The Healthcare Horizon: Real Costs for Early Retirees (Ages 40–65)

You stress-tested recessions, sequence of returns, and market crashes. But the spreadsheet goes blank on healthcare. Here are the real numbers.

The spreadsheet told you everything was fine. You ran the 4% rule. You stress-tested recessions. You modeled sequence-of-returns risk. You calculated down to the dollar when you could stop working. $3.9M portfolio. $136.5K safe withdrawal. You spend $160K. It's tight. You're short by $23.5K annually. But you already knew that. You'd work three more years, you'd cut $15K in annual spending, or you'd find $200K in part-time board work. The math worked.

Then at 2am, you opened a new spreadsheet tab. Healthcare. And your spreadsheet went blank.

The Black Box Years

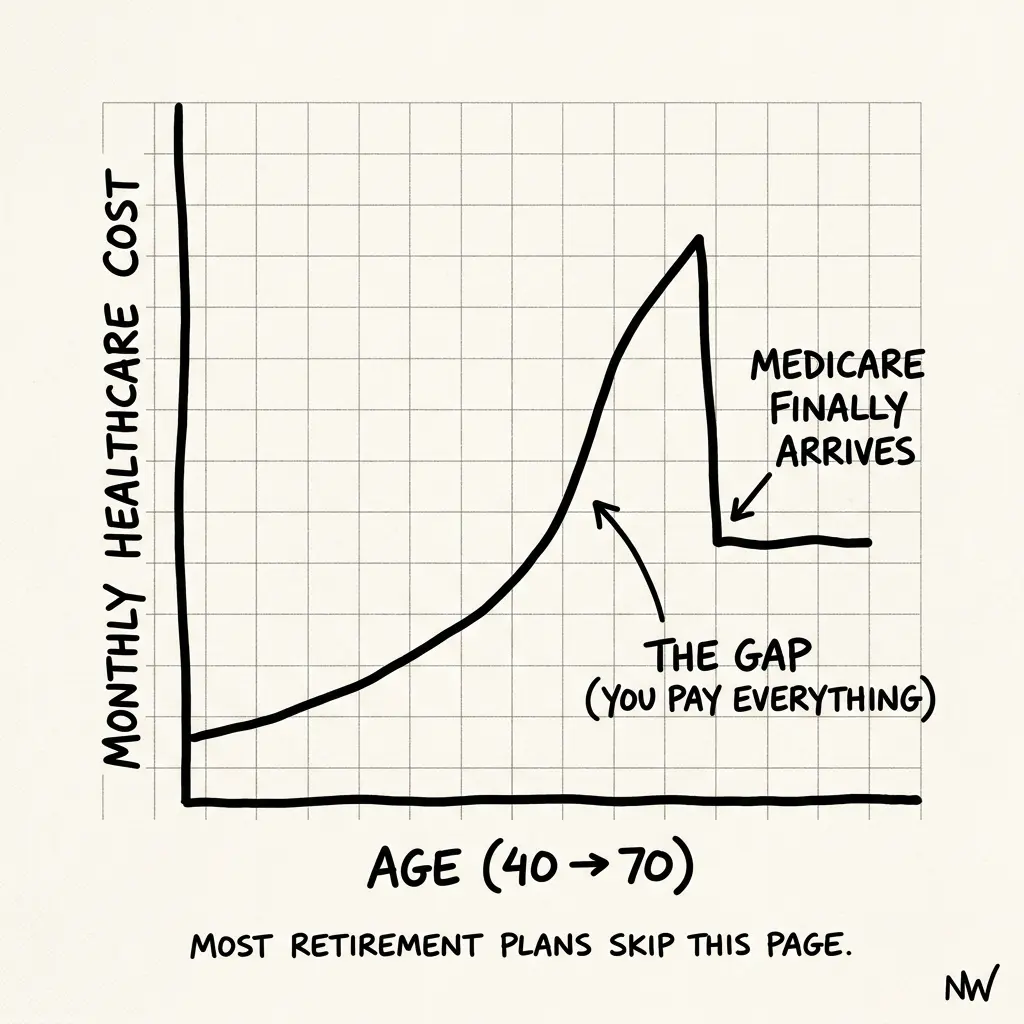

Here's what you know. Medicare starts at 65. Boom. Solved. Ages 40–65 is the gap. The quiet years where everyone else has coverage through employers. You do not have an employer.

Here's what you don't know. What does healthcare actually cost for a healthy 45-year-old. ($400/month? $2,000/month?) What if you have kids on your plan. (Exponential cost.) What if you get a chronic diagnosis at 50. (Uninsurable elsewhere, trapped in current plan.) What if you move to a different state. (Plans are state-level.) What about dental, vision, mental health. (Most plans don't cover dental. Vision is a joke.)

This is the Healthcare Horizon. The point where your FIRE planning hits a wall because the data gets foggy. And the internet doesn't help. Reddit has people saying "$2,000/month family plan, we're fine." Other Reddit people say "$6,000/month, and that's with a high deductible." That's a 300% range. For the same thing.

