How to Actually Invest an Inheritance (Without a Finance Degree)

You've done the inventory. The estate is settled. You've talked to your CPA. You've been reading for six months. Everyone says "invest it" but nobody explains what that actually means when you're holding $3M and have never done this before.

This post is the one that explains it.

No jargon. No upsell. No product recommendation. Just the framework that most financial economists actually agree on, which is much simpler than the industry wants you to believe.

The Thing the Industry Doesn't Want You to Know

The financial industry is built around complexity. The more complex your portfolio, the more it needs management. The more it needs management, the more fees it generates. This creates a structural incentive to make investing feel harder than it is.

Here is what the academic research actually shows. Over any 15-year period, roughly 85 to 90 percent of actively managed mutual funds underperform a simple index fund that tracks the same market. The more expensive the fund, the worse it does on average. Hedge funds, with their "2 and 20" fee structures (2% annual management plus 20% of profits), have consistently underperformed simple index portfolios after fees over the past 15 years.

This is not controversial among finance academics. It is the Bogleheads insight, named after Jack Bogle, the founder of Vanguard, who spent 40 years making the case for index investing. The Bogleheads community on Reddit (r/Bogleheads) applies this research in very practical terms.

The insight: you don't need complexity to succeed. You need low costs, diversification, and time.

The Three-Fund Portfolio

The Bogleheads three-fund portfolio is the simplest implementation of this idea that covers essentially everything:

- U.S. total stock market index fund. This owns a piece of every publicly traded company in the United States. At Vanguard, this is VTSAX (mutual fund) or VTI (ETF). At Fidelity, it's FZROX or FSKAX. At Schwab, it's SWTSX. These funds hold thousands of companies. When the U.S. economy grows over time, this grows.

- International stock market index fund. This owns companies outside the U.S. Developed markets (Europe, Japan, Australia) and emerging markets (India, Brazil, etc.). At Vanguard: VTIAX or VXUS. About 40% of the world's stock market value is outside the U.S.

- Bond market index fund. U.S. government and corporate bonds. These are more stable than stocks, don't grow as much, but reduce volatility. At Vanguard: VBTLX or BND.

That's it. Three funds. Thousands of underlying holdings. Low expense ratios (often under 0.05% per year, which is $50 per $100,000, compared to 1% which is $1,000 per $100,000). Broad diversification.

The allocation between the three depends on your age, goals, and risk tolerance. A simple starting point: your age in bonds. If you're 42, roughly 40% in bonds, 60% in stocks (split between U.S. and international). This is conservative by some standards. Adjust based on how you actually feel about volatility, not how you think you should feel.

Are Target-Date Funds a Cop-Out?

No.

Target-date funds (like Vanguard Target Retirement 2045 Fund) do the three-fund portfolio for you automatically. They hold a diversified mix of index funds and gradually shift toward more bonds as you approach the target date. They rebalance automatically. They are a complete portfolio in a single fund.

Expense ratios are slightly higher than the individual index funds (about 0.10-0.15% versus 0.03-0.05%), but the difference is small. For many people, the simplicity of a target-date fund is worth the marginal cost.

Using a target-date fund is not admitting defeat. It is making a sensible choice that most financial economists would approve of. If an advisor tells you that target-date funds are "too simple" for your situation, ask them to show you the evidence that their approach consistently outperforms. They usually can't.

Tax-Advantaged Accounts Come First

Before you put any inherited money into a taxable brokerage account, make sure you are using all available tax-advantaged space. This is one area where an inheritance gives you useful flexibility.

- 401(k) contribution to the max. The 2026 limit is $23,500 plus $7,500 if you're 50 or older. If you haven't been maxing your 401(k) because of cash flow, the inheritance gives you the income cushion to do it now. The tax savings are meaningful.

- Roth IRA. If your income allows it, contribute $7,000 per year (2026 limit). If you earn too much for direct Roth contributions (over $236,000 for married filing jointly), the backdoor Roth IRA is available. It is not complicated; your CPA can walk you through it.

- HSA if you have a high-deductible health plan. The HSA is the most tax-advantaged account available. Contributions are pre-tax, growth is tax-free, withdrawals for medical expenses are tax-free. Contribute the maximum ($8,300 for families in 2026) every year you can.

- 529 for children's education. If you have kids and college is coming, inherited money can fund a 529 now. Superfunding rules allow up to five years of annual exclusion gifts at once ($18,000 per year per child in 2026, so $90,000 per child at once as a one-time election).

The inherited money sits in the taxable brokerage account. But it allows you to redirect current income you would have spent into tax-advantaged accounts instead. Think of it as a cash flow enabler.

