Your H-1B Is In Transfer. You Have 60 Days. Here Is What To Do With Your Money.

The 60-day grace period is an immigration countdown. It's also a financial window with specific decisions that close permanently when the clock runs out.

The message came on a Thursday at 4pm: position eliminated, effective immediately, 60-day grace period per USCIS regulations. Kevin had seen the warning signs and hadn't moved. He called his immigration attorney. He didn't call anyone about his financial situation.

By day 45, he had a new sponsor. The H-1B transfer was filed. He felt like he'd made it through. Six months later, a letter arrived from his former employer: a corrected W-2, with supplemental withholding applied to an RSU acceleration event he hadn't known about. His unvested shares had accelerated on termination per the plan terms. His employer had withheld at the non-resident alien rate. He'd never sold them, never knew they'd vested, and now owed tax on income he hadn't realized was income.

Nobody had told Kevin the 60-day window was a financial window.

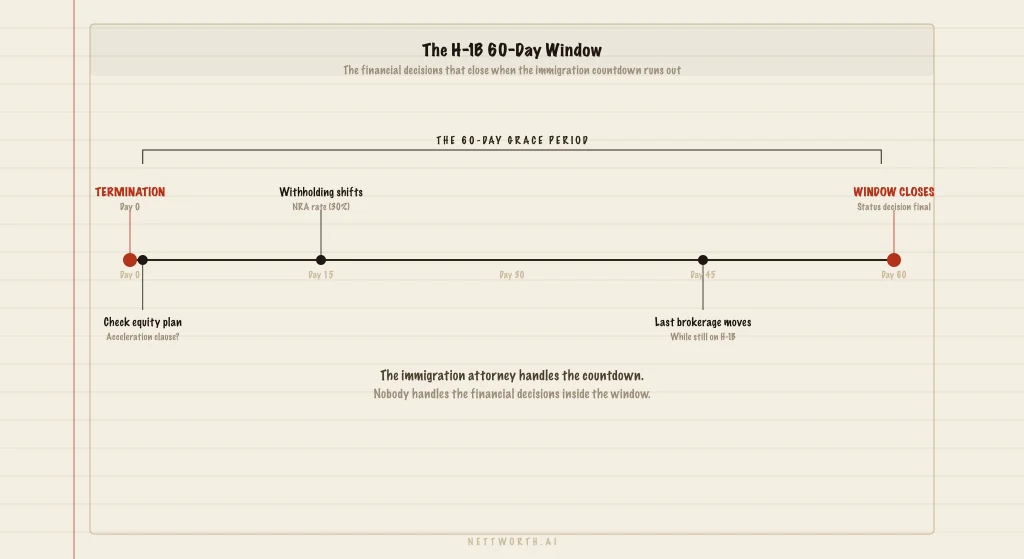

What the Grace Period Actually Is

When an H-1B holder's employment terminates, USCIS provides a 60-day grace period during which the person can stay in the US. The purpose is to allow time to find new sponsorship, change to another visa category, or prepare to depart. It is not a period of authorized employment. It is a period of authorized presence.

From an immigration perspective, the goal is straightforward: find a new employer and file the H-1B transfer before day 60, or leave. Most people focus entirely on this. The financial clock is running simultaneously and is almost entirely ignored.

The financial window has four components, each with a different deadline: equity decisions, HSA/COBRA decisions, 401K decisions, and the departure-vs-stay bifurcation that affects everything else.

Equity: The Decision That Has Already Been Made for You

The first thing to check when you receive a termination notice is your equity plan documents. Not the grant agreement. The plan document itself, which governs what happens to unvested shares on employment termination.

Three scenarios exist, and which one you're in determines everything:

Scenario 1: Unvested shares are forfeited on termination. This is the most common outcome. Your unvested RSUs disappear. The question becomes what to do with any vested-but-unsold shares before your tax residency status potentially changes.

Scenario 2: Unvested shares accelerate on termination (triggered acceleration). Some plans — particularly at larger tech companies — have provisions that vest unvested shares immediately on termination without cause. If this applies to your plan, those shares vested the moment your employment ended. Your former employer may report this as income on a corrected W-2. If they updated your tax status to non-resident alien before processing the final payroll, they may have withheld at 30% rather than your marginal rate.

