The 83(b) Election When You're on an H-1B: The Startup Advice That Doesn't Account for Visa Risk

The 83(b) election is usually the right move for early startup equity. For H-1B holders, one sentence in the plan document can make it the wrong one.

Wei was employee number 12. The startup had closed a Series A six months earlier. His attorney said: file the 83(b) within 30 days, it's standard practice. He filed it. The 409A valuation was $0.02 per share on 500,000 shares. The tax bill was approximately $300.

Two years later, the company closed a Series B at $4 per share. Wei's equity was worth $2 million on paper. His H-1B renewal was denied — his employer had missed a technical requirement in the petition. They couldn't find a cap-exempt slot for six months. Wei needed to choose between leaving the US or finding another employer quickly. He looked at his equity plan. It had a US residency requirement: continuous US residency was a vesting condition. If he left the US, his unvested shares were forfeited.

He'd pre-paid $300 in tax to secure shares he could no longer hold.

Why the Standard Advice Is Right (Most of the Time)

The 83(b) election allows you to pay income tax on restricted equity at the time of grant rather than at the time of vesting. For early startup equity at a low 409A valuation, the math is compelling: the shares are worth very little now, so the tax on "current fair market value" is negligible. If the company succeeds, the appreciation from grant to vest is treated as capital gains, not ordinary income. Without the election, all appreciation from grant to vest is ordinary income when the shares vest.

On 500,000 shares at $0.02, the tax on making the election is trivial. On 500,000 shares at $4 at vest — a theoretical scenario but a real one — the difference between capital gains treatment and ordinary income treatment on the growth from $0.02 to $4 is substantial.

The standard advice — file the 83(b), it's standard — is correct for most startup founders and early employees. The calculus has three inputs: the current 409A valuation, the expected appreciation, and the probability of vesting. If the current value is very low and the company has traction, the election makes sense.

For H-1B and L-1 visa holders, there's a fourth input that the standard advice omits.

The Fourth Input: Vesting Conditions in the Plan Document

Many US startup equity plans have provisions that were written for US employees and haven't been updated to account for globally mobile workforces. One common provision: a US employment or US residency requirement as a condition of continued vesting.

The provision typically reads something like: "Vesting is conditioned on Employee's continuous employment with the Company and Employee's continued authorization to work in the United States." Or more bluntly: "If Employee's visa status changes such that Employee is no longer authorized to work in the United States, all unvested shares shall be immediately forfeited."

If your plan has this language, the 83(b) election has a specific risk that the standard advice doesn't account for: you can pre-pay tax on shares that may be forfeited not because you left the company, but because your visa renewal was denied, the H-1B cap lottery didn't go your way, or your employer couldn't maintain your sponsorship.

The election is irrevocable. The pre-paid tax is not refundable. The loss on forfeited shares is a capital loss, not a refund of the income tax you paid.

What Happens If You Forfeit After Filing 83(b)

If you file an 83(b) election and later forfeit the shares (whether due to employment termination or a plan-enforced condition like the residency requirement), the tax you paid at grant time cannot be recovered as an income tax refund. You paid income tax on ordinary income at grant. The shares are now gone. The IRS does not reverse the income tax.

What you can claim is a capital loss equal to your basis in the shares. If you paid $300 in tax on shares worth $10,000 at grant ($0.02 × 500,000 shares), your basis is $10,000. If you forfeit with no proceeds, you have a $10,000 capital loss. Capital losses can offset capital gains, and up to $3,000 per year of capital losses can offset ordinary income.

The capital loss treatment is better than nothing but is not the same as a refund. On a large grant at a higher 409A valuation, the gap between what you paid in income tax and what you recover via capital loss can be significant.

The H-1B cap lottery risk

Unlike H-1B renewals for existing employees (which don't go through the lottery), initial H-1B petitions are subject to the annual cap lottery. As of recent years, with demand significantly exceeding the 85,000 annual cap, the odds of selection in any given year are roughly one in four for most registrants. If you join a startup on OPT, file an 83(b) election within 30 days, and then are not selected in the cap lottery for two years — you may face a situation where your OPT work authorization expires before you have an H-1B. If the plan has a work-authorization vesting condition, unvested shares are at risk. This is a structural risk for startup employees relying on H-1B cap lottery selection.

Three Steps Before Filing

Step 1: Calculate the actual tax cost at the current 409A valuation. The 83(b) election is only worth filing if the protection is worth the cost and the risk. Get the current 409A valuation from the company. Multiply by your share count. The income tax on that amount at your marginal rate is your cost. If the cost is $300, the risk-reward is very different than if the cost is $30,000.

Step 2: Read the equity plan for residency and work-authorization vesting conditions. The plan document is longer and more legal than the grant agreement. It's the governing document. Search it for the words "residency," "authorized to work," "immigration," and "visa." If there's a US residency or work-authorization vesting condition, that's the risk to evaluate.

Step 3: If the condition exists, decide your response. You have three options.

Option A: Negotiate removal of the residency condition before you file the 83(b). This is the cleanest path. Ask the company's legal counsel or the board to amend the plan or issue your grant under a modified grant agreement without the residency condition. Not all companies will agree, but the request is reasonable and startups with international employees are increasingly aware of the issue.

Option B: File the 83(b) anyway, acknowledging the visa risk as a factor you're accepting. This is the right call if the 409A valuation is very low, the visa risk is low (e.g., you're on an L-1 with strong sponsorship rather than dependent on the H-1B lottery), and the company's prospects are strong enough that the protection is worth the residual risk.

