Before You Move to the US from India: The Financial Checklist Your CPA Won't Give You

Preethi got her H-1B approval in March. She was already in San Jose by September, scanning apartments on Zillow and calculating commute times to her new office. She'd done most things right. She'd asked her Indian CA to close out accounts she didn't need anymore. He told her she could keep the NRE account — it was tax-free in India, no problem. She kept it. Six months after landing, her US CPA pulled up her return and asked about the NRE interest income. Preethi said there was nothing to report, the NRE was tax-free. The CPA didn't disagree with the word "tax-free." She just pointed out that "tax-free" means something different depending on which side of the Pacific you're asking.

NRE interest is exempt from Indian income tax. That exemption belongs to Indian residents and NRIs. From the moment Preethi became a US resident alien, she stopped being an NRI for US tax purposes. The interest was now US-taxable income. The account hadn't changed. The rules had.

Nobody had told her the rules changed the day she arrived.

The logistics of a move are straightforward. The financial decisions have deadlines that most people miss because nobody tells them the deadline exists.

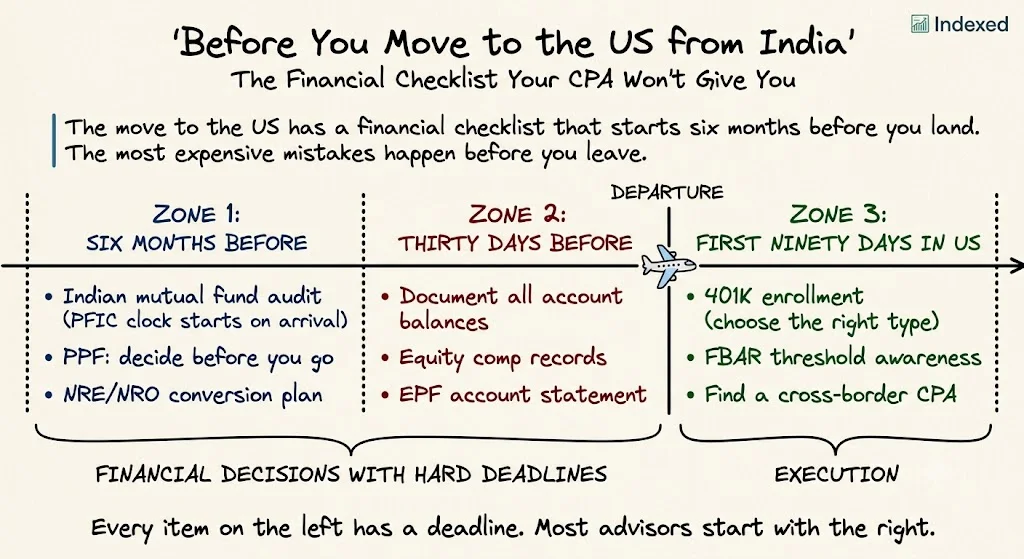

Three phases, three sets of decisions. The financial deadlines the moving checklist won't mention.

Six Months Before Your Flight

Indian Mutual Fund Audit

Pull up your Indian mutual fund portfolio. Every fund on that list — SBI Blue Chip, HDFC Midcap, any ELSS fund, any index fund — is a Passive Foreign Investment Company (PFIC) the moment you become a US tax resident. That's the IRS classification for foreign investment vehicles, and it comes with punitive tax treatment.

The default PFIC tax regime taxes excess distributions and gains at ordinary income rates, then adds an interest charge on top. Not capital gains rates. Ordinary income, plus interest. On a fund you may have held for ten years.

You have three options: sell the funds before you become a US resident alien; elect mark-to-market treatment (which requires annual reporting and treats unrealized gains as income each year); or elect Qualified Electing Fund (QEF) status. The QEF election requires the fund to provide specific annual information statements. Most Indian mutual fund houses do not provide these statements. In practice, QEF is not available for most Indian funds.

The decision: make it before you board the flight.

Once you become a US resident alien, selling Indian mutual funds is still possible but you're now inside the PFIC regime. Selling before residency starts keeps you in standard capital gains territory under Indian law. Selling after residency starts triggers PFIC rules. The cost of waiting is not small.

PPF Decision

The Public Provident Fund is one of the best instruments the Indian tax system offers. Tax-free contributions. Tax-free growth. Tax-free maturity proceeds. All three exemptions apply to Indian residents and NRIs investing in Indian accounts.