Scenario 3: Post-termination exercise window (stock options). If you hold unexercised options rather than RSUs, the plan defines a post-termination exercise window — typically 90 days for incentive stock options (after which they convert to non-qualified), and potentially longer for non-qualified stock options. The 60-day grace period may not align with this window. Act on options decisions immediately, not at day 59.

The non-resident alien withholding trap

If your former employer processes final equity payroll after updating your employment status, they may apply 30% NRA withholding to any accelerated or vested equity income. This rate is higher than the supplemental withholding rate (22%) and can be significantly higher than your actual marginal rate on a Form 1040. If this happened to you, you can potentially recover the over-withholding by filing correctly and establishing your resident alien status for the tax year. But you need to know it happened first. Check any W-2 corrections you receive after termination.

Vested Shares: Sell Now or Not?

If you have vested but unsold shares, the 60-day window is the period when you're still a US tax resident. Selling within that window means capital gains rates apply — 15% or 20% depending on your income level. If you find new sponsorship and remain in the US, this decision is less urgent. If there's any possibility you depart the US, it becomes significant.

Non-citizens who become non-resident aliens pay 30% US withholding on proceeds from selling US securities. This withholding applies to gross proceeds, not to gains. If you're holding $200K in vested shares with a basis of $150K, the gain is $50K — but the 30% withholding at point of sale applies to the $200K, meaning $60K is withheld. You recover the excess by filing, but the cash impact at point of sale is jarring.

US citizens are exempt from the 30% withholding rule regardless of residency. If you're a US citizen on an H-1B (which is uncommon but possible), this specific concern doesn't apply to you.

HSA: The Deadline Nobody Mentions

If you had employer-sponsored health coverage tied to an HSA-eligible high-deductible health plan, your coverage ends on termination. You have 60 days to elect COBRA continuation coverage. Missing the COBRA window permanently closes it.

Why this matters: HSA contributions can continue during COBRA coverage, as long as the underlying plan is HSA-eligible. If you maintain COBRA and remain HSA-eligible, you can continue making HSA contributions during the grace period. These contributions are tax-deductible regardless of your employment status.

What to check: Is your employer's COBRA HDHP plan HSA-eligible? Not all HDHPs qualify. Some employer plans layer on benefits that disqualify the plan for HSA purposes. If the plan is eligible, elect COBRA for the HDHP option specifically and continue contributing.

The 2026 HSA contribution limits: $4,300 for self-only coverage, $8,550 for family coverage. If you're in the second half of the year and haven't maxed, the grace period is the last window to catch up on contributions before your coverage situation changes.

401K: Don't Rush This One

Your 401K stays where it is after termination. You cannot contribute to your former employer's plan after your last paycheck, but you don't have to roll it immediately. The account continues to grow tax-deferred. You have options: leave it in the former employer's plan (if the plan allows it, which most plans do for balances above $5,000), roll it to an IRA, or roll it to a new employer's plan once you have one.

Do not cash it out. The 10% early withdrawal penalty applies if you're under 59.5, plus the distribution is ordinary income. On a $280K balance, a cash-out would cost roughly $90K+ in taxes and penalties. This is almost never the right move.

The rollover question can wait until you've resolved your visa situation. If you're successfully transferred to a new employer within 60 days, evaluate the new employer's plan before deciding. If you end up departing, the 401K decision becomes part of the pre-departure planning (covered in the RNOR window planning post for India returnees).

The involuntary separation exception

If you were laid off (involuntary termination) and you're 55 or older in the year of separation, you may be eligible for the "rule of 55" exception to the early withdrawal penalty from your former employer's 401K — but not from an IRA rollover. This is a narrow exception but meaningful for a specific age group. If you roll the 401K to an IRA before evaluating this, you lose the exception. Check your age and the plan terms before rolling.

The New Employer's Equity Plan: Read It Before You Sign

When you find new sponsorship and receive an offer, the equity component typically includes an unvested RSU or option grant. The key documents: the equity plan and the grant agreement. Read them before you accept.

