You Didn't Earn This Money. That Doesn't Mean You'll Lose It.

The money has been sitting in a Schwab money market account for fourteen months. Every week you tell yourself you'll deal with it this weekend. You are not lazy. You are not bad with money. Something else is happening.

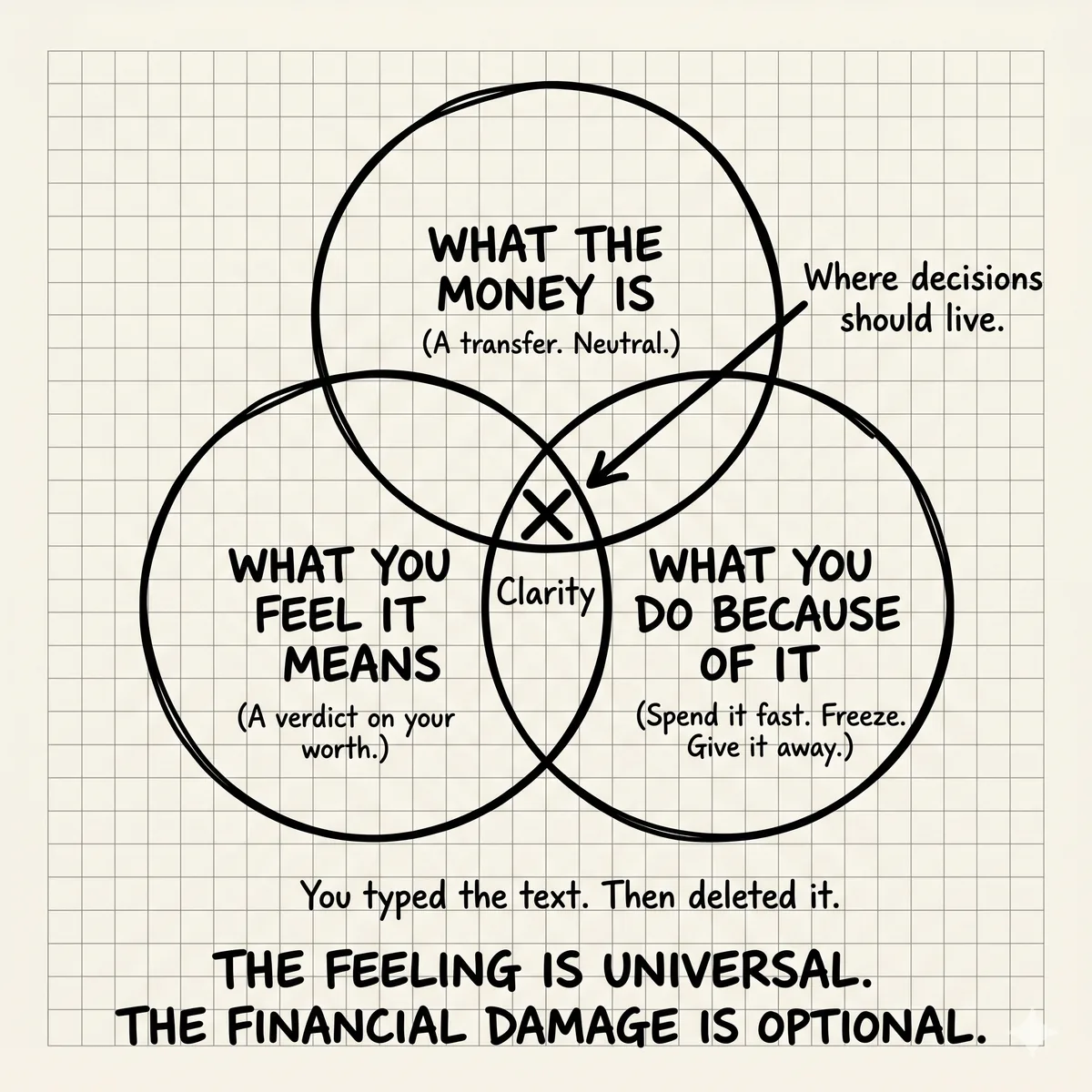

There is a thing that happens to people who inherit money that almost nobody writes about. It is not the tax questions. It is not the investment decisions. It is the feeling, persistent and specific, that you are not the kind of person who has this much money.

You didn't earn it. Your father built it over 40 years running a business, saving carefully, living modestly. You watched him clip coupons. You watched him drive the same truck for 12 years. And now his life's work is sitting in an account with your name on it and you are terrified to touch it.

That feeling has a name. Researchers call it "sudden wealth syndrome." People who experience it call it feeling like a fraud. You might call it the sense that you are holding something that belongs to someone else and if you make a single wrong move, you will prove you were never capable of this.

This is extremely common. And it is creating a specific problem for you that has nothing to do with markets or advisors.

What Imposter Feeling Actually Does to Financial Decisions

The imposter feeling doesn't make you reckless. It makes you frozen.

The paradox of sudden wealth is that the very feelings meant to protect the money end up costing it. Not through bad investments. Through doing nothing.

Here is what "doing nothing" actually looks like in financial terms. $3M in a money market fund earning 4.8% generates $144,000 per year. That sounds fine. But 4.8% in a taxable account, after taxes at ordinary income rates (let's say 35% combined federal and state), nets roughly 3.1%. Inflation over the same period is around 3%. Your real return is approximately zero.

You are not losing money in the way it would show on a statement. You are losing purchasing power. The money your father built is, in real terms, standing still while time passes. The imposter feeling, which was supposed to protect his legacy, is slowly eroding it.

