HENRY Tax Stack: Sequence Multiple Taxable Events

The worst tax years aren't the high-income years.

The worst tax years are the years when multiple things happen at once: W-2 income at $400K, RSU vesting at $80K, a real estate capital gain at $200K, a bonus at $50K, and an ISO exercise you'd been putting off.

Each income source has its own guide. Its own set of rules. What those guides don't cover: how they interact. How the RSU ordinary income pushes your LTCG rate from 15% to 20%. How the bonus triggers NIIT on investment income you already have. How the ISO exercise, which seemed like a good idea in isolation, creates AMT that isn't recoverable for three years.

These aren't four tax events. They're one tax system. And the order you sequence decisions changes the total bill by five figures.

Quick Answer

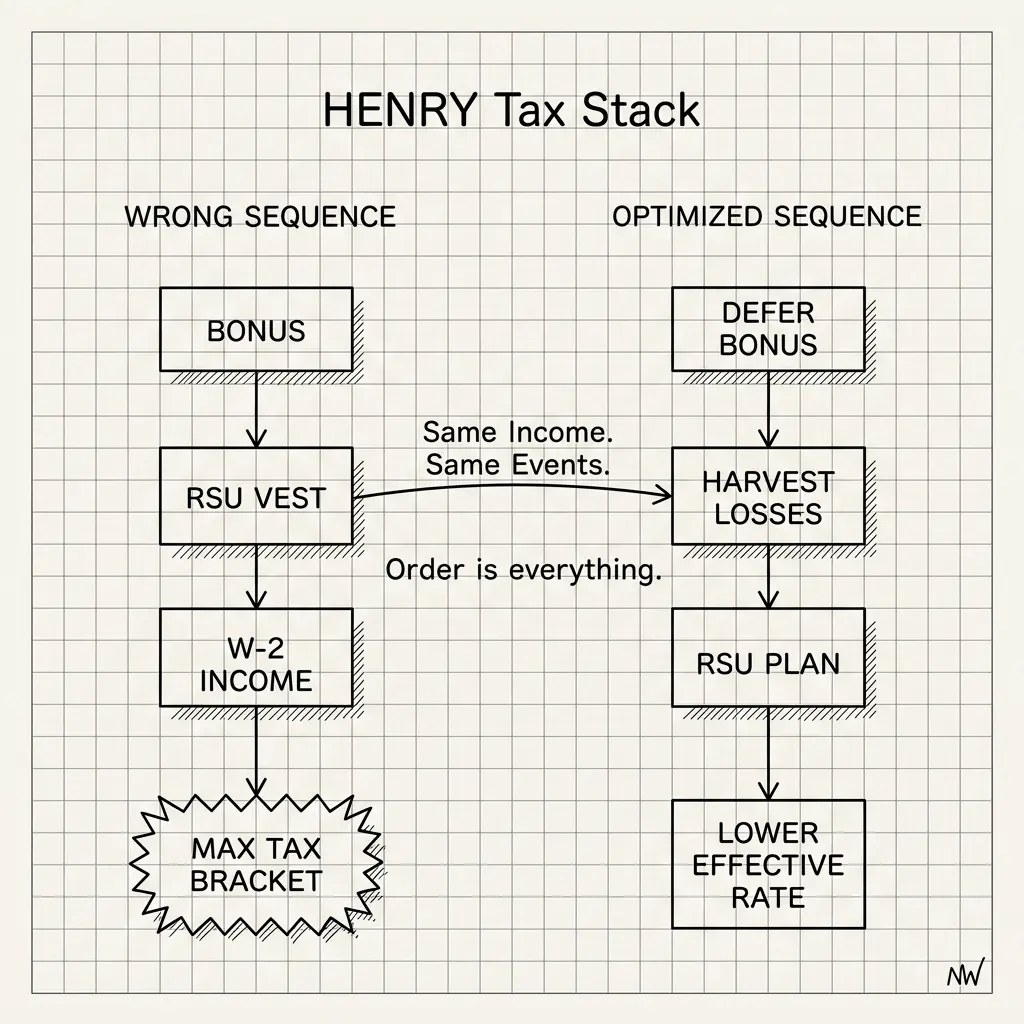

The Tax Sequencing Matrix establishes the decision priority for a year with multiple taxable events: (1) Understand your ordinary income total first — W-2 plus all ordinary income events — because this sets your marginal rate for everything else. (2) Model LTCG rate breakpoints before executing any capital gain transactions. (3) Identify NIIT exposure and whether you can shift investment income to avoid crossing thresholds. (4) AMT model before any ISO exercises. (5) Harvest losses to offset known gains before December 15. (6) Optimize charitable giving timing (DAF, bunching) to maximize deductions against your highest-income year. The order matters because earlier decisions constrain later ones.

The 2026 Tax Landscape (What Changed)

Before building the sequencing matrix, know what you're working with in 2026.

What's Settled

→ Top ordinary income rate: 37% permanently extended (TCJA made permanent by recent legislation)

→ SALT deduction cap: $40,000 MFJ, $20,000 single (increased from prior $10,000 limit — significant for CA/NY residents)

→ NIIT: 3.8% above $200K/$250K — still unindexed for inflation

→ AMT exemptions: $89,075 single / $138,450 MFJ (verify current, indexed annually)

The CA Reality

→ Top CA rate: 13.3% income + 1.1% SDI = 14.4% effective

→ CA SALT conformity: California doesn't conform to federal SALT cap — CA residents can still deduct full CA taxes on CA return

→ CA capital gains: taxed as ordinary income, no reduced rate

→ CA QSBS: does not conform — federal exclusion doesn't apply

The SALT change matters more than most people realize