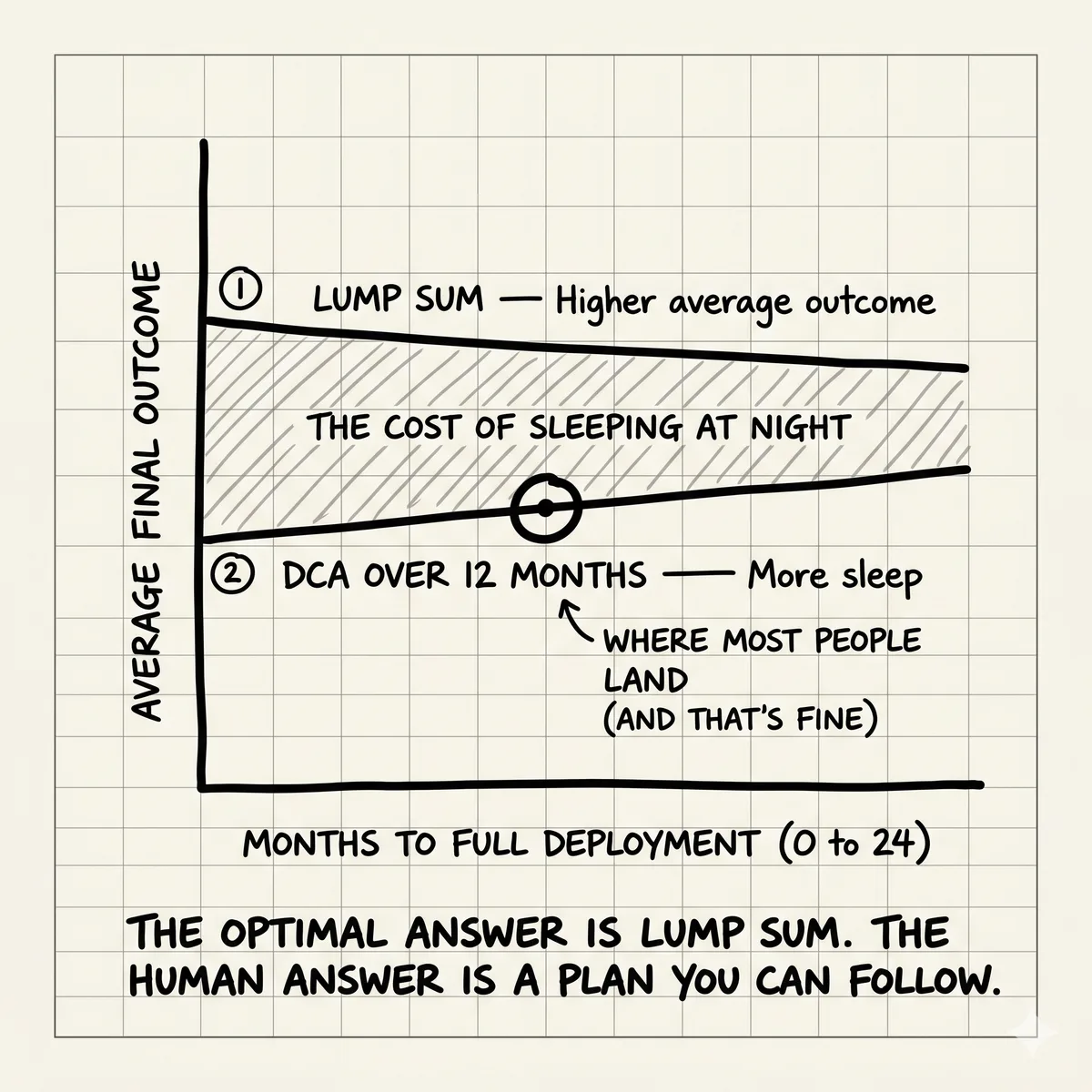

Lump Sum vs. Dollar-Cost Averaging

This is the question almost everyone asks when they inherit a large sum: "Should I invest it all at once or spread it out over time?"

The research is clear. Investing all at once (lump sum) outperforms dollar-cost averaging (spreading purchases over time) about two-thirds of the time over a 12-month period. The reason is simple: markets go up more than they go down. Every month your money is sitting in cash instead of invested is a month you are likely missing market growth.

The research is also clear that most people cannot emotionally tolerate lump sum investing after a windfall. Watching a $3M investment drop 15% in the first three months, even temporarily, is a different experience than watching a $3M portfolio drop 15% after it grew to that size over years. The unrealized loss feels catastrophic even when it isn't.

The honest answer: if you can sleep through the volatility, lump sum is statistically better. If you can't, dollar-cost averaging over 12 to 18 months is a reasonable tradeoff. You give up some expected return in exchange for not making a panic decision at the worst moment.

What you should not do: stay in cash for 24 months because you couldn't decide. That is the version where you get neither the math advantage nor the emotional comfort.

What You Actually Don't Need

A short list of things you do not need with $1M to $5M and a long time horizon:

- Alternatives (hedge funds, private equity, commodities funds) at this stage

- Separately managed accounts with custom "tax-loss harvesting algorithms"

- Annuities (almost never appropriate for inherited money)

- Whole life insurance as an investment vehicle

- Actively managed funds with sales loads

- Any product with a prospectus you can't summarize in two sentences

This list is not permanent. At $10M+ with specific tax situations, some of these tools become relevant. At $1-5M with a 20-year time horizon, they mostly add cost and complexity without proportionate return.

The Honest Limitation

This post is a starting framework, not a personalized plan. It doesn't know your tax situation, your existing investments, your mortgage rate, your income trajectory, or your goals. Those specifics matter. A three-fund portfolio is appropriate for many people. It may or may not be optimal for you.

If you have the kind of complexity that benefits from professional modeling (inherited IRA, real property, significant existing investments, business interests), a single engagement with a fee-only CFP is worth the cost. Not to manage your money permanently. To build a plan you execute yourself.

The point of this post is different. It is to make clear that the basic framework is not complicated. You don't need a finance degree to invest an inheritance well. You need low-cost diversified index funds, a reasonable asset allocation for your situation, discipline to not sell during downturns, and time.

That's most of it. The rest is refinement.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

The Portfolio Simplification Audit: From 15 Syndicates to Index Fund Zen

As net worth climbs past $5M, the greatest cost is mental overhead. Learn how to perform a simplification audit and shift from complexity debt to Index Fund Zen.

Concentrated Tech Equity: The Diversification Decision (With Math)

Your advisor says diversify. But diversification has a real cost. Here is the math on when holding wins, when selling wins, and what wealthy founders actually do.

H1B Homebuying: The 20-Year Math Nobody Runs

Visa uncertainty breaks conventional homebuying logic at year 5-7, not month 1. Nobody models the full timeline with immigration risk factored in — here's the math.