Mega-Backdoor Roth

A product guru didn't know it existed. A financial advisor colleague never mentioned it. The $1M+ lifetime tax shelter hiding in plain sight.

Adi's on the phone. He's a product genius—the kind of person who understands systems so deeply that he can see what's broken in them.

"Wait—that EXISTS?" he says, staring at his 401k documents.

"You mean I've been leaving $69K on the table every year?"

Yeah. He had. And he had an advisor.

The Information Asymmetry Problem

Here's the uncomfortable truth about wealth and taxes.

The reason rich people pay less in taxes isn't because they're smarter. It's because they can afford advisors who point out what they're missing.

Adi makes $400K a year. He's sophisticated. He reads financial research. He understands products deeply.

And he had no idea the mega-backdoor Roth existed.

Not because it's obscure. It's right there in his 401k plan documents. The plan administrator sends the details every year. It's available to anyone whose company offers it.

But it's invisible unless someone tells you to look for it.

That's the information asymmetry.

The wealthy don't get rich from discipline or intelligence. They get rich from knowing what to look for. And knowing what to look for costs money—either through advisors or through spending time researching what others have already figured out.

For Adi, that gap was worth $69K a year. Over 30 years of saving, that's $2.07M in contributions that could have gone into a Roth (and grown tax-free).

At 7% annualized returns, that $2.07M becomes $12.3M. Tax-free.

The difference between knowing and not knowing: roughly $12M in lifetime wealth.

And the only reason I knew to tell him was because I'd spent time researching it. Someone else had told me. The chain of information had eventually reached me.

He wasn't stupid. The system was just designed so the valuable information doesn't surface unless you're paying someone to find it.

How Mega-Backdoor Roth Works

The mechanism is simpler than the name suggests.

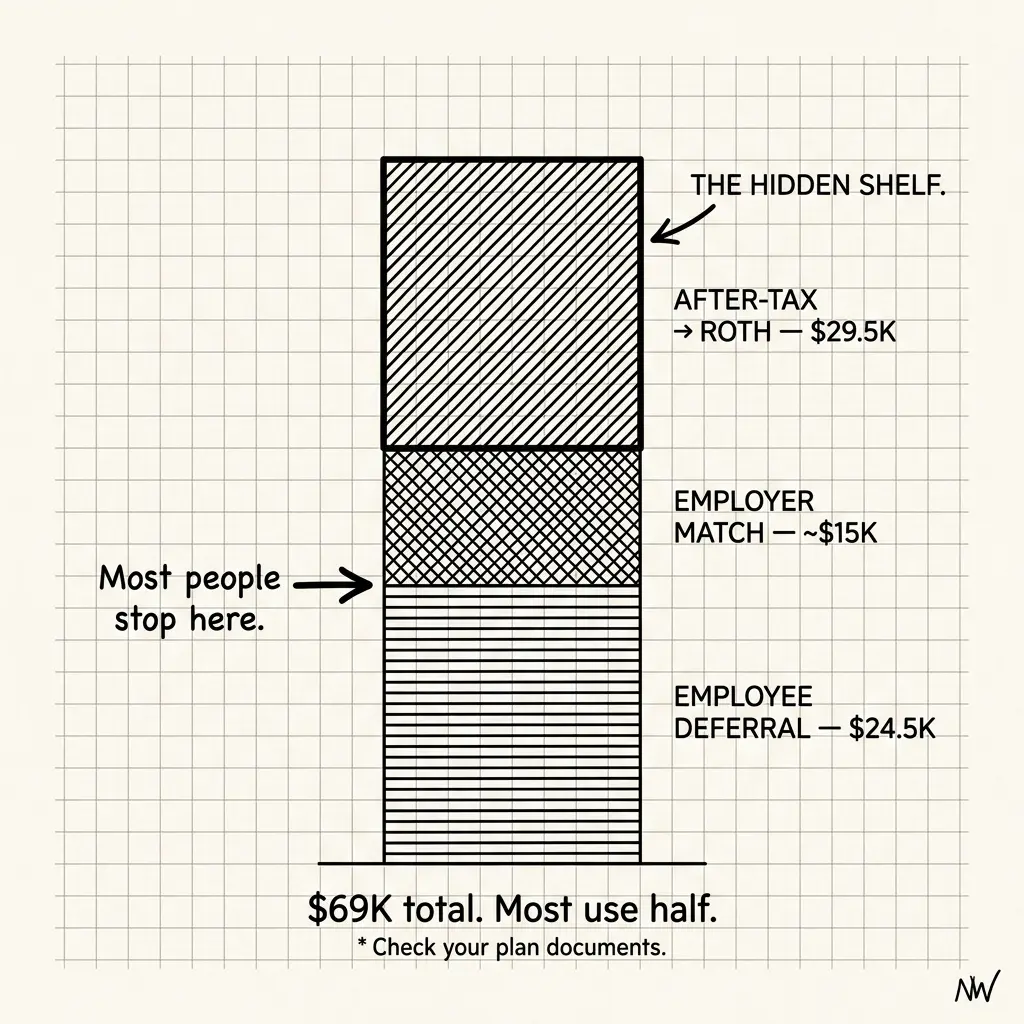

Your company's 401k plan has contribution limits:

- Employee deferral: $24,500/year (2026)

- Employer match: Up to 100% of compensation (varies by plan)

- Total limit: $69,000/year

Most people only use the employee deferral ($24,500). If their company matches, great—that's maybe $12K-$18K more. They're using $36K-$42K of the $69K total.

