The Estate Planning Inflection

Most people think trusts are for death. They're wrong. Here's what wealthy business owners do while they're alive to protect what they've built.

You've built a $5M company. Revenue's solid. You have employees who depend on you. Your family's lifestyle depends on it. And last night, you realized something that kept you awake until 3am. If you die tomorrow, your family doesn't inherit a company. They inherit a legal disaster.

Your attorney said something about trusts. Your accountant mentioned an LLC. Someone told you about family entities. But nobody explained what these things actually do. So you did what most business owners do. You nodded, said "I'll think about it," and got back to work.

The problem is this. Your attorney was talking about death planning. Trusts, probate avoidance, tax minimization for your estate. All important. But not urgent. What you actually need is life planning. Structures that work while you're alive. Structures that protect your company, your family, your assets. Structures that clarify who controls what, what happens if you're incapacitated, and what your family actually owns. Two different things. Most people conflate them. That's expensive.

The Single Point of Failure

Here's your current structure (even if you don't realize it). Your company exists as you. You sign contracts. You make decisions. Your personal credit is tied to your business credit. Your family has no idea what's in your business bank account or how to access it if you're gone.

If you're in a car accident tomorrow and in a coma for 6 months. Your company can't function because you're the only one who can sign documents. If you die. Your company's contracts transfer to your estate (which takes 12-18 months to settle). Your employees can't get paid without your executor's permission. Your family has no decision-making authority over the business they just inherited.

This is the Single Point of Failure. Your company depends entirely on your continued existence. Wealthy business owners don't operate this way.

What Wealthy Business Owners Actually Do (The Operating Agreement)

The first thing is simple but rarely done. An operating agreement. This is a 10-20 page document that says:

- How decisions are made (who decides what, voting structure)

- What happens to your shares if you're incapacitated (successor authority)

- What happens to your shares if you die (it goes to your trust, not your probate estate)

- What happens if a partner disagrees (buyout formula, dispute resolution)

It's not sexy. It doesn't make you money. But it does three things. First. It clarifies ownership. Your wife knows exactly what percentage of the company you own. Your kids know. Your accountant knows.

Second. It prevents chaos. If you're in a hospital for 6 months, the operating agreement says "CFO takes over." Not "company shuts down waiting for your recovery." Third. It forces you to name a successor. Not your wife (who may not want to run the company). Not your oldest child (who may be incompetent). Your actual chosen successor.

Most business owners don't have this because they never ask the question. "Who would actually run this if I couldn't?"

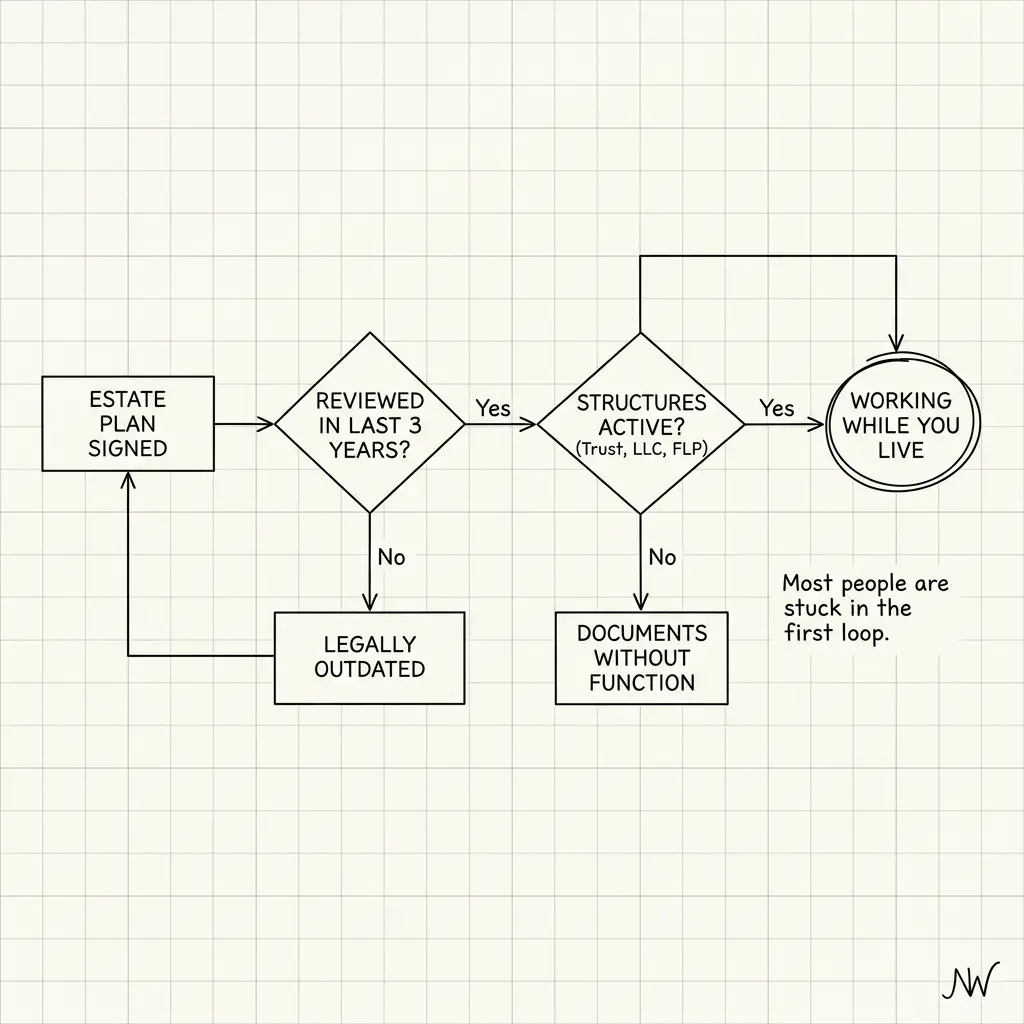

The Revocable Living Trust (It's Not About Death)

