You're Returning to India. Your RNOR Window Is Open. Here Is the Exact Sequence of Decisions.

The RNOR window is not a status. It's a planning window with an expiry date, and the most valuable actions happen before it opens, not during it.

Sunita returned to Bengaluru in October 2024. She had read the RNOR article. She knew the broad concept. By January 2025, she was filling out her Indian tax return with her CA. He asked about her US retirement distributions. She said she'd waited — she wasn't sure of the timing. He explained that the RNOR window might be optimal for 401K distributions. She asked how much she could take. He said it depended on what India would say about each account type, which depended on when she took it, which depended on when she'd returned and how long she'd been abroad.

She had all the information. Nobody had synthesized it into a sequence.

This post is the sequence.

What the RNOR Window Actually Is

Resident but Not Ordinarily Resident (RNOR) is an Indian income tax status. It's a transitional category for people who have been abroad for an extended period and have recently returned. You are RNOR — not a full Indian resident — if you meet either of these conditions during the tax year:

You have been a non-resident in India for 9 of the 10 preceding financial years, OR you have been in India for 729 days or fewer during the 7 preceding financial years.

For most NRIs returning from the US after 8+ years, the first condition applies. RNOR status typically lasts 2 years, sometimes extending to 3 years for very long-term non-residents. The clock starts from the financial year of return, not from the date you arrive.

The practical effect: during RNOR, income earned or received outside India is generally not taxable in India. Your US-sourced salary from a US job that you stopped before returning isn't taxable. Your US brokerage gains on non-Indian assets may not be taxable in India during RNOR. Your 401K distributions — sourced to the US — may benefit from this treatment.

"May" is the careful word here. The RNOR exemption applies to foreign income. Whether a given account's income counts as "foreign income" under the specific India-US DTAA treatment matters. The 401K analysis is the most important.

401K Distributions During RNOR: The Main Event

The US-India Double Taxation Avoidance Agreement (DTAA) covers pension and retirement income under Article 20. India has the right to tax pension distributions received by Indian residents from US sources. The treaty prevents double taxation — meaning if India taxes you, the US doesn't also tax the same income at full rates.

During RNOR, the analysis works like this: the US will withhold 10% on 401K distributions when you're a non-resident alien (the DTAA reduced withholding rate). India, technically, has taxing rights. But during RNOR, foreign-source pension income falls under the RNOR exemption for most practitioners' reading of the law — it's foreign income and you're RNOR. India doesn't tax it. The 10% US withholding is the effective tax rate.

Versus: distributions taken after your RNOR window expires and you're a full Indian resident. India taxes 401K distributions as ordinary income under Article 20. US withholding is credited, but you pay the difference to India if Indian rates are higher (they are — Indian top marginal rate is 30% plus surcharge).

The difference on a $200K distribution: 10% effective rate during RNOR vs. 30%+ effective rate after. That's $40,000+ on a single distribution.

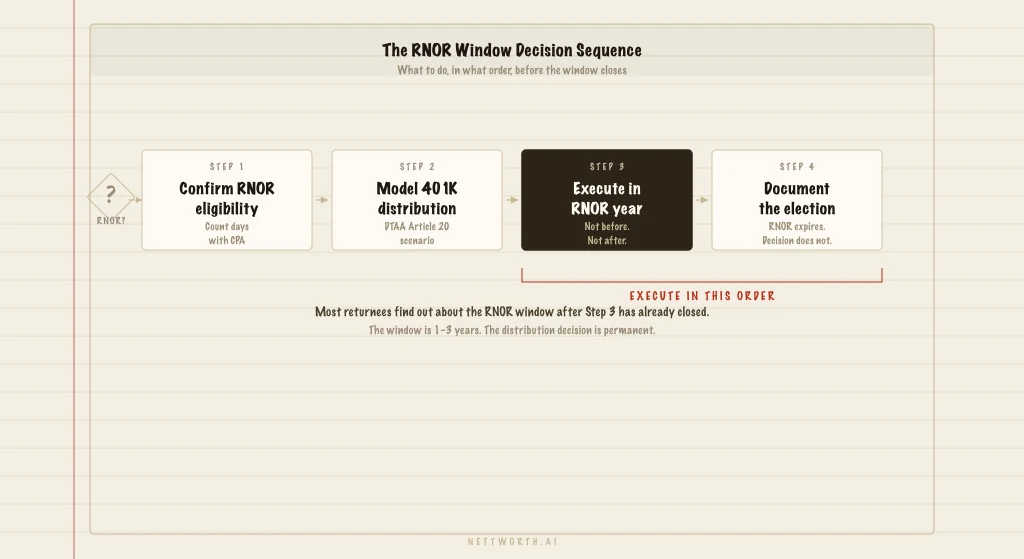

The strategic implication is clear: take 401K distributions during your RNOR window. The question is how much and in what sequence.

The disclaimer you need to read

The RNOR treatment of foreign pension income is not settled black-letter law. Multiple practitioners take slightly different positions on the mechanics. The broad consensus is that 401K distributions during RNOR are taxed only in the US (at the 10% DTAA rate), not additionally in India. But individual fact patterns matter, the tax authority's current administrative interpretation matters, and the specific structure of your 401K matters. This post gives you the framework for the conversation with your cross-border CPA — it doesn't substitute for it.

RSU Income During RNOR: This One Doesn't Help You

If your RSUs continue to vest after you return to India (because you have ongoing unvested grants from your US employer), the US-sourced portion of that income does NOT benefit from the RNOR exemption.

Why: RSU income sourced to US workdays is US-sourced employment income. The RNOR exemption covers foreign income earned outside India. US-sourced RSU income from a US employer, based on US workday calculations, is income the US has already established taxing rights over. India taxes it under Article 20 as employment income. The RNOR "foreign income" exemption doesn't override the sourcing analysis.

