You Inherited a Brokerage Account. Here's What 'Basis Step-Up' Actually Means.

Your father bought Apple at $4 in 2003. It's worth $190 now. He never sold it. You just inherited 2,000 shares. Everyone is telling you to diversify. Before you sell a single share, you need to understand what just happened to your tax bill.

The answer is: it almost disappeared. And most people don't find out until after they've already sold.

This is the most valuable tax treatment in the entire U.S. tax code for inheritors, and it is the least understood. The basis step-up. It is not complicated once you see it. But it has a timing dimension that matters enormously. If you sell before you understand it, you may pay taxes on gains you didn't have to pay.

What "Basis" Actually Means

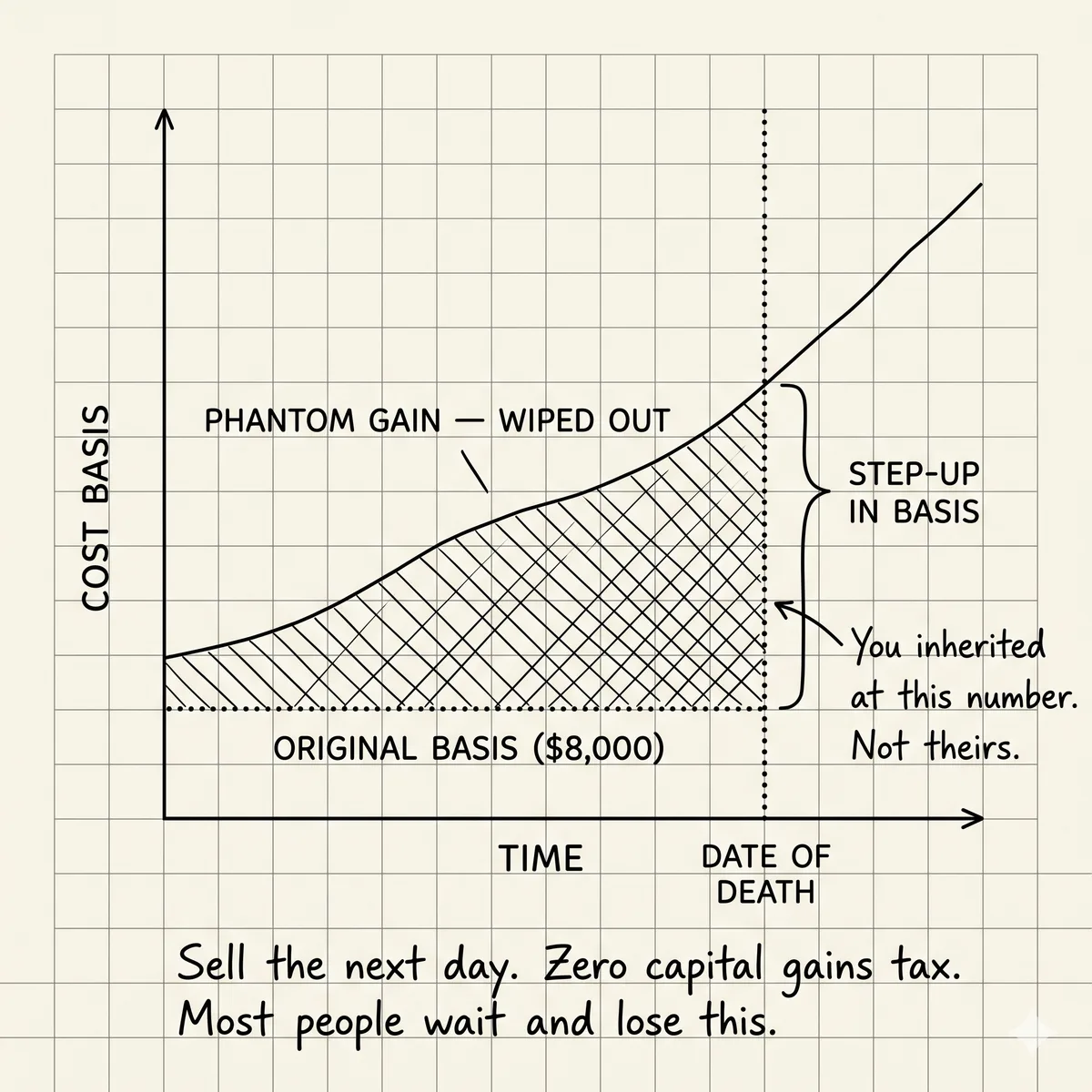

When you sell an investment, you pay capital gains tax on the profit. The profit is calculated as: sale price minus cost basis. The cost basis is what you originally paid for it (plus any reinvested dividends, adjusted for splits, etc.).

If your father bought those 2,000 Apple shares at $4, his cost basis was $8,000. If they're worth $380,000 today, his paper gain is $372,000. If he had sold before dying, he would have owed long-term capital gains tax on $372,000. At a 20% federal rate plus the 3.8% net investment income surtax, that's roughly $88,000 in federal taxes. More if he was in California.

Now he's gone. You inherited the shares.

Under IRC Section 1014, your cost basis in inherited property resets to the fair market value on the date of death. Not what he paid. What it was worth the day he died.

If Apple was at $190 on the day he died, your basis on those 2,000 shares is $380,000. Not $8,000.

If you sell them tomorrow for $380,000, your taxable gain is zero. The $372,000 of gain your father accumulated over 20 years simply ceased to exist as a tax liability.

