Will I Owe Taxes on My Inheritance? (What Most Articles Get Wrong)

The check from the estate cleared last week. Your first thought was: "Do I owe taxes on this?" Your second thought was: "I have no idea what the answer is, and everyone I've asked gives me a different answer."

This is one of the most common sources of confusion around inheritance. Not because the tax code is exceptionally cruel here. Because most articles conflate three different things that sound similar but are legally distinct.

Let's separate them clearly.

The Three Things Most People Are Confusing

There are three different tax concepts that get jumbled together when people talk about "inheritance taxes":

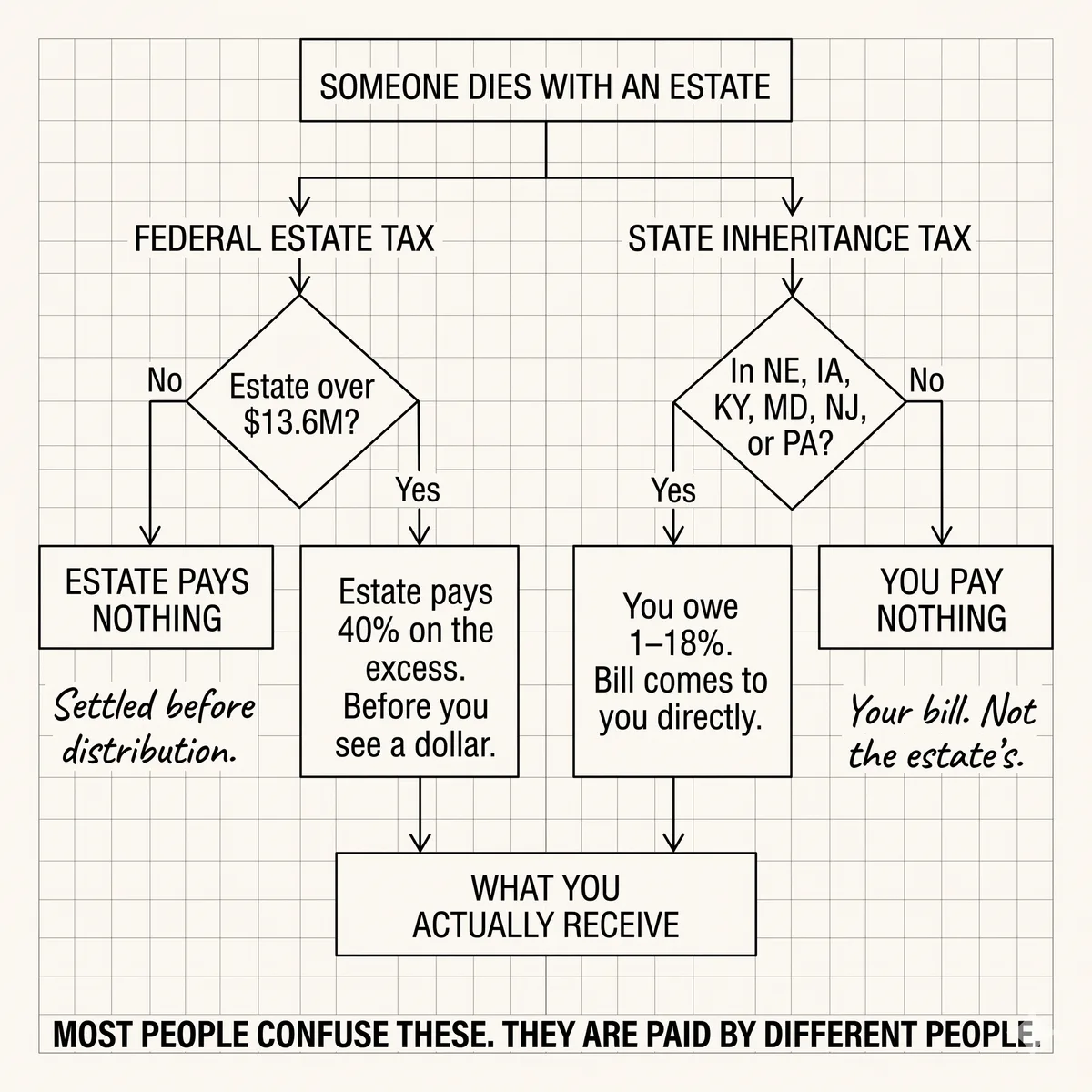

- Federal estate tax. A tax on the total value of a deceased person's estate before it is distributed to anyone. Paid by the estate, not by you.

- State inheritance tax. A tax on what you, the beneficiary, receive. Paid by you. But only in 6 states.

- Income tax on what you do after you inherit. This is what most people actually end up paying and is the one least discussed. You don't pay income tax on the inheritance itself in most cases. You do pay income tax on dividends, interest, and IRA distributions that come out of the inherited assets going forward.

Most people worrying about "inheritance taxes" are worried about concept 1 or 2. Most people actually paying taxes are dealing with concept 3. Let's go through each.

Federal Estate Tax: Who Actually Owes It

The federal estate tax applies to estates worth more than the federal exemption amount. In 2026, that exemption is $13.61 million per individual, or $27.22 million for a married couple using portability.

If your father's estate was worth less than $13.61 million (the total of everything he owned: house, brokerage accounts, retirement accounts, life insurance paid to the estate, business interests, and everything else), his estate owes zero federal estate tax.

The vast majority of estates pay no federal estate tax. The IRS reports that fewer than 0.1% of estates owe any federal estate tax. If the estate attorney or CPA didn't mention estate tax, it probably doesn't apply.