Two specific questions to answer:

Does the plan have a US residency requirement? Some equity plans require continued US residency as a condition of vesting. If your visa renewal fails in year two and you have to leave, do you forfeit unvested shares you were counting on?

What happens to unvested shares on termination? The cycle you just went through — termination, uncertain status, urgent decision-making — will likely recur at some point. Knowing the answer before you accept the next job is better than discovering it during the next grace period.

If You're Departing: The Dual-Status Filing Complication

If the 60-day period ends without new sponsorship and you depart the US voluntarily, your tax situation for that year becomes a dual-status return. You were a resident alien from January 1 through your last day of US presence, and a non-resident alien from departure through December 31.

Dual-status returns are more complex than either a full-year resident or a full-year non-resident return. Some deductions available to full-year residents are unavailable on the dual-status return. The standard deduction doesn't apply to the non-resident portion. If you have income from both periods, it may be reported differently depending on its character and source.

The filing itself: Form 1040 for the resident period, with a Form 1040-NR as a statement for the non-resident period (or vice versa depending on the specific guidance). Most CPAs handle this correctly, but fewer than you'd expect ask about the specific departure date and whether a dual-status situation applies. Flag it explicitly.

The Day-by-Day Priority Sequence

Days 1-3: Pull your equity plan document and grant agreements. Determine which scenario applies (forfeiture, acceleration, or exercise window). If acceleration, identify what income was reported and what withholding was applied. Call your CPA — the corrected W-2 may arrive months later, but the facts are happening now.

Days 1-10: Evaluate vested shares. If there's any chance you might depart the US, consider whether to sell now while you're still a resident. Contact your brokerage and confirm the process. Don't wait until day 55 to start this.

Days 1-60 (COBRA deadline): Elect COBRA if you want to maintain HSA-eligible coverage. The letter arrives by mail from your former employer or their COBRA administrator. The window is 60 days from the date of coverage loss (typically the last day of the month in which your employment terminated). Missing it is permanent.

Days 10-45: Focus on immigration resolution. The financial decisions above are parallel, not sequential — they don't wait for the visa situation to resolve.

Days 45-60: If transfer is filed and you're staying, confirm new employer benefits enrollment timing, evaluate 401K rollover vs. hold decision, and review new offer equity terms. If you're departing, begin pre-departure financial preparation — state tax residency, brokerage access from abroad, 401K decision.

Kevin's situation was recoverable. The corrected W-2 with NRA withholding was painful but fixable — he filed correctly, the over-withholding was recovered as a refund, and the accelerated shares had cost him in taxes but not destroyed anything. What he said afterward: "I wish someone had told me on day one that there was a financial checklist running parallel to the immigration checklist. I would have handled it differently."

The immigration attorney is the right call on day one. So is the CPA.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

Your First 90 Days in the US from India: The Financial Decisions Nobody Briefs You On

Dev had $35,000 in SBI Blue Chip and HDFC Top 100 when he landed at SFO on an H-1B. Fourteen months later his CPA asked if he'd filed Form 8621. He hadn't heard of it. Three decisions — PFIC elections, FBAR filing, and Roth vs. Traditional for someone who might return to India — needed to happen in the first 90 days. Nobody told him.

Leaving the US for Singapore With RSUs: Why 'No Tax Treaty' Is the Detail Everyone Misses

Alex said yes to the Singapore offer on a Tuesday. Six months in, a W-2 arrived showing $200K in income he didn't understand. His employer had sourced the RSU vesting period correctly — US workdays divided by total vesting days. The US taxes that portion regardless of where you live at vest. Singapore has no income tax treaty with the US. There is no protective mechanism.

Before You Leave the US for India: The RNOR Window, the 401K Decision, and Everything Else

Vikram had spent 11 years at Microsoft. He knew about the RNOR window — he found out about it 14 months after returning to Pune. The first two 401K distributions had already been taxed at India's full marginal rate. The RNOR window had been open. He hadn't known what to do with it. This checklist is for the version of Vikram who's still in the US.