The Transition Year Tax Map: Planning for the Income Gap

Quick Answer

The "Transition Year" is the 12-month period surrounding your exit from a high-income W-2 role. It is the most complex tax year of your life because it usually contains two distinct financial personalities: the "high-earning employee" (Q1-Q2) and the "retired investor" (Q3-Q4). Most people plan for the lower income of retirement but forget that their final bonus, severance, and RSU vesting often push them into the highest marginal bracket for the entire year. A Transition Year Tax Map helps you sequence income, deductions, and Roth conversions to avoid the "Success Tax" that burns 10-20% of your final payouts.

You cannot plan for the income gap if you don't understand the tax bridge.

Sarah was a VP of Product at a public tech company. She decided to "retire" in July. Her plan was simple: she'd lived on $250K a year, her net worth was $6M, and she'd spend the second half of the year traveling.

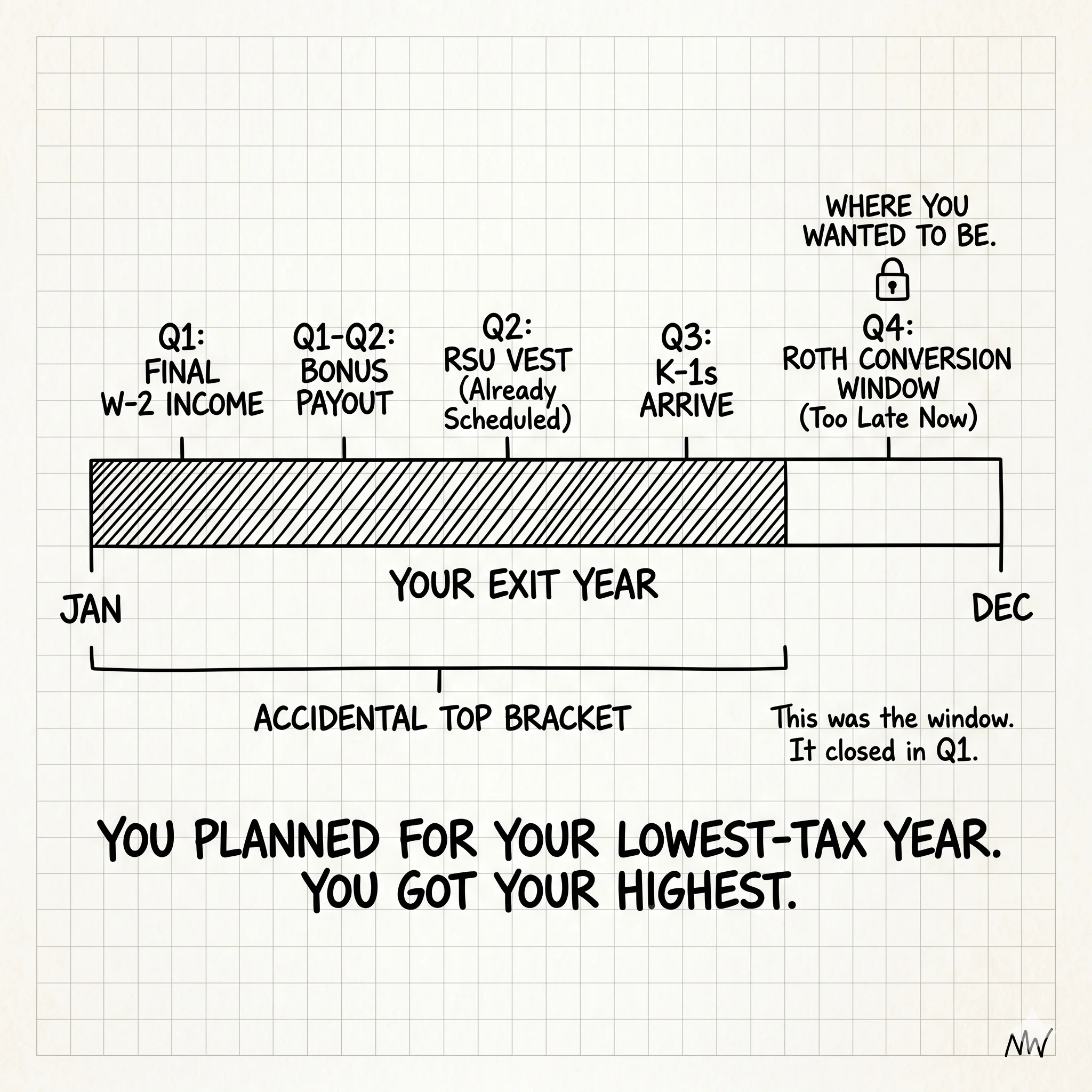

She correctly modeled that her income in Q3 and Q4 would be near zero. She planned to do a large Roth conversion in December to take advantage of what she thought would be a "low income year."

