Your First 90 Days in the US from India: The Financial Decisions Nobody Briefs You On

Dev landed at SFO on a Tuesday. He had his H-1B approval, a sublet in Sunnyvale, and first day at Google on Monday. He had about forty things on his list. "Review Indian mutual fund holdings for PFIC classification" was not one of them.

He found out about PFIC fourteen months later, when his US CPA asked if he had any foreign mutual funds.

He said yes. About $35,000 in SBI Blue Chip and HDFC Top 100.

His CPA went quiet for a moment. Then: "How long have you had these since becoming a US resident?"

Fourteen months.

"And you haven't filed Form 8621?"

No. He didn't know what Form 8621 was.

The CPA walked him through it. PFIC stands for Passive Foreign Investment Company. Indian mutual funds qualify. When you become a US tax resident, foreign mutual funds you hold get reclassified under a specific IRS regime. The default tax treatment is punitive: gains and distributions are taxed as ordinary income, not capital gains, and the IRS charges an interest penalty on top of that. The way to avoid the worst of it is to make a Mark-to-Market election in the first year. Dev had missed that window.

He hadn't done anything wrong in the sense that most people understand wrong. He hadn't hidden assets. He hadn't filed falsely. He just hadn't known to ask, and nobody had told him.

His HR team had been thorough on the US-side checklist. 401K enrollment, benefits, direct deposit, state income tax withholding. All of it. Nobody had thought to ask what he was leaving behind.

The first ninety days in a new country consume everything. The financial decisions that matter most are the ones you don't know to ask about.

This is what the checklist looks like for someone arriving from India on an H-1B or L-1.

The accounts you already have: what changed when you landed

You become a US resident alien for tax purposes when you meet the substantial presence test: 183 days in the US in a given year, calculated with a specific formula that weights the prior two years. For most H-1B holders who arrive mid-year, the first US tax year is a dual-status year. You are a nonresident for part of the year and a resident for the rest. Filing it correctly requires a specific form and attachment that most CPAs do not flag proactively.

That status change has immediate consequences for the Indian accounts you've held for years.

NRE accounts

NRE interest is tax-free in India when you're an NRI. That rule applies to Indian tax law. It does not apply to the US. From the day you begin accumulating days toward substantial presence as a US resident alien, NRE interest is US-taxable as ordinary income. Most people don't find this out until their first US tax return, when the CPA asks for foreign income and they say the NRE interest was tax-free. It was. In India. Not here.

PPF

Contributions to PPF are allowed while you're an NRI. The annual interest your PPF earns, however, is US-taxable income in the year it accrues. Even though you cannot withdraw it. Even though it's sitting in a locked account in India that you can't touch for years. The IRS taxes it the year it accrues. The tax treatment of PPF maturity proceeds under the US-India Double Tax Avoidance Agreement is unsettled. The conservative position, and the one most cross-border CPAs take, is that a portion is taxable.

EPF

If your EPF is still accruing interest, that interest is US-taxable income annually. The IRS has not classified EPF as a qualified foreign pension plan. That classification matters because qualified pension plans get deferred treatment. EPF does not qualify. The interest accrues, the US wants to tax it, and most NRIs in the US have never reported it.

None of these require immediate action in week one. But they require a conversation with a cross-border CPA before you file your first US return. The gap between "I'll deal with it at tax time" and "I filed incorrectly for two years" is smaller than people expect.

The mutual funds: PFIC and why it matters now

This is the one most people miss. And the one with the most lasting consequences.

