Backdoor Roth at $400K: Is It Worth It?

Short answer: probably yes, but not because everyone says so.

The longer answer requires knowing three things about your situation that generic financial advice never asks.

Quick Answer

The backdoor Roth IRA converts a non-deductible traditional IRA contribution into a Roth, bypassing the direct income limit. In 2026, it works cleanly if you have no existing pre-tax traditional IRA assets. If you do, the pro-rata rule dramatically reduces the benefit. For most HENRYs, the mega backdoor Roth — via after-tax 401(k) contributions — is worth 5-6x more and should be explored first. The Roth Worthiness Test below tells you which applies to you.

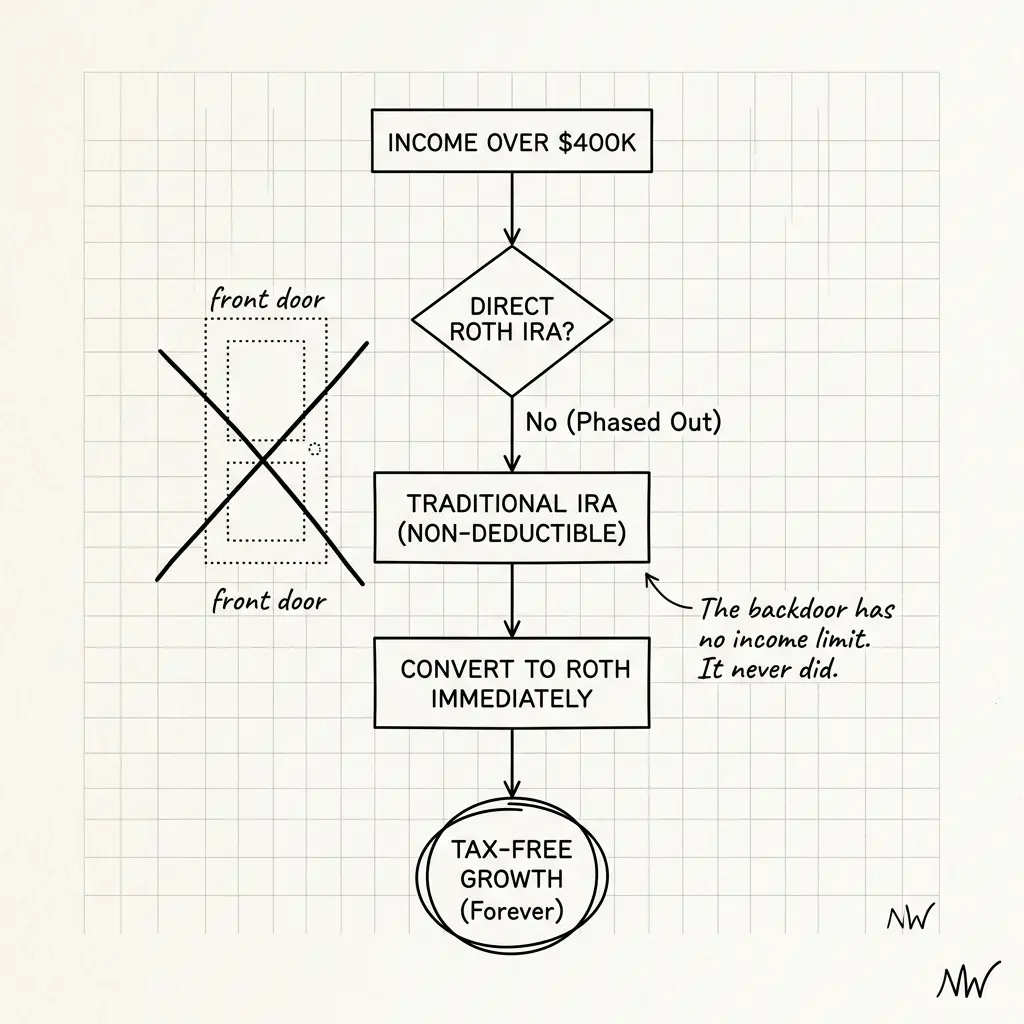

Why the Income Limit Exists (and Why It Doesn't Apply Here)

In 2026, direct Roth IRA contributions phase out at approximately $150,000 (single) and $240,000–$250,000 (married filing jointly). Above those thresholds — which, at $300K+, you are — you can't contribute directly.

The backdoor route:

Contribute up to $7,000 ($8,000 if age 50+) to a traditional IRA as a non-deductible contribution. No income limit applies to contributions — only to deductible contributions.

Immediately convert that traditional IRA to Roth. The conversion is taxable only on growth between contribution and conversion — which, done same-day, is zero.

Legal since 2010. Still legal. The IRS confirmed validity in Notice 2014-54.

The Pro-Rata Rule: Where Most People Get Tripped Up

This is where the strategy breaks for many HENRYs. And where generic "just do the backdoor Roth" advice fails.

If you have any pre-tax traditional IRA assets — a rollover IRA from a former employer, a deductible traditional IRA from lower-income years, a SEP-IRA — the IRS doesn't let you convert just the non-deductible portion. It treats all traditional IRAs as one pool.

