Liquidity Event Sequencing: Pre-Exit Tax Planning for Founders

Quick Answer

Liquidity Event Sequencing is the art of structuring major financial decisions *before* an exit, IPO, or windfall—not after. Most founders and early employees think about their liquidity event tax situation on the morning of close. By then, it's too late for most optimizations. The real value happens 12–18 months before close: charitable giving decisions, entity structure optimization, QSBS planning windows, and option exercise timing. The founder who sequences these decisions correctly walks away with 15–25% more after-tax wealth than the one who optimizes on close day. This is where deliberate planning creates outsized value.

Your company's Series C is closing in 18 months. The economics are good. You're likely to have an exit in 3–5 years. You should be planning for that now. Most people aren't. Most will optimize on day 1 of the exit. That's 18 months of missed opportunity.

Liquidity Event Sequencing is the practice of making *sequential* decisions in the 12–18 months before a known or anticipated liquidity event. Each decision creates optionality for the next one. Done correctly, sequencing compounds. Done incorrectly (or ignored), you leave substantial after-tax value on the table. The difference between intentional sequencing and ad-hoc decision-making is often $500K–$2M+ for founders with exits in the $50M–$500M range.

Why Sequencing Matters: The Decision Tree

Most exit planning is linear: exit happens → taxes are calculated → assets are allocated. But the real value comes from treating the pre-exit window as a decision sequence:

