimize what they don't know about. These are the specific questions worth bringing to your next conversation.

1. "Am I contributing to the right type of 401K given my actual retirement scenario?" Traditional vs. Roth is not a default answer. It depends on where you expect to retire and what the DTAA treatment is in that country. Most CPAs don't volunteer this analysis unless you surface the uncertainty about where you'll retire.

2. "Am I reporting all income from my Indian accounts correctly?" This means NRE interest, NRO income, PPF interest accruals, and any Indian mutual fund distributions or gains. Give your CPA a complete list of every Indian financial account, balance, and income generated. Don't assume they know about accounts you haven't mentioned.

3. "Do any of my Indian holdings qualify as PFICs, and if so, what election should I be making?" This requires them to look at the specific funds. Indian equity mutual funds, debt funds, ETFs listed on Indian exchanges, and certain other foreign investment vehicles likely qualify. The question isn't theoretical. It has a specific answer for each fund you hold.

4. "What's my RSU sourcing situation if I leave the US before my current grants finish vesting?" Give them your grant dates, vest schedules, and the number of US workdays you've accumulated in each grant period. Ask them to model the US-sourced portion. If the number is significant, ask what withholding to expect and whether any treaty rates apply.

5. "Am I on dual-status filing for my first year?" If you arrived in the US mid-year on your current H-1B, your first year may have been a dual-status year requiring a specific filing approach. Most H-1B holders who arrived mid-year and filed a standard 1040 without checking this should ask whether their first-year return was handled correctly.

6. "If I were to leave the US in the next 12 months, what would my financial checklist look like?" This isn't a question about intention. It's a stress test. A good cross-border CPA should be able to walk through the sequence: RSU sourcing, 401K options, FBAR final year, NRE/NRO status change. If your CPA looks uncertain, that's useful information about whether you have the right professional for your situation.

Arjun's transfer went through. His situation resolved. But the three weeks changed how he thought about his finances. Not because he panicked, but because the leaving scenario forced him to look at things he'd deferred indefinitely.

The 401K he'd never modeled for departure. The mutual funds he'd never flagged. The RSU sourcing he'd never heard of. None of these were filing problems. His returns were clean. They were decision problems, and the compliance layer had never touched them.

The cost of inaction here isn't a penalty notice. It's quieter than that. It's ten years of contributions in the wrong account type. It's PFIC gains taxed at a rate that wipes out the investment thesis. It's an RSU departure tax bill that arrives after you've already moved, when you're least positioned to deal with it. These aren't catastrophic events. They're expensive non-decisions that compound quietly until they're not quiet anymore.

Your specific situation will probably need a cross-border CPA to model correctly. But the questions above tell you where to start the conversation.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

Before You Move to the US from India: The Financial Checklist Your CPA Won't Give You

Preethi kept her NRE account when she moved to San Jose — her Indian CA said it was tax-free. It is, in India. From the day she became a US resident alien, the interest was US income. Three decisions have hard deadlines before your flight: your Indian mutual funds (likely PFICs the moment you land), your PPF contribution strategy, and the Roth vs. Traditional 401K choice that has a specific non-obvious answer if you might ever return to India.

NRE and NRO Accounts: What Changes the Day You Become a US Tax Resident

NRE interest is tax-free in India. The day you become a US tax resident, it becomes US taxable income at ordinary rates — and most NRIs find out two or three years late. NRO interest has a different problem: 30% TDS generates a Foreign Tax Credit, but the credit math depends on your US bracket. FBAR applies to both accounts from year one. The gap exists because the Indian CA says 'tax-free' and the US CPA never asks.

Before You Leave the US for Australia: What to Do About Your Super and Your US Accounts

Emma asked her Australian financial planner how to transfer her 401K into her super fund. He'd seen this question before. The answer: you can't. The US doesn't allow rollovers to foreign retirement plans. Australian super is likely a PFIC. The only viable path: leave the 401K in the US and manage two retirement systems in two countries.