The Portfolio Simplification Audit: From 15 Syndicates to Index Fund Zen

Quick Answer

As your net worth climbs past $5M, the greatest cost to your wealth isn't taxes or fees. It is mental overhead. Most successful high earners accumulate a "complexity debt" of direct real estate, syndicates, and niche private deals that individually looked smart but collectively operate like a second job. A Portfolio Simplification Audit identifies where you are spending high-value mental energy for marginal alpha (extra return). True index fund zen is the understanding that once your downside is protected, the value of your time and peace of mind is the only metric that matters.

At $2M, complexity feels like sophistication. At $10M, it feels like a cage.

David spent 20 years building a mid-sized manufacturing business. He sold it for $18M. After taxes and a few years of investing, he found himself sitting on a "sophisticated" portfolio.

He had 14 different real estate syndicates (multifamily in Texas, self-storage in Florida, industrial in Ohio). He had two direct-owned rental properties in his home state. He had shares in three early-stage startups where he'd done "angel investing" to help friends. He had a primary brokerage account with 40 individual stocks his advisor picked and a separate account for "speculative crypto."

On paper, the diversification was beautiful. In reality, David was miserable.

Every March and April were a nightmare of chasing K-1s. He spent 15 hours a month reading quarterly reports from syndicators who all used different portals. He was still the one the property manager called when the HVAC died in his local rentals.

He had achieved financial independence, but he hadn't achieved mental independence. He had replaced one job (running his company) with another (managing his complexity).

The Goal of Wealth is to Stop Thinking About Money. David's Portfolio Forced Him to Think About it Daily.

