Do You Actually Need a Financial Advisor After Inheriting? (And How to Find One If You Do)

You've gotten seven calls in three weeks. Each one starts the same way: "I wanted to reach out personally." You haven't called any of them back. Your question is not "which one should I hire." Your question is whether you need any of them at all.

That is the right question to start with.

The financial advisory industry is structured to make you feel like you need it regardless of whether you do. The advisors who called you got your name from the probate filing. They are in the business of converting inheritance events into client relationships. That doesn't mean they're bad at their jobs. It means their incentive to reach out to you is not the same as their incentive to serve you well.

Here is an honest answer to the question: maybe you need an advisor, maybe you don't. It depends on your situation. And the ones who called you are probably not the right ones regardless of whether you hire someone.

The Honest Case for Not Hiring Anyone

If your inheritance landed in a Schwab brokerage account, and you are a reasonably organized adult who is willing to spend 20 hours over the next six months learning how to manage it, the Bogleheads approach (three-fund portfolio, low-cost index funds, rebalance once a year) is genuinely appropriate for most inherited money. It is not complicated. It does not require an advisor. Millions of people do it themselves.

The evidence is clear and consistent: the average actively-managed fund underperforms a simple index fund after fees over any 10-year period. The average investor who hires an advisor does not consistently outperform the average investor who uses a simple index portfolio. The value advisors provide is mostly behavioral (stopping you from panic selling in 2020) and organizational (making sure you're not leaving money in a savings account for five years). Both of those are real values. Neither requires a 1% AUM fee.

1% of $3M is $30,000 per year. Every year. Whether markets are up or down. That is a real number. It compounds. Over 20 years, the cost of that fee is substantial.

When You Actually Benefit From Professional Help

That said, there are situations where professional guidance is genuinely worth it. Not commission-driven product sales. Not AUM-fee portfolio management. Actual planning expertise.

Consider a fee-only advisor if any of these apply:

- You inherited an IRA. The SECURE Act 10-year distribution rules are genuinely complicated and the tax planning around them benefits from professional modeling.

- You inherited real property in multiple states. Each state has its own rules around basis, transfer taxes, and probate.

- The estate is large enough to be close to the estate tax exemption. The federal exemption is $13.61M per person in 2026 but is scheduled to revert to approximately $7M in 2026 when the TCJA provisions sunset. This creates planning implications.

- You are thinking about large charitable giving. Qualified charitable distributions, donor-advised funds, and charitable remainder trusts have specific mechanics worth getting right.

- You have a complex existing financial picture. Significant existing investments, a business, equity compensation, or multi-state tax situations interact with an inheritance in ways that benefit from integrated planning.

- You are considering major financial changes in the next 24 months. Paying off a mortgage, changing jobs, moving states, funding children's college. These interact with inherited assets in ways worth modeling.

The common thread: you need help when the decisions have meaningful tax or legal complexity that a simple index portfolio approach doesn't address. Not because you can't understand the portfolio. But because the tax and estate planning layer benefits from someone who does it professionally.