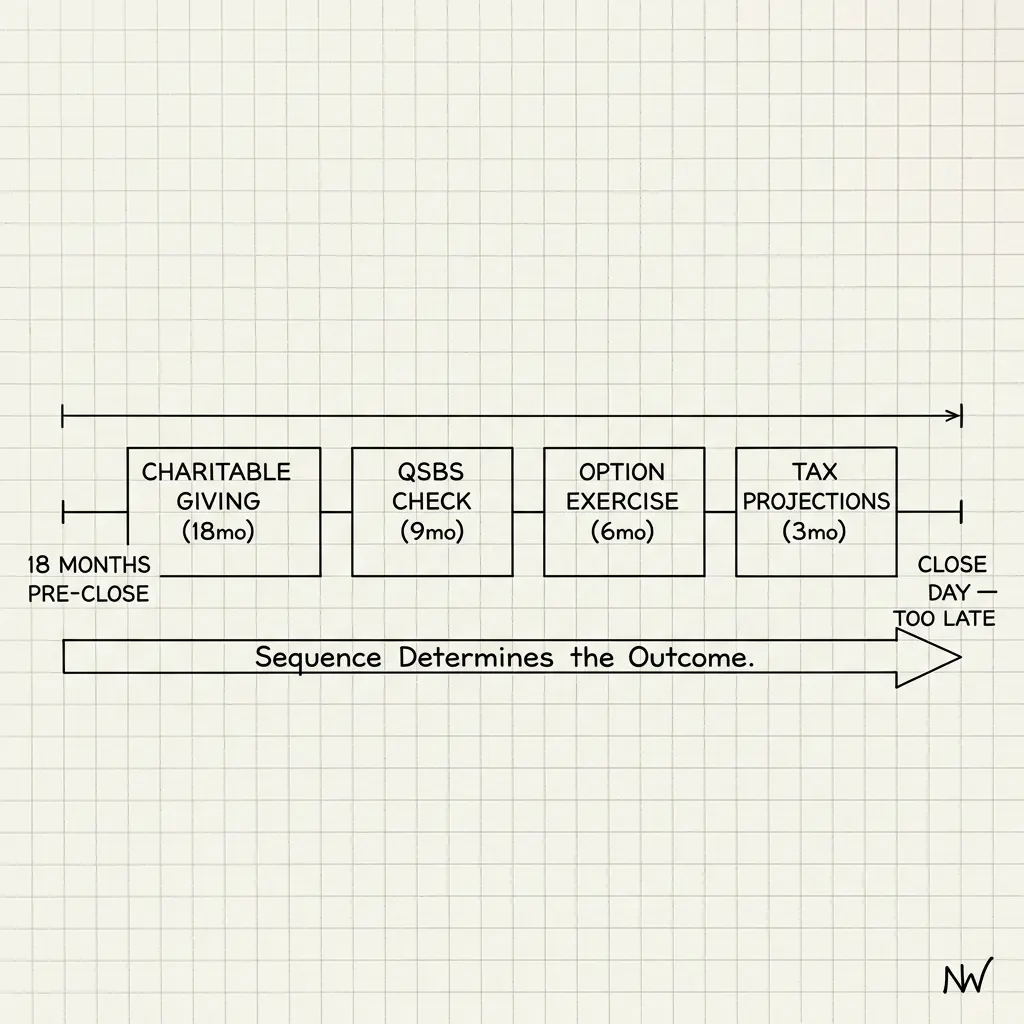

Decision 1 (Month -18 to -12): Charitable Giving Structure

Before you know your exact liquidity proceeds, establish a charitable donor-advised fund (DAF). You contribute appreciated stock or cash. You get an immediate tax deduction. Later, you direct the fund to give to charities. The timing flexibility lets you bunch charitable giving years before the exit (when your income is lower for tax purposes), then distribute from the DAF post-exit.

Value: Creating $200K in charitable deductions before exit saves $60K–$80K in taxes.

Decision 2 (Month -12 to -6): Entity Structure Review

Do you still need your current corporate structure (S-corp, C-corp, LLC)? Are there holding company optimizations? If the exit is taxable (stock sale vs. asset sale), the structure can affect whether you pay capital gains on your equity or ordinary income on the sale proceeds. Some founders can restructure before exit to lower the tax rate.

Value: Restructuring from C-corp to S-corp or from equity-based compensation to sale of partnership interests can save 5–15% on the exit proceeds.

Decision 3 (Month -12 to -3): QSBS Planning

Section 1202 Qualified Small Business Stock (QSBS) allows up to $15M in tax-free gains if you held the stock for 5+ years. If your company was founded 4 years ago and exit is planned for year 5, you might hit that window. But holding periods are strict—any sale before 5 years *disqualifies* the QSBS status retroactively.

Value: QSBS planning can save 20% on $1M+ in gains. That's $200K+ tax-free. But it requires knowing your timeline 12+ months in advance.

Decision 4 (Month -6 to close): Option Exercise Timing

If you have unvested options, the exercise window closes post-exit. The decision: exercise now (pay the strike price) or wait for the exit (exercise post-close with capital proceeds). The timing affects your tax liability and the composition of your post-exit wealth.

Value: Exercising pre-exit with anticipated tax loss harvesting can reduce the net cost of exercise by 15–25%.

Decision 5 (Post-close, Months 0–12): Asset Allocation and Diversification

Most founders receive liquidity in cash or acquirer stock. If acquirer stock, you have a 6-month lock-up. During that window, you're forced to hold concentration. After lock-up, diversification speed matters. If you diversify all at once, you trigger massive capital gains (if inside shares) or large amounts of stock sales at once (if restricted stock). Sequencing the diversification over 18–24 months post-close reduces timing risk.

Value: Gradual diversification vs. immediate liquidation can be worth 5–10% of the proceeds if the acquirer stock appreciates or depreciates unexpectedly.

The Sequencing Framework: What Depends On What

Here's the key insight: each decision creates *optionality* for the next decision. Decisions made early expand choices later. Decisions made late constrain them.

If you do charitable giving pre-exit:

You can deduct the gains on appreciated assets before exit. Post-exit, you can distribute from the DAF to charities without triggering gains. You've "converted" appreciation into charitable value.

If you don't structure the entity pre-exit:

The acquirer decides the structure of the deal (asset vs. stock sale). Your tax rate is determined by their choice, not yours.

If you understand your QSBS status 12 months pre-exit:

You can arrange the exit timing to maximize the holding period (if close). Or you can structure secondary sales (if far) to preserve QSBS treatment.

If you exercise options pre-close knowing tax-loss harvesting options:

You can offset exercise gains with losses in your personal brokerage portfolio. If you wait until post-close, you've lost that harvesting window.

Real Scenarios: How Sequencing Changes the Math

Scenario 1: Founder with $5M Exit Expected in 18 Months

Without Sequencing:

Exit closes. Founder realizes $5M in proceeds. Capital gains tax: 20% federal + 5% state = 25% = $1.25M. Net to founder: $3.75M. No planning. Default outcome.