Here is what changes when you become a US resident alien: the interest accruing in your PPF each year is US-taxable income. You cannot withdraw it. It is locked up for the remaining term of the account. But the IRS expects you to report it as income in the year it accrues.

The maturity proceeds: there is no settled US tax guidance on whether PPF maturity proceeds are US-taxable for returning residents who held the account during their US residency period. The conservative position is that the growth attributable to US-residency years is taxable.

The decision: continue contributing (accepting annual US tax on interest you cannot access, in exchange for the Indian tax-free maturity benefit) or stop contributions for the duration of your US stay. If you're young and your PPF has many years left, a cross-border CPA should model both paths for your specific situation. There is no universal answer.

NRE/NRO Account Restructuring Plan

Your NRE account holds foreign earnings repatriated to India. Interest on NRE accounts is exempt from Indian income tax. Your Indian bank knows this. Your Indian CA knows this. Neither of them has to care what the IRS thinks.

The IRS thinks this: you are a US resident alien, which means your worldwide income is US-taxable, including NRE interest. The Indian tax exemption does not carry over. It does not appear in the US-India DTAA in a way that makes the interest US-exempt. From day one of US residency, the NRE interest is income you owe the IRS.

This is not a reason to close the NRE account. You remain an NRI for Indian purposes (the H-1B is a non-immigrant visa; you are not an Indian tax resident while in the US). Your NRE account can stay. You just need to know that the interest becomes US income from the date you arrive. Report it. Include it in your first US return.

The NRO account is different. NRO accounts hold Indian-source income — rent from a flat you own, Indian dividends, salary paid before you moved. Once you're a US resident, NRO income you deposit is US-taxable. Indian TDS on NRO income generates a foreign tax credit you can use to offset some of the US liability, but the paperwork is not trivial. Talk to a cross-border CPA about whether to reduce NRO activity while you're in the US.

Thirty Days Before Departure

Document All Indian Account Balances

FBAR — the Report of Foreign Bank and Financial Accounts (FinCEN Form 114) — requires you to report the maximum balance in each foreign account at any point during the calendar year. The threshold is $10,000 aggregate across all foreign accounts combined at any single moment.

Your first FBAR as a US resident covers January 1 to December 31 of your first full calendar year in the US. But if you arrive mid-year, your partial year may also trigger FBAR if your Indian balances crossed $10,000 at any point after you became a US resident alien.

Before you leave: take screenshots or download statements showing the balance in every Indian account. NRE, NRO, any savings account, your EPF, any brokerage accounts. You need the maximum balance date and amount, not just the current balance. This documentation will be necessary when you file your first FBAR (due April 15 of the following year, with automatic extension to October 15).

Collect Equity Compensation Documents

If your new US employer is giving you RSUs or options, your vesting schedule and grant agreements will matter for tax purposes. If your Indian employer gave you equity that is still unvested, those documents matter even more — the sourcing allocation between India and US workdays will determine how much the US can tax each vest.

Gather grant agreements, vesting schedules, and any documentation of your Indian employment dates. Your US CPA will ask for this information and "I think it was around 2023" is not a sufficient answer for RSU sourcing calculations.

EPF Status

The Employees' Provident Fund is treated as a pension under Indian law, with full tax exemption on contributions, growth, and qualifying withdrawals. The IRS has not issued clear guidance classifying EPF as a qualified foreign pension plan.

The conservative and widely-used position among cross-border tax practitioners: the interest accruing in your EPF each year is US-taxable ordinary income. Not at withdrawal. As it accrues. You report it annually even if you haven't touched the account. Most NRIs currently in the US have never done this, which is a separate problem to address with professional guidance.

Before you leave: document your EPF balance, the contribution history, and the annual interest credited. The more documentation you have for your first US tax filing, the fewer problems you encounter later.

Your First Ninety Days in the US

401K Enrollment

H-1B holders are eligible to participate in employer 401K plans. You are not excluded by visa status. Enroll as soon as your employer's eligibility period allows.

The Roth vs. Traditional decision has a specific, non-obvious answer for someone who might return to India.

The US-India DTAA covers pensions and annuities (Article 20). Traditional 401K distributions for Indian residents are taxable in India, with credit given for US withholding. The effective India tax rate after the DTAA credit is lower than the full Indian marginal rate. This mechanism works because the US withholds tax on Traditional distributions, and India credits that withholding against what it charges.