Now the trust. And here's where the reframe happens. Your attorney will say. "The trust avoids probate when you die." True. But incomplete. The real reason wealthy business owners use revocable living trusts while they're alive is this. Incapacity planning.

If you're in a coma. Your family can't access your business. Your bank accounts are frozen. Your investment accounts are frozen. Everything requires your signature. A revocable living trust says. "I own all this. But if I'm incapacitated, my designated successor (not a court, not a judge) takes over and can sign documents, access accounts, and make decisions." That's the power. The trust works for you while you're alive. Not just for your kids after you die.

The structure is simple. You create a trust (costs $1,500-3,000 with a good attorney). You transfer your assets into it (company shares, real estate, investments). You name a successor trustee (your CFO, your spouse, your business partner). If you're incapacitated, that successor runs things without court involvement.

When you die, the trust's terms take over (who gets what, how fast, any conditions). But that's secondary. The primary benefit happens while you're alive and unable to act.

The Family Entity (Multiple Benefits)

Now add a layer. Some business owners put their company inside a family holding company or family LLC. Structure looks like this. You own a holding company. The holding company owns your operating business. Your spouse and kids own percentages of the holding company.

Why do this. First. Asset protection. If someone sues your operating business, they can't reach the holding company or your personal assets. Second. Succession planning. Your kids are already partial owners of the holding company. They have ownership psychology. They understand the business is a family asset. Third. Tax flexibility. The holding company can own real estate, make distributions, and minimize tax exposure in ways an operating business can't. Fourth. Incapacity planning. If you're incapacitated, the holding company structure says "your spouse and kids can make decisions through voting" without going to probate court.

Wealthy families do this not because it's complex. But because it buys time and clarity.

What This Actually Costs (In Time and Money)

Let's talk reality. An operating agreement: $2,000-3,500. A revocable living trust: $1,500-3,000. Asset transfers into trust: $500-1,500. A family holding company structure: $3,000-5,000. Total. $7,000-13,000 in legal fees. Time to set up. 4-6 weeks if you're responsive.

That feels expensive until you realize. If you die without this structure, your family spends $50,000-100,000+ fighting through probate court for 18 months while your company's future is uncertain. The math is simple. Pay now or pay way more later.

The Inflection Point (Why Now Matters)

Here's the trap most business owners fall into. They think. "I'll do this when the company is bigger. When it's more valuable. When I have more time." Wrong. The best time to set this up is now. When your company is young and the stakes feel lower.

Why. First. Cheaper. Transferring a $500K company into a trust costs the same as transferring a $5M company. Do it early. Second. Clearer thinking. When the stakes aren't life-or-death, you make better decisions. You're not under pressure. You can ask the hard questions. "Who would actually run this?" "What do I want my kids to inherit?" Third. Employee confidence. When your team knows there's a succession plan and structures in place, they stay. They don't start job hunting.

This is the Estate Planning Inflection. The moment when you shift from "I'll do this eventually" to "I'm doing this this quarter."

Your Next Move

This month. Schedule a 30-minute call with an estate planning attorney (not your corporate attorney, not your tax advisor, someone who specializes in business succession). Tell them. "I have a $X business. If I died tomorrow, what would actually happen to it. What should I put in place now while I'm alive." They'll walk through operating agreements, trusts, succession planning. Pick one thing to start with (probably the operating agreement).

Next month. Finalize the operating agreement (clarify ownership, successor authority, decision-making). Start the trust process (get a list of assets to transfer).

Quarter 2. Fund the trust (transfer company shares, real estate, investments). Update beneficiary designations on retirement accounts. Name successor trustees with a conversation (not by surprise after you die).

The outcome. Your wife knows exactly what you own. Your kids know what's coming to them (and when). Your business has clear succession authority. If you're incapacitated, someone can run things. If you die, your family doesn't fight through court. That's not complicated. It's the foundation. Get it right.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

Digital Wealth Custody: Protecting Your Family's Single Point of Failure

Passwords aren't infrastructure. Protect your $5M+ empire with multi-signature controls, air-gapped protocols, and institutional-grade custody.

The Healthcare Horizon: Real Costs for Early Retirees (Ages 40–65)

You stress-tested recessions, sequence of returns, and market crashes. But the spreadsheet goes blank on healthcare. Here are the real numbers.

What to Do (and Not Do) in the First Six Months After Inheriting Money

The first six months after inheriting money are almost entirely about not making irreversible mistakes. The advisors calling you want you to move fast. That is not in your interest. Here is the practical sequence: hold, inventory, understand, then decide.