The SALT cap increase from $10,000 to $40,000 (MFJ) is worth up to $9,250 in federal tax savings for high earners in CA and NY who itemize. ($30,000 additional deduction × 37% marginal rate = $11,100, minus any phase-out at very high incomes.) If you've been taking the standard deduction because SALT was capped at $10K, re-run the itemized vs. standard calculation with the new $40K cap.

The Tax Sequencing Matrix

Six steps. Execute in order. Each step constrains the options available in the next.

Step 1: Establish Your Ordinary Income Baseline

Total all ordinary income sources before making any decisions: W-2 wages, RSU vesting events for the year, any bonus or deferred compensation distributions, NSO exercise spreads, business pass-through income. This is your "ordinary income floor" for the year.

Why this first: Your ordinary income floor determines (a) your marginal rate for additional ordinary income events, (b) whether you've crossed the LTCG rate breakpoints, (c) whether you've crossed the NIIT threshold. You can't make informed decisions about Steps 2-6 without knowing this number.

Critical number to calculate: Taxable income after standard or itemized deductions. If you're close to LTCG rate breakpoints (~$519K single / ~$583K MFJ for the 15%/20% transition), knowing your deduction total matters enormously.

Step 2: Model LTCG Rate Breakpoints

Long-term capital gains rates in 2026: 0% (below ~$94K single/~$188K MFJ), 15% (below ~$519K single/~$583K MFJ), 20% above that. Plus 3.8% NIIT above $200K/$250K — meaning the effective LTCG rate for most HENRYs is 15% or 23.8%, depending on where their total income falls.

The rate cliff question: Are any of your planned capital gain transactions (real estate sale, QSBS partial sale, security sale) creating gains that push you from 15% to 20% LTCG rate? If so, can the transaction be split across two tax years, or can other deductions prevent the cliff?

The compression zone: If your ordinary income plus projected LTCG pushes you to the 20% LTCG zone, but you could reduce ordinary income (by increasing 401(k) contributions, timing deferred comp, or shifting income to next year), you may be able to bring gains back to the 15% zone. The math: $100,000 of LTCG at 15% vs. 20% is $5,000. If you can reduce ordinary income by $100,000 to stay in the 15% zone, that's the value.

Step 3: NIIT Exposure Assessment

NIIT of 3.8% applies to net investment income (dividends, capital gains, interest, passive business income) for taxpayers above $200,000 (single) / $250,000 (MFJ). These thresholds aren't indexed — the same numbers as 2013. Bracket creep is real: more HENRYs hit NIIT each year.