The mega-backdoor Roth is the lever most people don't touch: after-tax contributions.

Here's how it works:

Your plan allows you to contribute up to the $69K limit using after-tax money (money you've already paid income tax on). So if you've maxed your $24,500 employee deferral and your employer matched $15K, you can contribute another $29,500 in after-tax money.

Then—and this is the magic—most plans allow in-service distributions.

You can immediately convert that after-tax contribution into a Roth IRA.

You pay taxes on the growth (if any), but the $29,500 principal goes into the Roth tax-free. From that point forward, it grows tax-free forever.

The math:

- Year 1: Contribute $29,500 after-tax → Convert to Roth → Grows tax-free forever

- Year 2: Contribute another $29,500 after-tax → Convert to Roth → Grows tax-free

- Year 30: You've contributed $885K in after-tax money, and it's now worth ~$5.3M (at 7% returns)

- Tax bill on that $5.3M: $0

Compare that to a taxable brokerage account: That same $5.3M would owe roughly $1M+ in capital gains taxes when you eventually need to access it.

That's the lever. That's why Adi was shocked.

Why Most Plans Don't Make This Easy

Not every 401k plan offers mega-backdoor Roth. And that's intentional.

Plans that offer it tend to be at larger companies (tech, finance, established firms) where HR is sophisticated enough to set it up and employees are wealthy enough to use it.

Your company's plan needs two specific features:

- In-service distributions allowed (can you move money out while still employed?)

- Roth conversion option (can you convert to Roth, or just Traditional?)

Without both, you're stuck. You can contribute the after-tax money, but you can't convert it to Roth until you leave the company.

If you leave before converting, and your new company's 401k doesn't allow it, you're permanently locked into Traditional treatment. That after-tax $29.5K a year becomes pre-tax growth, subject to taxes when you withdraw it.

That's the trap. And it's why having a plan that allows mega-backdoor Roth is like having a cheat code.

Most people don't even know to check their plan documents.

How to Check Your Plan

Your company's 401k plan document is public information. You can request it from HR.

What to look for:

- "After-tax contributions" or "non-elective contributions" — This means the plan allows mega-backdoor

- "In-service distributions" — This means you can move money out while employed

- "Roth conversion option" — This means you can convert to Roth in-service

If all three are mentioned, your plan supports mega-backdoor Roth.

If only one or two are mentioned, you have a partial solution. Some plans allow after-tax contributions but don't allow in-service conversions (you'd need to wait until you leave the company).

Take the plan document to your CPA or tax advisor and ask: "Does this plan allow mega-backdoor Roth?"

If they hesitate or look confused, find someone else. This should be a 10-second answer for anyone competent.

The Real Message

Here's the uncomfortable truth: Adi didn't know because nobody had told him.

He wasn't ignorant. He was just operating with a different information set than someone who'd spent time researching tax optimization.

And that information gap is worth millions of dollars over a lifetime.

The mega-backdoor Roth exists in plain sight. It's legal, it's available, it's documented in your plan.

But you only benefit from it if you know to look for it.

That's the entire system. That's how wealth compounding actually works at the high end. Not through secret strategies or illegal loopholes. Just through knowing what already exists and taking advantage of it before someone tells you to stop.

Check your plan documents. Ask your advisor. If they don't know, find someone who does.

The $69K you contribute this year at 7% growth becomes $327K in 30 years. And it's all tax-free if you know the lever that exists.

Adi found out. He's doing it now.

How many people are leaving this on the table because they don't know it's there?

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

Backdoor Roth at $400K: Is It Worth It?

Backdoor Roth saves $1,400-$3,000 lifetime. But is it your best move with RSUs and ISOs already in play? Complete 2026 strategy guide for high earners.

Your EPF Balance Is Probably Taxable in the US. Nobody Told You.

The IRS has not issued clear guidance classifying EPF as a qualified pension plan. The conservative position: interest accruing annually in your EPF is US-taxable income, even if you haven't withdrawn a rupee. Most NRIs in the US have never reported it.

The RNOR Window: The 2-3 Year Tax Opportunity Most NRIs Miss

Your first 2-3 years back in India, foreign income is largely tax-free. It's the window for Roth conversions and asset restructuring. Almost nobody plans for it before they leave the US.