Digital Wealth Custody: Protecting Your Family's Single Point of Failure

Quick Answer

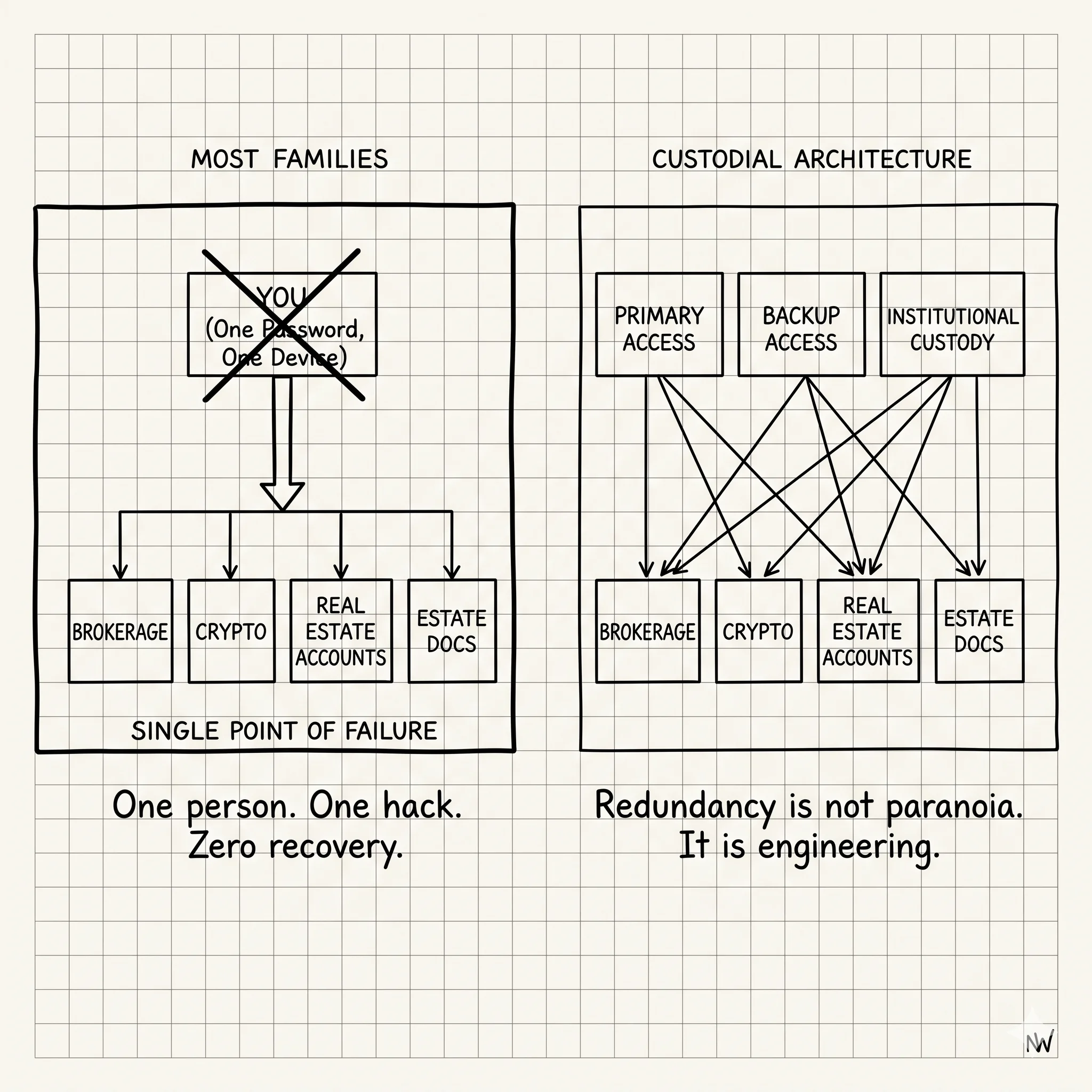

Most high earners treat digital security as a "password problem." For a family with $5M+ in assets, security is a "custody problem." Your current setup—likely a single password manager and a phone-based 2FA—creates a single point of failure that is vulnerable to social engineering, device theft, or mortality events (if you die, your family is locked out). Digital Wealth Custody is the move from fragile individual security to institutional-grade wealth infrastructure: multi-signature authorizations, air-gapped hardware, and cold-storage protocols. It's the difference between "securing your accounts" and "protecting your family's future."