She was wrong.

Because Sarah worked until July, she received her annual bonus ($120K) in March. She had a major RSU vest in May ($200K). Her salary for the first six months was $175K. By the time she "retired" in July, her year-to-date income was already $495K.

When she did her $200K Roth conversion in December, she wasn't converting at the 12% or 22% bracket she'd hoped for. She was converting at the 37% top marginal rate. That mistake cost her $50,000 in unnecessary tax.

The Transition Year is a Hybrid. It Obeys the Rules of Your Past, Not Your Future.

The Three Zones of the Transition Year

Zone 1: The Accumulation Peak (Months 1–6)

Your final months of work are often your highest earning. Bonuses, vesting acceleration, and "payouts for unused PTO" all land here. This is where you set your marginal tax bracket for the year.

Zone 2: The Liquidity Event (Month 7)

The exit day itself. Whether it's a company sale or just a retirement package, this is the moment of peak complexity. Decisions made here (like whether to take a lump sum vs. installments) are irreversible.

Zone 3: The Income Gap (Months 8–12)

The "quiet" period. Your bank account is full, but your cash flow has stopped. This is when the temptation to "do something smart" (like Roth conversions) is highest, but the tax cost is often hidden by Zone 1.

Mastering the Bridge: 4 Critical Moves

1. The "Deferred Compensation" Bait-and-Switch

If your company offers deferred compensation, should you use it in your final year? Often, the answer is NO. If you defer income from a 37% year into a year where you'll still be in the 37% bracket (due to your exit), you haven't saved anything. You've just lost liquidity.

2. Harvesting Losses in the High-Income Year

Most people wait until they are "retired" to clean up their portfolio. This is a mistake. You want to harvest capital losses in the year you have the highest ordinary income (the Transition Year). Why? Because you can offset $3,000 of ordinary income at your 37% rate, and you can offset unlimited capital gains from your exit.

3. The Roth Conversion Delay

Wait. Just wait. Unless you are retiring in January, your "Transition Year" is almost always a high-income year. The time to do massive Roth conversions is the *first full calendar year* of retirement (Year 2), when your total income is truly near zero.

4. Charitable Bunching

If you have a high-income year (the Transition Year) followed by low-income years, use a Donor Advised Fund (DAF). Contribute 5-10 years' worth of your planned charitable giving in the transition year. You get the deduction at the 37% rate, and you can distribute the money to charities slowly over the next decade.

Warning: The AMT Trap

High income combined with ISO exercises in the same year is the ultimate recipe for an Alternative Minimum Tax (AMT) disaster. If you are exiting a company and exercising options, the "Transition Year" becomes a $100K+ tax event if not sequenced correctly. Never exercise and sell in the same year without a pro-forma tax return.

The Checklist for Your Exit

- Run a "Mock" Tax Return in June. Don't wait until April. You need to know your projected AGI before you make Year-End decisions.

- Check your RSU withholding. Most companies withhold at 22%. If your transition year puts you at 37%, you will owe a massive bill in April. Increase your withholding or set aside cash.

- Max out everything early. Get your 401(k) and HSA contributions done before you leave. You can't contribute to these once the W-2 stops.

Retirement is a Destination. The Transition Year is the Journey.

If you don't map the journey, you will arrive at the destination with significantly less fuel than you planned. The "Income Gap" is an opportunity for tax optimization, but only if you acknowledge that the bridge to get there is built on high-income foundations.

Run Your Wealth Like You Run Your Career. Plan the Exit with the Same Precision You Used to Plan the Promotion.

Are you exiting in the next 12 months?

Get your Transition Year Tax Map ready before you sign the papers.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

The RNOR Window: The 2-3 Year Tax Opportunity Most NRIs Miss

Your first 2-3 years back in India, foreign income is largely tax-free. It's the window for Roth conversions and asset restructuring. Almost nobody plans for it before they leave the US.

Liquidity Event Sequencing: Pre-Exit Tax Planning for Founders

Real exit tax savings (15-25% of proceeds) come from decisions 12-18 months before close. Master charitable structures, entity optimization, QSBS timing, and option planning.

Roth IRA Is a Tax Trap for NRIs Returning to India

India taxes Roth distributions as ordinary income. The account everyone told you to max is built for a US retirement, not an India return. Most NRIs find this out too late.