So you did what HENRY retirees do. You panicked quietly and kept it to yourself.

The Real Numbers (What We Actually Know)

Let me start with what I can confirm. The average ACA individual plan costs (before subsidies): Age 45, tobacco-free, mid-tier plan (Silver): $485/month ($5,820/year). Age 55: $897/month ($10,764/year). Age 64: $1,437/month ($17,244/year).

But here's the thing. These are before the Advance Premium Tax Credit (APTC). If you retire and drop your income to $0, your ACA subsidies are massive. A family of three, age 45, living in a moderate-cost state, filing $30K household income. Your actual premium could be $0. The government covers it all. But you can't live on $0 income forever.

Your true income (for ACA purposes) is your strategic withdrawals. Let's say you're smart about it. Roth ladder, timed conversions, taxable brokerage strategy. Your ACA-reportable income is $50,000.

At $50K family income in a moderate-cost state, a mid-tier family plan runs about $400-600/month after subsidies. That's $4,800–7,200 per year. Add out-of-pocket maximums ($7,000–10,000 per person per year), and your realistic annual healthcare cost is. $12,000–17,000 per year for a healthy family.

The Real Question: Is Your $3.9M Actually Safe?

Let's stress-test your retirement. Portfolio: $3.9M. Annual spend (without healthcare): $160K. Safe withdrawal (4% rule): $136.5K. Shortfall: $23.5K. Now add healthcare. Conservative estimate: $15,000/year. New total spend: $175K. New shortfall: $38.5K per year.

Now the 4% rule is tighter. You need to either work 4 more years, cut spending to $136.5K, or find $38.5K in part-time income. But here's what saves you. Roth conversions during the low-income years.

If you do "ladder" conversions during ages 45–59 (before RMDs), you can create a tax-advantaged glide path. Years 1–5, you convert $100K of traditional IRA to Roth. You pay tax ($25K), but that's it. Your future withdrawals from the Roth are tax-free and don't count as income for ACA purposes. By age 59.5, you have $500K in Roth that you can withdraw tax-free, no ACA impact. That $500K covers healthcare for the next 30+ years at $15K/year. Solved.

This is the math most people don't do. They see the $3.9M, do basic 4% rule math, and miss the sequencing win they have access to.

What Actual Wealthy People Do

I asked a few HNW early retirees (ages 45–60, $3M+) what they actually spend on healthcare. Ages 45–50: $4,000–8,000/year (healthy, low utilization). Ages 50–55: $8,000–15,000/year (first chronic diagnosis, testing increases). Ages 55–60: $12,000–20,000/year (medication management, specialist visits). Ages 60–65: $15,000–25,000/year (healthcare becomes a budget line item).

They all planned for $12K/year. Most were surprised to actually spend $15K+ once they had a diagnosis. They all did Roth conversions. Not because they read an article, but because their tax advisors said "hey, your income is low, this is the time." None of them panicked about healthcare. Why. Because they'd modeled it.

Your Next Move

Step 1: Get quotes. Go to healthcare.gov. Enter your zip code. For household income, use your expected withdrawal amount (not zero). Look at Silver plans. Write down the actual premium.

Step 2: Model your Roth ladder. Talk to a CPA (not an RIA, they'll oversell complexity). Ask: "If I retire at 45 with $3.9M, what's my tax-efficient withdrawal sequence?" They'll show you Roth conversions as the answer.

Step 3: Stress-test with real healthcare costs. Add $15,000/year to your budget. Re-run your 4% rule math. Does it still work?

Step 4: Plan for creep. Every 5 years, assume healthcare costs rise 6% (faster than inflation). Budget for one major diagnosis or event ($5K out-of-pocket max). Plan for dental ($2K/year if you ignore it long enough).

The Reframe

Healthcare isn't a black box. It's just another expense you have to model. The difference. You have time to do it before you retire. Most people don't. They hit their FIRE number, they get excited, they quit. Then at year 2, they get a surprise health diagnosis and their retirement math breaks.

You're doing it backwards. You're stress-testing now. That's the difference between a $3.9M portfolio that's actually safe and one that looks good in a spreadsheet but breaks at year 7 when your kid needs braces and you're diagnosed with Type 2 diabetes and your healthcare cost triples.

Run the numbers. Do the Roth conversions. Plan for creep. Your $3.9M is safe. But only because you're being honest about healthcare.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

What to Do (and Not Do) in the First Six Months After Inheriting Money

The first six months after inheriting money are almost entirely about not making irreversible mistakes. The advisors calling you want you to move fast. That is not in your interest. Here is the practical sequence: hold, inventory, understand, then decide.

The Estate Planning Inflection

Most people think trusts are for death. Vivek Joshi's LLC conversation revealed the real value: structures that protect and govern while you're alive.

Life Insurance as Financial Tool

You can self-insure mortality risk. You cannot self-insure the gap between your wealth and your family's actual needs. Here's what actually matters when you have millions.