With Sequencing (Charitable + QSBS):

Month -18: Establish DAF, contribute $200K in appreciated company stock (gets $200K deduction). Month -6: Exercise options pre-close, harvest losses in personal portfolio to offset exercise gains. Month +6 (post-close): QSBS planning ensures $3.5M of the $5M exit qualifies for zero capital gains (keeping $3.5M entirely). Remaining $1.5M taxed at 25%. Tax total: $375K. Net to founder: $4.625M. Difference: $875K.

Scenario 2: Early Employee with 4-Year Vesting, Year 4 Exit

Without Sequencing:

Options vest fully into sale. Capital gains tax: 25%. Net proceeds: $750K on a $1M option exercise value.

With Sequencing (QSBS):

Month -12: Confirm QSBS eligibility (granted 4 years ago, held 5+ years at exit). If exit structured as stock sale, gains qualify for QSBS exclusion. Net to employee: $1M entirely (zero capital gains). Difference: $250K.

The Decision Checklist: 18 Months Pre-Exit

Months 18–12 Pre-Exit

- Confirm company's exit timeline (rough estimate, not exact date)

- Review QSBS status: when was this company founded? Have you held for 5+ years?

- Establish a DAF if considering significant charitable giving

- Review current entity structure with tax counsel

- Identify any concentrated positions in personal portfolio for harvesting

Months 12–6 Pre-Exit

- Contribute to DAF (if applicable) to lock in pre-exit tax deductions

- Explore restructuring options if entity structure is suboptimal

- Confirm deal structure with acquirer (stock vs. asset sale if known)

- Review option exercise decision with an options specialist

- Harvest losses in taxable brokerage account to prepare for exercise

Months 6–Close

- Final review of QSBS timing (confirm 5+ year holding period)

- Exercise options if decided (post-loss-harvest)

- Confirm deal structure and tax treatment with CPA

- Plan asset allocation post-close (diversification schedule)

Months 0–12 Post-Close

- Manage lock-up period (if acquirer stock)

- Begin diversification on schedule (avoid timing risk)

- Direct DAF to charitable recipients (if applicable)

- File taxes with professional handling all QSBS, exercise, and sale mechanics

The Questions That Matter

Do you know your company's expected exit timeline?

If "maybe 3–5 years," start sequencing now. If "probably never" or "definitely next month," adjust accordingly.

Do you have QSBS-eligible equity?

If yes, understand the 5-year holding period. If you're close (4+ years), protect it. QSBS can be worth 15–25% of your exit proceeds.

Have you modeled the tax impact of the exit?

If not, get a CPA to run the numbers. Options vs. stock sale, charitable giving, QSBS timing all affect the outcome.

Do you have significant personal losses available for harvesting?

If yes, they're more valuable *now* than post-exit (because you might have lower income post-close, making losses less useful). Harvest early.

The Sequencing Principle

Liquidity Event Sequencing is based on one principle: *early decisions expand later options; late decisions constrain them*.

The founder who sequences 18 months pre-exit isn't playing luck. They're creating compounding optionality.

Each decision (charitable giving → entity structure → QSBS planning → option exercise → diversification) flows into the next. The cumulative effect is 15–25% more after-tax wealth than the founder who optimizes on day one. Most of that value is created before close, not after.

If your company might exit in the next 3–5 years—

You should be sequencing decisions now, not on day one of close. The planning value is 10x larger before exit than after.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

The 15-Year Tax Setup I Wish Someone Had Told Me

Rohit pulled up his 2009 W-2 not to look at the number — to look at the decisions he hadn't made yet. Wrong account type. Wrong entity structure. Wrong equity exercise timing. None of it was illegal. All of it was expensive. And none of it was fixable once the window closed.

The Transition Year Tax Map: Planning for the Income Gap

The first 12 months post-exit are a tax minefield. Sequence your income, deductions, and Roth conversions to avoid the 'Success Tax' that burns 10-20% of your final payouts.

Tax-Loss Harvesting: Behavioral Tool for Tech Employees

Real value isn't the $2K-$4K tax savings. It's the behavioral reset: you face underperforming positions and rebalance. Master the strategy that improves decision-making.