What NIIT applies to: Realized capital gains, dividends, taxable interest, passive rental income. What it doesn't apply to: active W-2 wages, active business income, RSU ordinary income (that's W-2), qualified retirement distributions.

The NIIT compression strategy: If you're just above the NIIT threshold, additional pre-tax retirement contributions can reduce MAGI and potentially reduce your NIIT exposure. The math works best for people who are close to the threshold — it doesn't help once you're significantly above it.

Step 4: AMT Pre-Modeling (Before Any ISO Exercises)

AMT is a parallel tax system. You calculate regular income tax, then calculate AMT, and pay whichever is higher. For most HENRYs, regular tax exceeds AMT — unless they exercise ISOs.

The ISO bargain element: When you exercise ISOs, the spread between FMV and strike price is an AMT preference item. It doesn't create regular income — but it creates AMTI that can push you into AMT.

The AMT exemption phase-out: The AMT exemption phases out at $1 for every $4 of AMTI above $632,650 (single) / $1,265,300 (MFJ) in 2026 (verify current figures). High earners can lose the exemption entirely, making AMT even more expensive.

Before exercising any ISOs: Run the AMT model with your current-year income and the proposed exercise. The marginal AMT rate on ISO bargain elements is 28% above the exemption. At high income levels, the effective rate can exceed regular income tax. Know the number before you sign.

Step 5: Tax-Loss Harvesting (Execute by December 15)

By December 1, you know your full-year realized gains from Steps 1-4. Now identify unrealized losses in your taxable accounts that you can harvest to offset those gains.

Capital losses offset capital gains dollar-for-dollar, regardless of holding period. Net losses above gains offset up to $3,000 of ordinary income annually; excess carries forward indefinitely.

The practical deadline: Trades need to settle in the current tax year. Standard equities settle T+1. Target December 15 for execution to guarantee settlement before December 31. After December 15, settlement risk rises.

Step 6: Charitable Giving Timing

If you give charitably, a high-income year is the best year to do it. The charitable deduction is worth 37 cents per dollar in a 37% marginal rate year vs. 24 cents per dollar in a 24% year.

Donor-Advised Funds (DAFs): Contribute appreciated securities (or cash) to a DAF, get the deduction now, and distribute to charities over multiple years. The contribution timing is what matters for your deduction — not when the charity actually receives the money. December 15 is the practical DAF contribution deadline for current-year tax purposes.

Bunching: If you're near the standard deduction threshold ($31,400 MFJ in 2026), consider alternating between "bunched" charitable years (itemize) and standard deduction years. A two-year bunching strategy in a high-income year can capture $15,000-$25,000 more in deductions than spreading contributions evenly.

The SALT + NIIT + AMT Trifecta

High earners in California and New York face a specific tax complexity that most advice ignores: three parallel systems that interact badly.

// CA High Earner Tax Surface (2026, MFJ, $600K total income)

Federal ordinary income (37% bracket): 37%

CA state income: 13.3%

NIIT on investment income: 3.8%

Combined effective rate on next dollar of investment income: ~54%+

// Note: SALT deduction reduces federal burden somewhat

// AMT adds parallel complexity — cannot combine directly

At these rates, the value of timing decisions — deferring income to a lower year, accelerating deductions into a high year, harvesting losses against high-tax-year gains — is significant. A $100,000 income timing decision at 54% effective rate is worth $54,000 over a $100,000 decision at 37%. The math rewards precision.

This is precisely the kind of calculation that requires knowing your actual numbers — not generic tax guidance.

A Worked Example: The Collision Year

Marcus, 42. Head of Product at a public tech company. California. Married, two kids.

INCOME EVENTS (2026)

W-2 salary: $380,000

Annual bonus (paid March): $70,000

RSU vest (4 events): $120,000

Sold rental property (LTCG): $180,000

Total: $750,000

AVAILABLE TOOLS

→ $60,000 in unrealized losses (taxable accounts)

→ DAF with $0 balance (can fund now)

→ Itemized deductions ~$85,000 (with new $40K SALT)

→ Mega backdoor Roth capacity: $38,000

→ 401(k): not yet maxed for year

Baseline ordinary income: $380K + $70K + $120K = $570K ordinary income before deductions. After $24,500 401(k), $8,550 HSA, and $85K itemized deductions: taxable ordinary income ~$452,000. Well above 37% bracket.