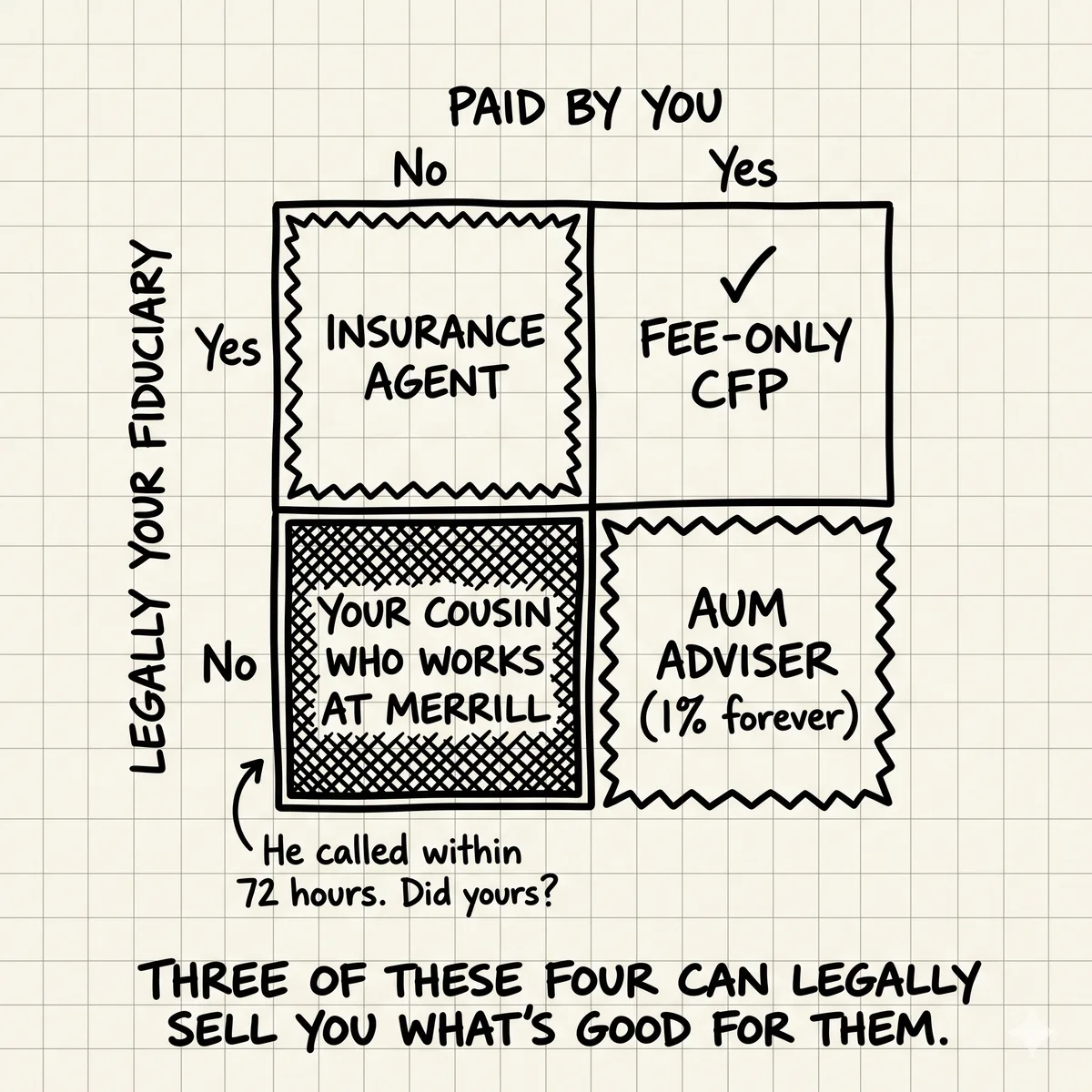

The Critical Distinction: Fee-Only vs. Commission-Based

This distinction matters more than almost anything else when hiring a financial professional.

Commission-based advisors

This includes broker-dealers, insurance agents who offer "financial planning," and many bank-based advisors. They earn money when you buy products. Life insurance. Annuities. Actively managed mutual funds with sales loads. The product may or may not be appropriate for you. They have a legal obligation to recommend products that are "suitable," which is a lower standard than "in your best interest."

Many of the advisors who called you are in this category. Their pitch may be excellent. The products they recommend may even be fine. But you cannot know whether the recommendation is driven by your best interest or their compensation structure without asking specifically.

AUM-fee advisors (Registered Investment Advisors, "RIAs")

These advisors charge a percentage of assets under management, typically 0.5% to 1.5% per year. They are registered as fiduciaries with the SEC or state regulators, which means they have a legal obligation to act in your best interest. They are generally better than commission-based advisors. But their fee is ongoing and substantial.

An AUM fee of 1% on $3M is $30,000 per year forever. The better RIAs earn this through comprehensive financial planning, tax coordination, and behavioral coaching during volatile markets. The worse ones are essentially paying for index funds while charging active management fees. Ask specifically what you get for the fee beyond portfolio management.

Fee-only advisors (the category worth seeking)

Fee-only advisors charge flat fees or hourly rates. They do not earn commissions on products. They do not earn a percentage of assets. They charge you directly for advice, the same way a lawyer or accountant does.

A comprehensive financial plan from a fee-only CFP might cost $3,000 to $8,000 as a one-time engagement. An ongoing relationship might cost $5,000 to $15,000 per year flat. These numbers are large in absolute terms. Relative to 1% of $3M every year forever, they are often much smaller.

The important nuance: "fee-only" is a specific term. "Fee-based" is different. Fee-based advisors charge fees and also earn commissions. Ask explicitly: "Do you receive any compensation other than what I pay you directly?" A fee-only advisor's answer is no. If the answer is anything else, they are not fee-only.

Where to Find Fee-Only Advisors

Three networks are worth knowing:

- NAPFA (napfa.org). The National Association of Personal Financial Advisors. All members must be fee-only fiduciaries. The search tool lets you filter by specialty including estate planning and sudden wealth.

- Garrett Planning Network (garrettplanningnetwork.com). Specifically designed for people who want hourly or project-based advice rather than ongoing relationships. Good for the person who wants a plan done well and then wants to manage it themselves.

- XY Planning Network (xyplanningnetwork.com). Focuses on younger advisors who often work with clients in the 30-50 age range. Many specialize in sudden wealth events.

When you contact them, ask three questions in the first call:

- "Are you fee-only? Do you receive any compensation other than what I pay you directly?"

- "Do you work with clients who have recently inherited money? What does that engagement typically look like?"

- "What would a comprehensive plan for my situation cost, and what does it include?"

The answers tell you a lot. A good advisor will be clear on the first question, specific on the second, and transparent on the third. An advisor who pivots quickly to "let me understand what you have" before answering those questions is putting the sales conversation before the disclosure conversation.

What NettWorth Is (and Is Not)

We want to be direct about this: NettWorth is not a substitute for a CFP. A good fee-only financial planner gives you personalized advice, tax modeling, estate planning coordination, and a relationship over time. That is a different product than what we are building.

What NettWorth provides is financial clarity and memory. A place to organize your full picture (inherited accounts, existing accounts, real property, tax basis), model scenarios, and think clearly without someone's sales calendar in the room. It is a thinking tool that makes you a better client for a fee-only advisor if you hire one, and a more informed self-directed investor if you don't.

The framing we use internally: you're not trusting us with your money, but with the analysis that helps you make the decisions on what to do with it. That's a different kind of relationship than an advisor wants with your assets. We think both can coexist.

The advisors who called you from the obituary? You probably don't need to call them back.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

The Expat Financial Checklist: What Mid-Senior Professionals Get Wrong Before They Relocate

Everyone checks the cost-of-living calculator and the school ratings. Almost nobody reviews the financial decisions that need to be made before they leave — the ones with hard deadlines that disappear when the moving truck arrives.

Concentrated Tech Equity: The Diversification Decision (With Math)

Your advisor says diversify. But diversification has a real cost. Here is the math on when holding wins, when selling wins, and what wealthy founders actually do.

How to Actually Invest an Inheritance (Without a Finance Degree)

Low-cost index funds outperform most actively managed alternatives over any 15-year period. The three-fund portfolio and target-date funds are not cop-outs — they are the approach most economists would actually use. Here's the jargon-free version.