QSBS 2026: Maximize Your $15M Tax-Free Gain

You've heard of QSBS. Most founders and early employees have.

Fewer know the decision tree. Whether to early exercise. When the gross asset window closes. How stacking actually works across a family. What disqualifies stock most people assume qualifies.

This post is that decision tree — not an encyclopedia.

Quick Answer

Section 1202 Qualified Small Business Stock allows taxpayers to exclude up to $15M in capital gains (after recent legislative changes) from a single C-corp investment. Exclusions are now tiered: 50% at year 3, 75% at year 4, 100% at year 5. The gross asset threshold increased to $75M at issuance. The biggest opportunity most people miss: stacking exclusions across family members and trusts, and early exercising to start the holding period clock before the company's asset base grows past the threshold.

What Changed and Why It Matters Now

The original Section 1202 rules provided a 100% gain exclusion for C-corp stock held 5+ years from companies with gross assets under $50M at issuance — up to the greater of $10M or 10x your investment basis.

Recent legislation expanded this significantly:

$15M

Exclusion cap (up from $10M)

$75M

Gross asset threshold at issuance (up from $50M)

3-5yr

Tiered: 50% / 75% / 100% exclusion

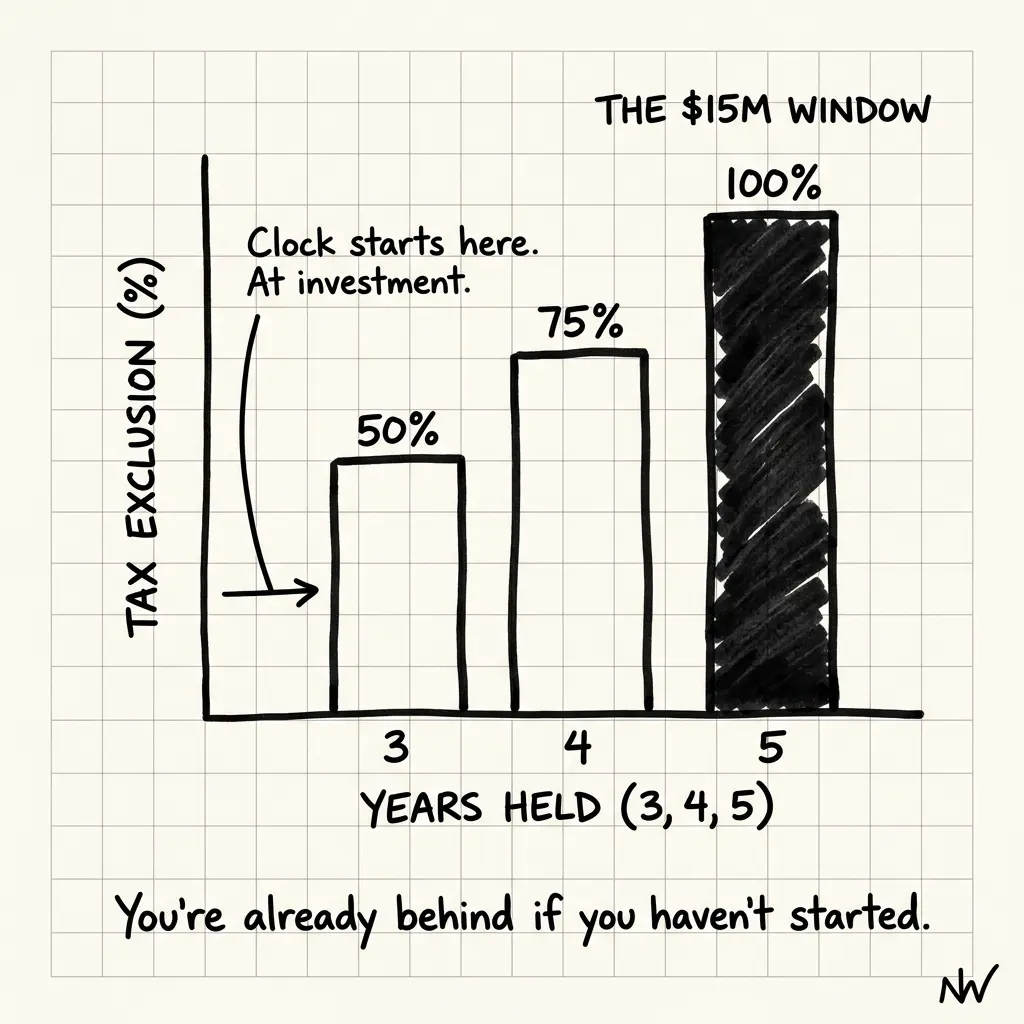

The tiered structure is new. You no longer have to hold for five years to get any benefit. At year three, 50% exclusion applies. Year four, 75%. Year five, 100%. This changes the decision calculus for founders and early employees managing liquidity needs.

Important: many states, including California, do not conform to federal QSBS rules. California taxes the full gain regardless of federal exclusion status. At 13.3% CA rate on gains that could be $15M, that's roughly $2M in state taxes that the federal exclusion doesn't touch. Know your state.

The QSBS Decision Tree

Most QSBS guides explain the rules. This one tells you what to do.

Decision 1: Does my stock actually qualify?

QSBS qualification has four requirements that all must be met:

→ Entity type: Must be a domestic C-corp at time of issuance. S-corps, LLCs, and partnerships don't qualify. Reorgs from LLC to C-corp: new holding period starts at conversion date.

→ Gross assets: Company gross assets must be under $75M at time of issuance and immediately after. Not current value — the book-value asset base at the time you receive the stock.

→ Original issuance: Stock must be acquired directly from the company (primary issuance). Secondary market purchases — even of stock that originally qualified — do not qualify for the buyer.