Option C: Don't file the 83(b). This means the appreciation from grant to vest will be ordinary income at vest. For a very early-stage company where the 409A is legitimately low and likely to increase significantly, this is usually the worse financial outcome if you do vest. But it avoids the capital loss trap if you don't.

L-1 and O-1 Visa Holders: Similar Structure, Different Risk Profile

L-1 visa holders have an intracompany transfer structure that's generally more stable than H-1B cap-subject status. If your L-1 is tied to a parent or affiliated company, your sponsorship stability depends on the company's continued US operations and your continued role. The residency vesting condition risk still applies — read the plan document regardless of your visa category.

O-1 visa holders (extraordinary ability) generally have more immigration flexibility, with multiple potential sponsors and a higher success rate on renewals. The H-1B cap lottery doesn't apply. The residency vesting condition risk still exists if the plan has that language, but the immigration risk component is lower.

The 83(b) analysis is the same for all three visa categories: calculate the cost at current 409A, read the plan for conditions, then decide. The immigration stability factor is different for each, which affects the probability weight you give to the forfeiture scenario.

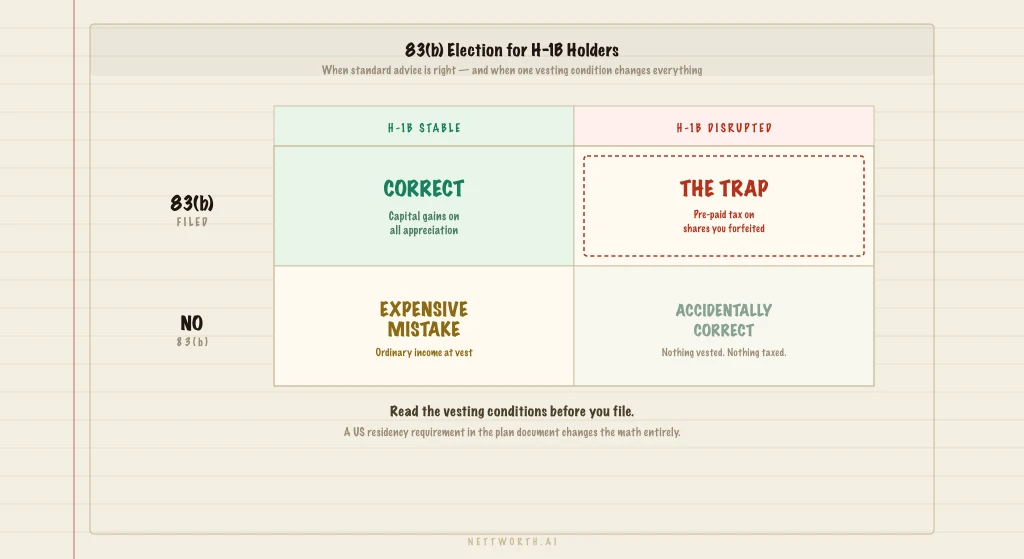

The Decision Matrix

Run the election through this:

409A valuation very low (under $0.10/share) AND no residency condition in plan: File the 83(b). The cost is negligible and the protection is real.

409A valuation very low AND residency condition in plan AND visa is H-1B cap-subject: Attempt to negotiate removal of the condition. If company declines, assess the visa risk probability. H-1B cap lottery failure is a real risk. Consider the cost-benefit carefully.

409A valuation meaningful (over $0.50/share) AND residency condition in plan: Do not file without addressing the condition. The cost of filing on meaningful valuation shares that you subsequently forfeit is material.

L-1 or O-1 with no cap lottery risk AND residency condition in plan: Immigration risk is lower. File the 83(b) if the cost is low, but still attempt to negotiate the condition removal if you have the leverage.

Wei got a new H-1B on day 58. He stayed in the US. His unvested shares eventually vested and he did well on the company's eventual exit. The 83(b) election turned out to be the right call for him financially. What he said afterward was simpler: "I would have made the same decision. But I would have made it knowing the risk. I didn't know the risk existed."

Reading the plan document before filing is a 30-minute task. It's also the 30 minutes most people skip.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

Before You Move to the US from China: Your Financial Checklist

Wei assumed his Chinese A-share brokerage account was invisible to the IRS. What he hadn't read: China joined the Common Reporting Standard in 2018. His bank had been automatically reporting his account to the Chinese tax authority, which shares with the IRS. Before you become a US resident alien, you need to know what this means for your accounts.

Traditional 401K or Roth 401K When You Might Move Back to India? The Math Most H-1B Holders Never See

Meera maxed her 401K every year for seven years. Then a colleague mentioned something: India taxes 401K distributions as ordinary income. She'd assumed the tax treaty covered it. It does — but not the way she thought. The treaty prevents double taxation. It doesn't prevent Indian taxation. And Roth 401K is worse.

Your First 90 Days in the US from India: The Financial Decisions Nobody Briefs You On

Dev had $35,000 in SBI Blue Chip and HDFC Top 100 when he landed at SFO on an H-1B. Fourteen months later his CPA asked if he'd filed Form 8621. He hadn't heard of it. Three decisions — PFIC elections, FBAR filing, and Roth vs. Traditional for someone who might return to India — needed to happen in the first 90 days. Nobody told him.