That's not a loophole. That's the law. And most people miss it.

Why People Miss It

The most common scenario: inheritor gets the account, sees a big number, gets nervous, and asks their new advisor to "just simplify everything." The advisor moves it all into their preferred funds. All at once.

If the advisor knows about basis step-up, this is actually fine. Because the basis was reset to date-of-death value, selling everything shortly after death and reinvesting has minimal tax consequences. The gain from death-date value to sale date (usually small, over a short period) is all that's taxable.

But here is the mistake people make: they do nothing with the account for 18 months, then sell everything. Now the gain from the step-up value to the sale price is real. If the market went up 20% in that 18 months, they owe taxes on a 20% gain instead of zero.

The step-up didn't go away. But by waiting, they created new gains on top of it. This is fine if they were holding intentionally. It's a mistake if they were holding because they didn't know what to do and then eventually needed to liquidate.

The Practical Sequence

Step 1: Confirm the step-up happened

Call the brokerage. Ask: "What is the cost basis recorded for the inherited shares in this account?" The answer should be the fair market value on the date of death. If the brokerage shows your father's original purchase prices, the basis has not been updated. This needs to be fixed before you sell anything.

For large estates, the estate executor should have determined the date-of-death values (usually from brokerage statements on that specific date). This is the number that goes on the estate tax return (Form 706) if one was required. It is also your basis.

Step 2: Document it now

The brokerage should have a record. But keep your own copy. The probate court documents showing the date of death, the brokerage statements from that date (or as close to it as possible), and any estate tax return if one was filed. Years from now, if the IRS questions your basis, you want clean documentation.

Step 3: Understand what you're actually holding

Many inherited brokerage accounts are complicated. Your father may have had 40 positions across 30 years. Some with huge gains (now stepped up). Some with embedded losses (these disappear too at death, unfortunately). Some that have already been sold.

The question to ask: after the step-up, what are the holdings and what are their current gains or losses relative to step-up basis? This is the starting point for any investment decision.

The Special Case: Community Property States

If you inherited assets from a spouse (not a parent), and you live in a community property state (California, Texas, Arizona, Nevada, Washington, Idaho, Louisiana, New Mexico, Wisconsin), the rules are even more favorable. In community property states, both halves of community property get a basis step-up, not just the deceased spouse's half. This is sometimes called the "double step-up."

This is one of the situations where talking to a CPA who understands estate basis rules is worth the cost of a single consultation.

What Doesn't Get Stepped Up

The step-up applies to assets in a taxable brokerage account, real property, and most other capital assets. It does not apply to:

- Inherited IRAs or 401(k)s. These are pre-tax retirement accounts. The money was never taxed when it went in. When you take it out, you pay ordinary income tax. No step-up. The SECURE Act rules about 10-year distribution windows apply here and are covered separately.

- Annuities. The gain inside an inherited annuity is taxable as ordinary income when distributed.

- Series I Bonds and EE Bonds. Accrued interest is taxable when redeemed.

If your parent had both a brokerage account and an IRA, the brokerage account benefits from basis step-up and the IRA does not. This matters when deciding which to spend first (spend from the IRA earlier to spread out the tax hit, preserve the stepped-up brokerage account longer to minimize capital gains).

Is Selling Right After Inheritance Actually a Good Idea?

Sometimes yes. If the inherited portfolio is concentrated in a few positions your parent accumulated over decades, and you want a more diversified allocation, the period right after death is the lowest-tax moment you will ever have to sell those positions. The step-up basis means gains from decades of appreciation are gone. You only owe tax on appreciation from date-of-death forward.

Selling everything immediately is not obviously wrong. It depends on whether you have a better place to put the money, whether you're doing it in a tax-aware way, and whether you're doing it because it's the right financial move or because an advisor told you to and you hadn't asked the right questions yet.

The key: know your basis before you sell anything. The rest of the decision can take some time. The basis confirmation cannot wait.

One More Thing: Tax-Loss Harvesting No Longer Applies

If your parent had positions with large unrealized losses, those losses disappear at death too. The basis steps up to current value regardless of whether that value is higher or lower than what was paid. If Apple was down when he died, the basis steps down, not up, to the lower value.

Unrealized losses in an inherited portfolio cannot be harvested by the estate or the inheritor unless the position was sold before death. This is occasionally a reason to sell a specific position before death if there is time and planning. Most families don't have that opportunity. It's worth knowing in case you do.

The basis step-up is not complex. But it is specific. And getting the details right in the first few months protects you from tax mistakes that are much harder to fix later.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

The Green Card Exit Tax: Why Your Biggest Immigration Upgrade Has a Hidden Cost

After 8 years, a green card isn't just an immigration status — it's a tax position with a specific cost to exit. The deemed-sale rule applies to your entire portfolio on the day you leave. Most NRIs don't discover this until they want to move back.

Inherited IRA: The 10-Year Rule That Most People Get Wrong

Since the SECURE Act, most non-spouse inheritors must empty an inherited IRA within 10 years. The mistake is waiting until year 10 and taking a massive tax hit all at once. Spreading thoughtful annual withdrawals across the decade can save tens of thousands of dollars.

Roth IRA Is a Tax Trap for NRIs Returning to India

India taxes Roth distributions as ordinary income. The account everyone told you to max is built for a US retirement, not an India return. Most NRIs find this out too late.