→ Active business: The company must conduct an active trade or business at time of issuance. Excluded industries include: professional services (law, health, accounting, financial services, engineering), hospitality, and certain other service businesses. Most tech companies qualify. Many consulting and services companies don't.

Decision 2: Should I early exercise to start the clock?

The holding period starts when you acquire the stock — not when options vest. If you have unvested ISOs or NSOs in a company with gross assets under $75M, early exercising starts your 3-5 year holding period now.

The risk: if you exercise and the company fails, you've paid real money for worthless stock. The 83(b) election (filed within 30 days of exercise) locks in a low ordinary income tax basis and starts the clock — but doesn't protect against the company failing.

Early exercise makes sense when: Company gross assets are approaching $75M (the window may be closing), the current strike price is low (limiting ordinary income on exercise), and you have reasonable confidence in the company's survival.

Decision 3: Hold at year 3, 4, or 5?

With tiered exclusions, the decision calculus is now: what is the value of selling one year earlier vs. the additional exclusion benefit of holding?

At year 3 vs. year 5 on a $15M gain: 50% exclusion vs. 100% exclusion = $7.5M difference in taxable gain. At 37% federal, that gap is worth ~$2.8M. If the company might fail or be acquired in years 4-5 at a lower valuation, that calculus shifts. The Section 1045 rollover (within 60 days of year-3 sale, reinvested into another QSBS company) lets you preserve the holding period if you need liquidity now.

The Stacking Play: Up to $45M Tax-Free from One Company

The $15M cap applies per taxpayer per issuing company. "Per taxpayer" is the key phrase.

Stacking Mechanics:

Founder: $15M exclusion

+ Spouse (with separate shares): $15M exclusion

+ Non-grantor trust (with separate shares): $15M exclusion

= $45M in total federal exclusions from a single company

This requires careful planning before a liquidity event. The shares must be separately held by each taxpayer or trust — you can't gift shares post-sale and retroactively claim multiple exclusions. Transfers to a spouse can maintain the holding period under certain conditions; transfers to trusts require careful structuring.

The gift tax implications of transferring QSBS shares are real. Transfers above the annual exclusion ($18,000 per recipient in 2026) use lifetime exemption or require gift tax returns. Get a tax attorney involved before transferring QSBS shares to family members or trusts.

Disqualification Risks You Might Not Know

QSBS status can be retroactively lost. Here's what most guides don't emphasize:

Company stock redemptions

If the company repurchased stock from you or another 5%+ shareholder within 2 years before or after your QSBS shares were issued, your shares may be disqualified. This catches founders in acquisition scenarios where part of the deal is a stock redemption.

Industry pivots into excluded businesses

If the company pivots into a professional services or financial services business after your shares were issued, and more than 80% of company assets become dedicated to an excluded industry, the QSBS status can be affected. Monitor company direction if you're in a holding period.

Gross asset test at issuance, not current value

The $75M threshold applies at the time of stock issuance, not current company value. A company that was worth $40M when you received stock may now be worth $500M — and the stock still qualifies. But if the company's book-value assets exceeded $75M on the date your specific grant was issued, those shares don't qualify even if you didn't know it then.

Documentation requirements for audit defense

IRS audits of QSBS claims require: original stock purchase agreement, 83(b) election copy (if applicable), company attestation letter confirming gross asset status at issuance, and evidence of active business qualification. Many founders discover at exit — when it's too late — that they don't have the attestation letter. Get it before the company changes hands.

FAQ

Can I claim QSBS on stock I received as RSUs, not options?

Yes, if the underlying company stock otherwise qualifies. RSU shares received from a qualifying C-corp count as QSBS. The holding period starts when the RSUs vest and shares are received, not when the RSU was granted. For early employees receiving RSUs at a company with assets well under $75M, this is often QSBS even if nobody told you.

What is the Section 1045 rollover and when does it make sense?

If you sell QSBS after the 3-year minimum holding period but before 5 years, Section 1045 lets you roll the proceeds into another QSBS company within 60 days and defer the gain. The holding period from the original stock tacks onto the replacement stock. This is valuable if you need liquidity from a year-3 sale but want to preserve the full 5-year exclusion chain.

California doesn't conform to QSBS — what does that mean practically?

It means your federal exclusion applies to your federal return, but California taxes the full gain regardless. On a $15M gain excluded federally: $0 federal capital gains tax, but ~$2M in California income tax. This is still a significant benefit — but not zero state tax. Know your state's conformity status before assuming QSBS is completely tax-free.

Does AMT affect QSBS gains?

Pre-2010, 7% of the QSBS exclusion was an AMT preference item. The Tax Relief Act of 2010 eliminated this. As of 2026, 100% excluded QSBS gains don't create AMT preference items. This was one of the most significant pro-QSBS tax changes in the last decade.

The document your tax advisor needs before your exit:

A company attestation letter confirming the gross asset status at the date of each stock issuance. This single document is the foundation of your QSBS audit defense. Most companies can provide it. Most founders don't ask for it until after the company is acquired and nobody answers the phone.

Ask for it now. Keep it with your equity grant agreements and 83(b) election copies.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

Liquidity Event Sequencing: Pre-Exit Tax Planning for Founders

Real exit tax savings (15-25% of proceeds) come from decisions 12-18 months before close. Master charitable structures, entity optimization, QSBS timing, and option planning.

Tax-Loss Harvesting: Behavioral Tool for Tech Employees

Real value isn't the $2K-$4K tax savings. It's the behavioral reset: you face underperforming positions and rebalance. Master the strategy that improves decision-making.

Cross-Border Job Move: Tax Planning for Expat Equity

Moving abroad with equity triggers cascading complications: tax residency, retirement rules, filing obligations. Master the 18-month planning window and avoid $20K-$100K surprises.