The Efficiency Audit: Marginal Alpha vs. Mental Overhead

The 1% Trap

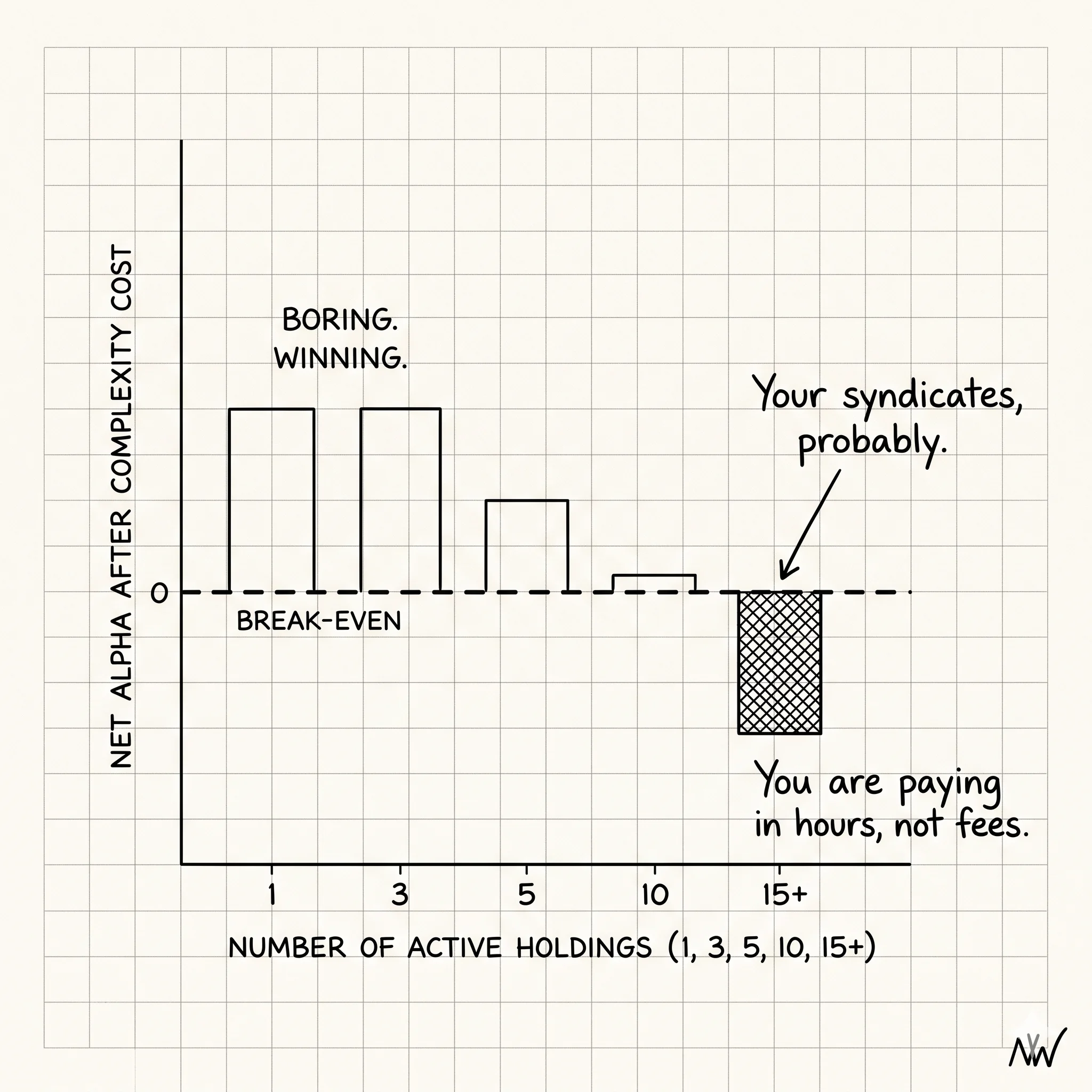

Many high earners justify complex private deals because they "might beat the S&P by 1-2%." On a $5M portfolio, that 1% is $50,000.

But what is the cost of that $50,000?

- Time: 120 hours a year in reporting, tax prep, and due diligence.

- Cognitive Load: The background anxiety of "Did I miss a capital call?" or "Is that tenant paying?"

- Illiquidity: The inability to pivot if your life goals change next week.

If your time is worth $500/hour, those 120 hours cost you $60,000 in opportunity cost alone. You are paying $60K to chase $50K. The math doesn't work.

Phase 1: Identifying "Zombie Assets"

Zombie assets are investments that are technically "alive" (they might even be cash-flowing) but are dead to your future strategy. They take up space on your balance sheet and in your brain without providing enough utility to justify the friction.

Primary Zombie: The Orphan Rental

The condo you lived in 10 years ago that you kept as a rental because "real estate is a hedge." It earns $800/month in net cash flow but requires 10 phone calls a year and a separate tax filing.

Secondary Zombie: The Legacy Syndicate

A $50K investment in a 2018 fund that has been "recapitalizing" for three years. You get a K-1 every year with $0 income, but you still have to pay your CPA $300 to process it.

Phase 2: The Consolidation Framework

Simplification isn't a weekend project. It's a strategic exit. You need to sequence your moves to minimize the "Exit Tax" (capital gains) while maximizing the "Peace Dividend" (reduced complexity).

Step 1: Set the "Index Fund Zen" Target

"I want 90% of my wealth in 3-4 highly liquid, tax-efficient index funds. I want 10% for high-conviction direct opportunities where I have a unique edge."

Step 2: Exit the Orphans First

Sell the direct-owned rentals. Use a 1031 exchange if the tax hit is massive, but only if you are moving into a truly passive structure (like a Delaware Statutory Trust). Or, better yet, just pay the tax and move to the index fund. The mental clarity is worth the check.

Step 3: Secondary Market for Syndicates

You don't have to wait 7 years for a syndicate to close. There is a deep secondary market for private equity and real estate interests. You might take a 10-15% haircut on value, but you gain 100% of your time back.

The Result of Simplicity

David performed his audit. He sold his rentals. He liquidated his angel shares on a secondary platform. He rolled 12 of his 14 syndicates into a single diversified REIT. He moved his brokerage to a 3-fund ETF portfolio.

His "on paper" return dropped by about 0.8% due to the loss of some specific leverage.

But his life return exploded.

He stopped checking his accounts every day. He stopped dreading tax season. When he travelled, he didn't check his email for "emergency" property repairs. He was finally, truly, retired.

Complexity is a Tax on Your Peace of Mind.

If your financial life requires a spreadsheet with more than 10 tabs, you aren't managing wealth. Your wealth is managing you. The audit starts with a simple question: If I liquidated this tomorrow and put it in a Vanguard Total Market fund, how much would I actually lose in dollars, and how much would I gain in life?

Run Your Wealth Like You Run Your Career. Optimize for Efficiency, Not Activity.

Is your portfolio a job or a tool?

The Portfolio Simplification Audit is how you reclaim your time. Start today.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

How to Actually Invest an Inheritance (Without a Finance Degree)

Low-cost index funds outperform most actively managed alternatives over any 15-year period. The three-fund portfolio and target-date funds are not cop-outs — they are the approach most economists would actually use. Here's the jargon-free version.

The Expat Financial Checklist: What Mid-Senior Professionals Get Wrong Before They Relocate

Everyone checks the cost-of-living calculator and the school ratings. Almost nobody reviews the financial decisions that need to be made before they leave — the ones with hard deadlines that disappear when the moving truck arrives.

Smart Debt at Scale

When you own $3M in paid-off assets, borrowing at 2.8% beats liquidating appreciated stock. Here's the math that changes the conversation about debt.