Important caveat: the $13.61 million exemption is scheduled to drop significantly starting in 2026, when the Tax Cuts and Jobs Act provisions sunset. The exemption may revert to approximately $7 million (indexed for inflation from 2017). If you are managing a large estate or doing planning for someone who is still alive, this change matters. For most people who have already inherited, it doesn't change what you owe retroactively.

Estate tax, when it does apply, is paid by the estate before assets are distributed to beneficiaries. You don't receive an inheritance and then write a check for estate tax. The estate settles it first.

State Inheritance Tax: The One That Can Apply to You Directly

Six states impose an inheritance tax paid by the beneficiary: Iowa, Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania. (Maryland has both an estate tax and an inheritance tax, which is a fun combination.)

If neither you nor the deceased lived in one of those states, you owe no state inheritance tax.

If you do live in one of those states, or the deceased did, rates and exemptions vary. Most states exempt direct descendants (children, grandchildren) from inheritance tax entirely or at very low rates. Pennsylvania charges 4.5% on inheritances from parents to children. Nebraska charges 1% on close relatives. The specifics matter.

Check your state. If you're in one of the six, confirm with a CPA whether you owe anything. This is the one tax that comes directly to you (as the inheritor) rather than to the estate.

Federal Capital Gains Tax: The Step-Up Connection

When you inherit a taxable brokerage account or real property, you generally do not owe income or capital gains tax on the value at the time of inheritance. This is not a loophole. It is by design.

The theory: the estate tax was supposed to capture the unrealized gains at death. Since most estates don't owe estate tax (see above), the practical result is that decades of accumulated gains often pass to inheritors tax-free via the basis step-up. This is one of the largest tax advantages in the code for families.

The step-up basis means your cost basis in the inherited stock, fund, or property resets to its value on the date of death. If your father bought shares at $10 and they're worth $80 when he died, your cost basis is $80. You don't owe capital gains tax on the $70 gain he accumulated. If you sell immediately for $80, you owe nothing. If you hold and sell for $90 later, you owe capital gains tax only on the $10 gain from $80 to $90.

We cover this in more detail in the step-up basis post. The core point for the tax question: you don't owe taxes on inherited brokerage assets at the time of inheritance, and you get a reset on future gains.

What You Will Owe Taxes On Going Forward

Once you inherit the money and it's in your accounts, any income it generates becomes your taxable income. This is where most inheritors are genuinely surprised in the first tax year.

- Interest income from money market funds and bonds. If your $3M is sitting in a money market fund earning 4.8%, that's $144,000 in interest income. It is taxable as ordinary income in the year you receive it. At a 35% combined federal and state rate, that's $50,400 in taxes on money you didn't actually "spend." This surprises people.

- Dividends from stock holdings. Qualified dividends (from most U.S. stocks and many international stocks) are taxed at long-term capital gains rates (0%, 15%, or 20% depending on income). Non-qualified dividends are taxed as ordinary income.

- Capital gains when you sell. If you sell inherited investments after the date of death, you owe capital gains tax on any gains from the step-up value forward. Long-term capital gains rates (0%, 15%, or 20%) apply if you hold for more than a year from the date of death.

- Inherited IRA distributions. Every dollar you take out of an inherited traditional IRA is ordinary income. This is the most significant income tax issue for many inheritors and the one most worth planning carefully.

- Rental income from inherited real property. If you inherited a condo and rent it out, the rental income is taxable.

The Estimated Tax Payment Issue

If the inheritance creates significant new income (interest, dividends, a large inherited IRA distribution), you may owe estimated quarterly tax payments. The U.S. tax system is pay-as-you-go. If you don't withhold enough throughout the year, you owe a penalty.

The threshold: if you expect to owe more than $1,000 in federal income taxes that won't be covered by withholding, you should make estimated payments. Quarterly deadlines are generally April 15, June 15, September 15, and January 15 of the following year.

Ask your CPA in the first year: "Given the inherited income I'm now receiving, do I need to adjust my withholding or make estimated tax payments?" This is an easy oversight to avoid with one conversation.

The Simple Summary

- Federal estate tax: You don't owe it. The estate did (if large enough, usually it's not).

- State inheritance tax: Only in 6 states, usually small amounts, often exempt for children.

- Capital gains on inherited brokerage: No tax at time of inheritance (basis stepped up). Tax only on future gains from that new basis.

- Income from inherited assets: Yes, you owe tax on interest, dividends, and IRA distributions going forward.

- Inherited IRA: Every distribution is ordinary income. Plan the withdrawals carefully over 10 years.

The tax picture for most inheritors is manageable. The most important thing is to talk to your CPA in the year you inherit, before the end of that calendar year, so you can plan the income and avoid surprises on April 15.

Most people who inherit money don't owe a large lump sum "inheritance tax." What they owe is income tax on the income the inherited assets generate. That's real. It requires planning. It is not the same as the scary "inheritance tax" that most articles describe incorrectly.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

Inherited IRA: The 10-Year Rule That Most People Get Wrong

Since the SECURE Act, most non-spouse inheritors must empty an inherited IRA within 10 years. The mistake is waiting until year 10 and taking a massive tax hit all at once. Spreading thoughtful annual withdrawals across the decade can save tens of thousands of dollars.

NRI Selling Property in India: The Two-Tax Hit Nobody Explains Clearly

India taxes the property. Your country of residence taxes you. The DTAA doesn't eliminate the second hit — it sequences them and gives you a credit. On a large Indian property sale, the combined effective rate is closer to 24% than the 12.5% India rate most people quote.

The RNOR Window: The 2-3 Year Tax Opportunity Most NRIs Miss

Your first 2-3 years back in India, foreign income is largely tax-free. It's the window for Roth conversions and asset restructuring. Almost nobody plans for it before they leave the US.