LTCG rate check: $452K ordinary + $180K LTCG = $632K total. The $180K LTCG is in the 20% bracket (above $583K MFJ threshold). Effective LTCG rate: 20% federal + 13.3% CA (CA taxes LTCG as ordinary) + 3.8% NIIT = 37.1% combined. This is the rate on the rental property gain.

TLH intervention: Harvest $60K in losses from taxable accounts. This offsets $60K of the rental property LTCG. Savings: $60K × 37.1% = $22,260. Execute by December 15.

DAF charitable contribution: Marcus gives $40,000 annually to charity. Instead of spreading $40K over 2026-2027, contribute $80K to a DAF now in 2026. Additional $40K deduction at 37% marginal rate = $14,800 additional tax savings vs. distributing evenly across two years.

Mega backdoor Roth: With $38K in after-tax 401(k) conversion capacity, Marcus converts to Roth in Q4 of his highest income year. Future growth on $38K accumulates tax-free. Worth doing precisely because this is a high-income year — the tax cost of the conversion is zero (after-tax basis) while the future benefit compounds.

Coordinated result: approximately $37,000 in tax savings vs. independent decisions on each income source. Same income. Different sequencing.

FAQ

At what income level does this kind of tax coordination actually matter?

The interaction effects become significant above $300,000 in total income — that's roughly where NIIT, LTCG rate transitions, and AMT all become live concerns simultaneously. Below $200,000, most of the complexity simplifies out. Above $300,000, the marginal value of sequencing decisions correctly scales with income.

When should I start this process each year?

September 1 is the right starting point. By September, you can project full-year income with reasonable confidence. October is for LTCG modeling and large transaction decisions. November is for AMT modeling and ISO exercises. December 1-15 is the execution window for TLH and DAF contributions. Starting in December means you can only execute Steps 5-6. Starting in September means you can execute all six steps in the right order.

Can I defer RSU income to a lower-income year?

Generally no. RSU ordinary income is fixed at vest date — the company controls the vest schedule. What you can influence: (1) the tax elections around RSUs (disposition choice), (2) offsetting RSU ordinary income with other deductions (DAF contributions, increased 401(k)), and (3) timing other income events around known RSU vest months. If you have a year with unusually heavy RSU vesting, that's the year to maximize deductions and DAF contributions.

What about deferred compensation — should it be included in the ordinary income baseline?

Yes, if you have a distribution from a non-qualified deferred compensation plan (NQDC) planned for the year. NQDC distributions are ordinary income at distribution. The distribution schedule is typically locked years in advance (IRS Section 409A restrictions). If you can elect the distribution schedule and haven't yet, the decision should account for projected future income levels — defer into lower-income years if possible.

The decision that requires knowing YOUR numbers

The Tax Sequencing Matrix gives you the framework. The specific numbers — your LTCG breakpoint, your exact NIIT exposure, your AMT room — require your actual income, your actual deductions, and your actual portfolio. Generic advice gives you the structure. Inside-out intelligence gives you the answer.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

You Inherited a Brokerage Account. Here's What 'Basis Step-Up' Actually Means.

When you inherit a brokerage account, the cost basis resets to the date-of-death value — meaning decades of capital gains can simply disappear as a tax liability. Most inheritors don't find out until after they've already sold.

The Transition Year Tax Map: Planning for the Income Gap

The first 12 months post-exit are a tax minefield. Sequence your income, deductions, and Roth conversions to avoid the 'Success Tax' that burns 10-20% of your final payouts.

Liquidity Event Sequencing: Pre-Exit Tax Planning for Founders

Real exit tax savings (15-25% of proceeds) come from decisions 12-18 months before close. Master charitable structures, entity optimization, QSBS timing, and option planning.