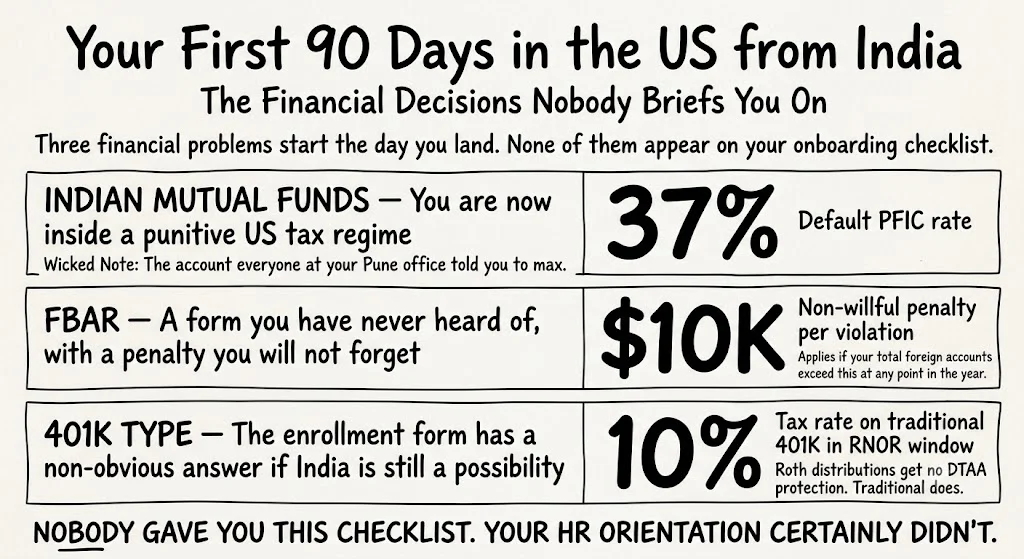

PFIC stands for Passive Foreign Investment Company. An Indian mutual fund is almost certainly a PFIC. Equity funds, ELSS funds, debt funds, hybrid funds. If you hold shares in an Indian mutual fund and you are now a US tax resident, you hold a PFIC.

Fixed deposits are not PFICs. NRE savings accounts are not PFICs. Those are bank instruments. Mutual funds are the issue.

Why does it matter? Because the IRS applies a specific, punitive tax treatment to PFIC gains and distributions by default. When you eventually sell or receive a distribution, the gain is taxed at ordinary income rates, not long-term capital gains rates. And the IRS charges an interest penalty on deferred income going back to the year the gain accrued.

PFIC: the three elections

You have three options for how PFICs are taxed. Each must be elected on Form 8621, filed with your return.

- Default (excess distribution): No election needed, but the worst outcome. Gains and distributions taxed at ordinary income rates plus an interest charge going back to the year the income accrued.

- QEF (Qualified Electing Fund): You include your share of the fund's ordinary income and capital gains each year. Requires the fund to provide a PFIC Annual Information Statement. Indian fund houses almost never provide this. For most H-1B holders arriving from India, this election is not practical.

- Mark-to-Market (MTM): You recognize the change in the fund's fair market value each year as ordinary income or loss. No interest charge. No excess distribution regime. The practical option for most people who decide to keep their Indian mutual funds. Must be elected in the first year you hold the fund as a US resident.

The MTM election is the practical choice for most H-1B holders who want to keep their Indian mutual funds. You report the annual gain or loss as ordinary income each year. It's not ideal from a tax rate perspective, but it avoids the interest-charge regime that makes the default treatment so painful.

The other practical choice is to sell before you trigger US tax residency, or very shortly after arriving. If you sell while you're still a nonresident, you pay Indian capital gains tax only. No PFIC issues. No Form 8621. The problem goes away.

Most people don't know to make this choice. They hold the funds because they've always held the funds. Then they're four years in, the funds have appreciated, and they're looking at a PFIC problem that could have been avoided.

Dev's SBI Blue Chip had been growing for four years before anyone told him about PFIC. His options at that point were substantially worse than his options in month one.

The 401K question you'll face in week two

Most H-1B employers offer 401K enrollment in the first 30 to 90 days. You'll get an email from Fidelity or Vanguard asking you to make an election.

The generic advice is Roth if you're young and expect higher income later. Traditional if you're in a high bracket now and expect lower income in retirement. That advice was written for someone whose retirement will happen in the US.

If you might return to India, the calculation changes.

The US-India DTAA has no specific provision for Roth IRA or Roth 401K. India does not recognize the Roth wrapper. If you take Roth distributions after returning to India, India may tax those distributions as ordinary income. The tax-free treatment you paid for by contributing after-tax dollars may not survive the border.

Traditional 401K distributions are taxable in the US as ordinary income, with mandatory withholding. India taxes them as well, with a foreign tax credit for US withholding. If you distribute during the RNOR window, the two-year period after returning to India when foreign-sourced income is often tax-exempt, the math can work out significantly better. The strategy requires coordination between a US and Indian tax advisor. But the starting point is: Roth is not obviously better for someone whose retirement jurisdiction is uncertain.

The one thing that's not complicated: the employer match

Take it. Every time. A 50% or 100% instant return on the first few percent of contribution is the highest guaranteed return available to you in the US financial system, regardless of your eventual distribution situation. The Roth vs. Traditional question matters. The match question does not.

FBAR: the form you've never heard of that has a $10,000 penalty for not filing

Most H-1B holders don't know FinCEN 114 exists until their first US CPA brings it up. Some CPAs don't bring it up. That's the problem.