Your family's safety shouldn't depend on a single password that your spouse doesn't know.

Mark was a tech founder with $12M in net worth. He was "good" at security. He used a password manager. He had 2FA on everything. He even had a hardware key for his primary email.

Then he went for a run in San Francisco and his phone was snatched while it was unlocked.

In the 20 minutes it took him to get home and try to lock his accounts, the thief had changed his Apple ID password (using the unlocked phone), gained access to his primary email, and initiated transfers from his Coinbase and Mercury accounts. Because the thief had the physical device and the primary email, they were able to bypass nearly every security layer Mark had built.

He didn't lose everything, but he lost $400K in under an hour.

The problem wasn't Mark's password. The problem was his architecture. He had built a system where a single unlocked device was the master key to his entire empire.

If One Device or One Person Can Move All the Money, Your Wealth is Fragile.

The Single Point of Failure (SPOF) Audit

Perform this audit on your family's financial state today. If you answer "Yes" to any of these, you have a critical vulnerability:

- Can a single person (you) move more than 50% of the net worth without a second person's approval?

- If your primary phone is stolen while unlocked, can someone change the password to your primary brokerage account?

- If you died today, would it take your spouse more than 48 hours to gain access to the accounts?

- Is your "Seed Phrase" or "Emergency Recovery Kit" stored in a digital format (notes app, email, computer) instead of physical cold storage?

Leveling Up: From Passwords to Infrastructure

Wealthy families and institutions don't rely on "strong passwords." They rely on multi-party computation (MPC) and air-gapped protocols. You can implement these same strategies for your personal wealth.

1. Multi-Signature (Multi-Sig) Controls

Never rely on single-person approval for large transfers. For crypto, use a 2-of-3 or 3-of-5 multi-sig (like Gnosis Safe). For traditional brokerage, set up secondary approval requirements for wires over a certain threshold. It creates a "circuit breaker" for social engineering.

2. The Air-Gapped Fortress

The most critical assets (long-term holdings, equity documents, private keys) should never touch the internet. Use air-gapped hardware wallets or dedicated, "clean" devices that are only turned on for specific, planned transactions.

3. Redundant Custody

Don't keep everything at one institution. The $285M Drift hack showed that even "decentralized" platforms have protocol risks. Split your wealth across 2-3 tier-1 institutions with different security architectures.

The "Mortality Event" Protocol

Security is often at odds with availability. You make it so secure that your family can't get in if you're gone.

How to Build a Resilient Recovery Plan:

- Physical Cold Storage: Keep one physical copy of your recovery kit (passwords, keys, instructions) in a safe deposit box or home safe.

- The 48-Hour Training: Once a year, walk your spouse or heir through the "Emergency Access" procedure. Don't just tell them—have them do it.

- Independent Custodians: Use a service (like Casa or a trusted law firm) that can help recover access through a multi-sig process without having full control themselves.

Wealth is not just what you own. It's what you can protect and pass on.

In the digital age, your greatest liability is the "Single Point of Failure." Moving to institutional-grade custody feels like a burden until the day your phone is stolen or your email is hacked. Then, it's the only thing that matters. Build the fortress before the storm arrives.

Run Your Wealth Like You Run Your Career. Build Redundancy into the Foundation.

Could your family survive your phone being stolen?

Build your Digital Wealth Custody framework today.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

Life Insurance as Financial Tool

You can self-insure mortality risk. You cannot self-insure the gap between your wealth and your family's actual needs. Here's what actually matters when you have millions.

The Estate Planning Inflection

Most people think trusts are for death. Vivek Joshi's LLC conversation revealed the real value: structures that protect and govern while you're alive.

The Estate Planning Inflection: Structures That Work While You're Alive

Most people think trusts are for death. They're wrong. Here's what wealthy business owners do while they're alive to protect what they've built.