Roth 401K distributions: the US withholds nothing (qualified distributions are tax-free in the US). India has no specific treaty provision recognizing Roth accounts as tax-exempt. India sees a distribution from a foreign retirement account and taxes it as ordinary income. There is no US withholding to credit. You get no DTAA offset. If you return to India after RNOR status expires, every Roth distribution is taxed at the full Indian marginal rate with no credit mechanism.

The 401K decision if you might return to India

Traditional 401K wins if you return to India after RNOR status. You deferred US tax going in. India taxes distributions, but credits US withholding. Net effective rate is lower than Roth, which offers no DTAA credit. If you stay permanently in the US, Roth may win. The decision depends on which country you expect to retire in — and the answer is often "I don't know yet," which is a reason to model both rather than default to the standard US advice.

The RNOR window (the 2-3 years after you return to India where foreign income is largely exempt) is the exception: Roth distributions taken during RNOR may be tax-free in India. If you have a concrete return timeline within the next decade, that timing conversation belongs in your first meeting with a cross-border CPA, not your last one.

FBAR Awareness

Your first FBAR as a US resident covers the period from when you became a US resident alien through December 31 of that calendar year. The rule: if your foreign accounts had an aggregate balance of $10,000 or more at any point during the year, you must file.

Your NRE account counts. Your NRO account counts. Any Indian savings account counts. Your EPF balance counts. Add them together, not separately. If the combined balance touched $10,000 at any point in the year — including before you arrived, if that year was a partial-year residency — you file.

FBAR is filed separately from your tax return. It goes to FinCEN (the Financial Crimes Enforcement Network), not the IRS. The due date is April 15, with an automatic extension to October 15. The penalty for willful non-filing is significant. The penalty for non-willful non-filing is lower, but still real. File it.

Indian Mutual Funds You Kept

If you decided to keep Indian mutual funds and accepted the PFIC burden, you are now inside the reporting regime. Document two things: the date you became a US resident alien, and the fair market value of each fund on that date. This is your PFIC entry basis.

You will need Form 8621 for each PFIC you hold. If you chose mark-to-market, you report unrealized gains (or losses) annually. If you are in the default regime, excess distributions are calculated when you eventually sell.

The number that matters most is the value on the date you became a US resident. If you didn't capture it then, try to reconstruct it from fund NAV history. NAV data for Indian funds is publicly available through AMFI (Association of Mutual Funds in India). Get the number.

Preethi paid tax on the NRE interest. Not a catastrophic amount — the account wasn't huge and she'd only been in the US for part of the year. But she paid it retroactively, with a penalty, because nobody had told her in advance. Her CA had told her the account was fine. He was right, for India. For the US, from day one, it was income.

The financial decisions in this checklist are not complicated once you know they exist. The problem is not complexity. The problem is that the people who tell you to open the NRE account, contribute to the PPF, and grow the mutual fund portfolio are working under a different tax system than the one that applies to you from the moment you land.

The rules didn't fail Preethi. The handoff did. No one told her the rules had changed.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

Traditional 401K or Roth 401K When You Might Move Back to India? The Math Most H-1B Holders Never See

Meera maxed her 401K every year for seven years. Then a colleague mentioned something: India taxes 401K distributions as ordinary income. She'd assumed the tax treaty covered it. It does — but not the way she thought. The treaty prevents double taxation. It doesn't prevent Indian taxation. And Roth 401K is worse.

Your First 90 Days in the US from India: The Financial Decisions Nobody Briefs You On

Dev had $35,000 in SBI Blue Chip and HDFC Top 100 when he landed at SFO on an H-1B. Fourteen months later his CPA asked if he'd filed Form 8621. He hadn't heard of it. Three decisions — PFIC elections, FBAR filing, and Roth vs. Traditional for someone who might return to India — needed to happen in the first 90 days. Nobody told him.

The H-1B Financial Playbook: What the Tax Firms Cover and What They Leave Out

Your CPA files FBAR and reports your RSU income. What they don't do is tell you whether you're in the wrong 401K type for your actual retirement country, why your Indian mutual funds are classified as PFICs, or what your unvested equity does to your tax bill if you leave. Three problems. All connected. None of them compliance.