Taxable % = Pre-tax IRA balance ÷ Total traditional IRA balance

Concrete example:

// Pro-Rata Trap

Rollover IRA from former employer: $193,000

New non-deductible traditional IRA: $7,000

Total traditional IRA pool: $200,000

Pre-tax ratio: $193K ÷ $200K = 96.5%

Taxable conversion amount: $7,000 × 96.5% = $6,755

At 37% marginal rate: $2,499 in taxes to put $7,000 in Roth.

The "backdoor" barely worked.

The workaround: Roll your pre-tax traditional IRA into your current 401(k) before making the backdoor contribution. This zeroes out the pre-tax IRA balance and clears the pro-rata trap.

Not all 401(k) plans accept incoming IRA rollovers. Check your Summary Plan Description or ask your benefits administrator before assuming you can.

The Mega Backdoor Roth: Usually Worth More

Most HENRYs focus on the backdoor Roth ($7,000/year) and miss the mega backdoor, which can be 5-6x more valuable.

Most 401(k) plans allow total annual additions up to the federal "annual additions limit" — approximately $70,000 in 2026 (verify with your plan). After maxing your employee contribution (~$24,500 in 2026) and employer match (~$5,000 to $15,000 depending on employer), there's often $30,000–$45,000 of room for after-tax (non-Roth) contributions.

If your plan allows in-service withdrawals or in-plan Roth conversions, you can contribute after-tax and immediately convert to Roth. No income limit. No pro-rata rule. Up to $40,000+ in Roth conversions per year beyond the employee contribution limit.

Two things your plan must allow:

(1) After-tax contributions, and (2) in-service withdrawals or in-plan Roth conversions. Many plans don't allow one or both. Check the Summary Plan Description under "After-Tax Contributions" before assuming this works for you.

The Roth Worthiness Test

Two minutes. Run through this:

Step 1: Do you have pre-tax traditional IRA assets?

→ Yes, and my 401(k) doesn't accept IRA rollovers: Backdoor Roth is largely broken by pro-rata. The complexity cost outweighs the benefit.

→ Yes, but my 401(k) accepts rollovers: Roll the IRA in first. Then proceed with backdoor Roth.

→ No: Backdoor Roth works cleanly. Proceed.

Step 2: Does your 401(k) allow after-tax contributions with in-service conversion?

→ Yes: Mega backdoor Roth is worth 5-6x more. Pursue that first. Standard backdoor Roth is secondary.

→ No: Standard backdoor Roth ($7,000/$8,000) is your best Roth option. Worth doing.

Step 3: Is this actually your highest-priority financial decision right now?

The backdoor Roth is worth approximately $7,000 × your expected tax rate differential over decades. At 20%, that's roughly $1,400 in lifetime value. Not nothing. But if you have RSU vest decisions, ISO exercise windows, or QSBS holding periods pending — those generate 10-100x the financial impact per hour of attention. Do those first.

A 2026 Catch-Up Rule That Changed

Recent legislation introduced a mandatory Roth catch-up rule for employees age 50 and older who earned more than $145,000 in FICA wages in the prior year.

If you're 50+ and earned above that threshold in 2025, your 2026 catch-up contributions must go to Roth — the pre-tax catch-up deduction is no longer available to you.

If you've been using catch-up contributions to reduce current-year taxable income, verify with your plan administrator. The change affects traditional and Roth 401(k) catch-up contributions.

FAQ

Is the backdoor Roth still legal in 2026?

Yes. The IRS confirmed its validity in Notice 2014-54. Despite periodic legislative threats — including the 2021 Build Back Better Act's proposed elimination — the backdoor Roth remains intact.

Does the conversion need to happen immediately after the contribution?

No, but faster is better. The longer you wait, the more growth accumulates in the traditional IRA — and that growth is taxable ordinary income at conversion. Convert within the same tax year as the contribution. Many people do same-day or same-week conversions.

Can my spouse do this too?

Yes. Each spouse contributes to their own IRA — $7,000 each ($8,000 each if 50+). The income phase-out applies to household income, but each IRA is individual. A married couple can move $14,000–$16,000 annually into Roth via backdoor.

What's Form 8606 and why does it matter?

Form 8606 tracks your IRA basis — the non-taxable portion from non-deductible contributions. Without proper 8606 filing, you can end up paying taxes twice on the same money years down the road. File it every year you make a non-deductible traditional IRA contribution, even if you convert immediately.

I have a SEP-IRA from freelance income. Does that affect this?

Yes. SEP-IRA balances count as pre-tax traditional IRA assets for pro-rata purposes. If your SEP-IRA has significant pre-tax balances, the backdoor Roth benefit is dramatically reduced. The workaround — rolling SEP into your employer 401(k) — requires checking whether your 401(k) plan accepts SEP rollovers. Not all do.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

Mega-Backdoor Roth

A product guru didn't know it existed. A financial advisor colleague never mentioned it. The $1M+ lifetime tax shelter hiding in plain sight.

The Green Card Exit Tax: Why Your Biggest Immigration Upgrade Has a Hidden Cost

After 8 years, a green card isn't just an immigration status — it's a tax position with a specific cost to exit. The deemed-sale rule applies to your entire portfolio on the day you leave. Most NRIs don't discover this until they want to move back.

The RNOR Window: The 2-3 Year Tax Opportunity Most NRIs Miss

Your first 2-3 years back in India, foreign income is largely tax-free. It's the window for Roth conversions and asset restructuring. Almost nobody plans for it before they leave the US.