This is not a critique. It is a description of what happens. And it happens to most inheritors for at least 12 months. Researchers who study inherited wealth find that the modal behavior is precisely this: leave it in cash or near-cash for 12 to 24 months while "figuring it out." In many cases, people never fully emerge from that holding pattern.

Where the Feeling Comes From

The feeling is not arbitrary. It has a specific psychological structure.

Money, for most of us, is tied to identity through labor. You earn what you are worth. You accumulate what you have worked for. This equation is deeply ingrained. It is how your self-concept of financial competence was built.

An inheritance breaks the equation. You have not earned this. Your identity as a competent earner doesn't apply. The implicit question becomes: if you didn't earn this, why should you be trusted to manage it?

The imposter feeling is the mind's answer to that question. It reads as humility but functions as paralysis. It is the brain saying: you are not qualified for this, therefore do not act, therefore do not risk proving that you are not qualified.

There is also a grief layer. The money arrived because your father died. Moving it, investing it, changing it in any way can feel like moving on from him. The frozen account is, in some part, an expression of the unwillingness to close a chapter. The account as a memorial.

Both of these are recognizable and human responses. They are not signs that something is wrong with you. They are signs that something very hard happened to you and your mind is managing it the way minds manage hard things.

What the Imposter Feeling Predicts (and What It Doesn't)

Here is the thing that most financial content gets wrong about this: the imposter feeling does not predict what will happen to the money.

Research on inherited wealth consistently shows that adults who inherit significant assets are not more likely to "blow it" than people who accumulated the same wealth themselves. The horror stories (lottery winners who go bankrupt in five years) are real but not representative. They are also usually about people with no prior financial education and no trusted advisors, not about people with careers, financial accounts, and college educations.

You have been managing a 401(k). You have a mortgage. You have filed taxes. You understand compound interest. The feeling that you are not equipped for this is not an accurate prediction of your competence. It is an artifact of how the money arrived.

The people who lose inherited wealth don't usually lose it because they felt too confident. They lose it because they trusted the wrong advisor too quickly, or made large concentrated bets, or changed their entire life too fast. The cautious, paralyzed inheritor is not the primary risk profile for money loss. The caution is a protection. It is just also, eventually, a cost.

The Specific Behaviors to Watch For

The imposter feeling, left unexamined, tends to produce a few predictable financial behaviors:

- Indefinite deferral. "I'll decide when I'm ready" extends to 24 months of money market earning nothing in real terms. The threshold for "ready" keeps moving.

- Excessive delegation. Handing control to an advisor not because you have verified their quality but because you don't feel entitled to have opinions. This creates relationships where your interests may not come first.

- Secrecy that costs money. Not telling your accountant about the inheritance, or telling them late, because you feel awkward about it. Missing tax planning opportunities as a result.

- Lifestyle suppression past the point of meaning. Refusing to make any quality-of-life improvements because spending feels like betraying the legacy. Your father saved so you could have security. Spending $10,000 on a trip you've wanted to take for 10 years is not betraying what he built.

- Avoiding the topic with your spouse. "It's Dad's money" as a way of not fully integrating it into your joint financial picture, which creates planning gaps.

None of these are unusual. Most people who inherit significant money exhibit at least one of them. Recognizing the pattern is the first step to making different choices.

A Different Way to Frame This

The frame that seems to help most: stewardship rather than ownership.

You are not the person who built this wealth. You are correct about that. But you are now the person responsible for it. Those are different roles. The question is not "am I worthy of this money?" The question is "what does a responsible steward of this money do?"

A responsible steward learns the basics. Reads the Bogleheads guide, or finds a fee-only CFP for a one-time consultation, or spends 30 hours understanding what they have before making decisions. A responsible steward acts on a reasonable timeline rather than deferring forever. A responsible steward honors the intent of what was built by taking care of it, not by leaving it untouched in a money market account.

Your father worked so that you would have security. The money sitting in a fund earning nothing real is not what he worked for. Acting thoughtfully, on a reasonable timeline, with the right people helping you, is honoring what he built.

You didn't earn this money. That is true. It also doesn't mean you'll lose it. The evidence is on your side. The feeling is not the forecast.

On Getting Help

The imposter feeling is sometimes better addressed therapeutically than financially. A few sessions with a therapist who works with life transitions, or with a financial therapist (yes, this is a real specialty), can do more for your financial decisions than a dozen meetings with an investment advisor.

This is not instead of financial planning. It is sometimes a precondition for it. If you cannot make decisions because the emotional layer is blocking you, clearing the emotional layer first is the highest-leverage move.

The Sudden Wealth Institute (sudden-wealth.com) and the Financial Therapy Association (financialtherapy.org) have directories of professionals who specialize in exactly this situation.

The money doesn't need to be decided this week. But the paralysis does need to be named.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

180-Day Window: Critical Steps After Liquidity Event

After exit or IPO, 6 months determine everything: over-concentration, tax errors, lifestyle lock-in, estate planning failures. Sequence the right decisions before permanent lock-in.

AI Knows the Market. It Doesn't Know You.

Every Davos panel is a purchased narrative. AI amplifies those narratives. But the S&P hitting new highs tells you nothing about whether you should sell your RSUs or refi your mortgage.

You Can't Share This With Anyone Who Won't Make It Weird

You typed the text. Then deleted it. The people who most need peer context are the ones most isolated from it — family has baggage, friends have context mismatch, advisors have incentive misalignment. This is the problem NettWorth was built to solve.