FBAR stands for Report of Foreign Bank and Financial Accounts. It's filed separately from your tax return, electronically, through the BSA E-Filing System. It's not an IRS form. It's a Financial Crimes Enforcement Network form. That distinction confuses people and creates the gap.

FBAR: who files, what counts, what it costs to miss it

Who files: US persons, including resident aliens. You become a US person for FBAR purposes when you establish US tax residency. That includes H-1B holders who meet the substantial presence test.

The threshold: Aggregate value of all foreign financial accounts exceeds $10,000 at any point during the calendar year. Not the year-end balance. Any single day during the year.

What counts: NRE accounts, NRO accounts, FCNR accounts, savings accounts, fixed deposits, demat accounts that hold securities, EPF if you have signing authority. When in doubt, err toward disclosure.

When it's due: April 15, automatically extended to October 15 with no action required. No paper form. Electronic filing only via the BSA E-Filing System at fincen.gov.

The penalty: Non-willful failure to file is up to $10,000 per account per year. Willful failure is up to $100,000 or 50% of the account balance, whichever is greater, per year. The IRS has collected these penalties from people who genuinely didn't know.

The most common pattern: someone arrives on H-1B, has three Indian accounts, each with balances well above $10,000, files their US taxes for two years without mentioning FBAR, then gets a new CPA who looks at the situation and has to figure out how to fix two years of non-filing.

The IRS has a streamlined filing compliance procedure for non-willful failures. It allows you to catch up with reduced penalties. But the process is not free, not simple, and not quick. Filing correctly in year one is significantly better than fixing two years of non-filing in year three.

If you arrived in the US and your Indian accounts had more than $10,000 in aggregate at any point during the year, FBAR is probably required. Get this on your CPA's radar before April 15 of your first US filing year.

Your HR team handles the US setup. These three problems start the day you land — and nobody briefs you on them.

The 90-day sequence

Days 1 through 30: open US checking and savings accounts, enroll in benefits, set up a credit card to begin building US credit history. Don't make any major moves on Indian accounts yet. You need a cross-border CPA before you change account structures.

Days 31 through 60: evaluate your Indian mutual fund exposure. Look at what you hold. Determine whether each fund is a PFIC (mutual funds are; FDs are not). Understand what liquidating before your US residency triggers vs. holding and filing Form 8621 with the MTM election would look like. This is the decision with the longest tail. Making it in month two, rather than month fourteen, gives you options.

Days 61 through 90: get a cross-border CPA on board, ideally one who handles both US and Indian tax. Walk them through your Indian accounts: NRE, NRO, PPF, EPF, any mutual funds you've decided to keep. Confirm FBAR requirements. Understand your dual-status filing obligations for the first year. Get the MTM election decision documented before your first US tax return is due.

By day 90, you should know your Indian account situation. That knowledge doesn't require action on everything immediately. It requires a plan.

Dev sold his SBI Blue Chip and HDFC Top 100 funds six weeks after he found out about PFIC. He paid Indian capital gains tax on the proceeds. He filed Form 8621 for the fourteen months he'd held the funds as a US resident, using the default excess distribution regime because the MTM window had closed. It was not catastrophic. It was substantially more expensive than if he had made the decision in month one.

The next 90 days after that were the first 90 days where he actually knew what his financial picture looked like. Both sides of it.

The question nobody asks when they land is: what did arriving here do to the accounts I already had? The answer has a 90-day window for most of the decisions that matter.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

Before You Move to the US from India: The Financial Checklist Your CPA Won't Give You

Preethi kept her NRE account when she moved to San Jose — her Indian CA said it was tax-free. It is, in India. From the day she became a US resident alien, the interest was US income. Three decisions have hard deadlines before your flight: your Indian mutual funds (likely PFICs the moment you land), your PPF contribution strategy, and the Roth vs. Traditional 401K choice that has a specific non-obvious answer if you might ever return to India.

Your H-1B Is In Transfer. You Have 60 Days. Here Is What To Do With Your Money.

Kevin got the layoff message Thursday at 4pm. He called his immigration attorney immediately. He didn't call anyone about his financial situation. Six months later: a corrected W-2 with 30% NRA withholding on RSUs he hadn't known had accelerated. The 60-day grace period is also a financial window. Nobody told him.

Leaving the US for the UK: The Financial Decisions That Have Hard Deadlines Before Your Flight

Olivia landed in London on a Sunday and started work on Monday. Week seven: she found out about the UK's Foreign Income and Gains regime — introduced April 2025, exempts foreign income from UK tax for four years, must be elected in the first UK tax year. She'd missed the 30-day window by five weeks. This is what she should have known before she boarded the flight.