The practical implication: if you have significant unvested RSUs and you're planning your India return, the RSU acceleration or deferral decision needs to happen before you return, not during RNOR. This is part of the pre-departure sequence covered in the 18-month countdown below.

Roth Conversions: The Move That Has to Happen Before You Leave

This is the most frequently missed planning move.

A Roth conversion — rolling a traditional 401K or IRA balance into a Roth account — is a taxable event in the year you convert. You pay income tax on the converted amount at your current marginal rate. After conversion, the Roth account grows tax-free, and qualified distributions are tax-free in the US.

The problem for India returnees: the US-India DTAA has no Roth provision. India doesn't recognize Roth accounts as tax-exempt. If you take Roth distributions while an Indian resident, India taxes those distributions as ordinary income. The US doesn't double-tax you (you already paid tax at conversion), but India can and does tax the distribution.

The strategy: do Roth conversions before you return to India, while you're still a US resident. Specifically, do them in a year when your US income is low — a year between jobs, a year when you've accepted the India role but haven't started yet, or the year you formally resign from US employment.

The converted amount grows tax-free in the US. If you later take Roth distributions as an Indian resident, India may tax them — but the growth that occurred in the Roth account accrued tax-free, and you locked in a lower US marginal rate at conversion. The window to do this is US-residency. Once you're an Indian resident, converting a traditional 401K to Roth is still possible but you pay India's rates on the conversion income. That's worse.

How much to convert: evaluate how much traditional 401K balance you have vs. what you plan to take as distributions during RNOR. If your plan is to take $150K per year in 401K distributions during a 2-year RNOR window, leaving the remaining balance unconverted and distributing later is the question. The math depends on: current US marginal rate on the conversion, India's treatment of future distributions, and whether you expect your India income to push you into higher Indian tax brackets after RNOR.

Brokerage Capital Gains: Timing and Sourcing

US brokerage gains on US-listed securities are US-taxable regardless of your residency status — the US taxes non-resident aliens on US-source income. Capital gains from US stocks and ETFs are US-taxable for you whether you're in India or the US.

India's RNOR exemption applies to gains on non-US assets during the RNOR period. If you held UK stocks, Singapore REITs, or non-US assets in a non-US brokerage account, gains realized during RNOR may be exempt in India. These are niche cases for most NRIs returning from the US who hold primarily US-domiciled assets.

The practical action: if you hold appreciated positions in non-US assets, evaluate realizing those gains during RNOR. If you hold primarily US-listed assets, the timing doesn't change the India tax picture (it's US-taxable regardless), but it affects the US capital gains rate you pay — realize long-term gains while you still have favorable US rates if you expect your income to drop after return.

The 18-Month Countdown Sequence

18 Months Before Return: Roth Conversion Window

If you're going to do Roth conversions, this is the time. You're still a US resident with US-income-level tax rates. You may be in a lower-income year (transitioning jobs, taking a gap before return). Calculate how much to convert: enough to shift traditional balance into Roth while staying at a tax rate lower than what you expect India to impose after RNOR expiry.

Also at 18 months: review your RSU vest schedule. What vests in the next 18 months before you return? What vests in the first 2 years after return? If significant unvested grants will vest while you're in India, model the tax exposure. Consider whether acceleration makes sense — RSUs vested before departure are taxed at US resident rates, not at NRA withholding rates.

6 Months Before Return: 401K Distribution Strategy

Map your 401K balance against your estimated RNOR window duration (2 or 3 years). How much can you distribute per year without bumping into a tax bracket problem? The US withholds 10% on 401K distributions to non-resident aliens under the DTAA rate. India's treatment during RNOR: see the discussion above. Plan annual distribution amounts.

Also at 6 months: state tax residency. If you're in California, New York, or another high-tax state, terminate state residency before departure. The RNOR window doesn't help you with state taxes. California in particular will pursue residency claims. Clean exit before you leave.

Month of Return: RNOR Clock Starts

Your RNOR status begins in the financial year of your return. India's financial year runs April 1 to March 31. If you return in October, you have roughly 6 months left in the financial year before the RNOR year 1 tax year ends. The second full financial year after return is RNOR year 2 (or year 1 depending on how you count).

Track the date carefully. The RNOR window calculation depends on your specific return date and your years abroad. Verify your RNOR eligibility and window duration with your Indian CA in the first month after return.

RNOR Year 1: Maximize 401K Distributions

Take the first year of distributions at the rate your CA recommends given your overall income picture. The US withholds 10% via Form W-8BEN (or equivalent). Report on Form 1040NR as a non-resident alien. Confirm with your India CA how this income is reported on the Indian return for RNOR filers. Don't assume your India CA knows the US withholding mechanics — cross-border coordination matters here.

RNOR Year 2 (and Year 3 if applicable): Complete the Strategy

Continue distributions per your plan. Also in this period: evaluate what remains in traditional 401K vs. Roth. If RNOR expires while you still have significant traditional balance, the distributions after RNOR become subject to India tax. Build your distribution schedule to take what you reasonably can during the window, not so fast that you're taking unneeded distributions (generating US tax at 10% is fine; the US taxes you regardless).

Also in this period: don't trigger Indian resident status early by mistake. Days spent in India count toward the 182-day India residency threshold. If you're traveling and spending time in other countries, those days don't count toward your India total. Keep a calendar. You want to use the full RNOR window, not exit it accidentally by being in India for more days than you realize.

What the Sequence Looks Like in Practice

Sunita had $280K in her traditional 401K and $80K in a Roth. She returned in October 2024. Her RNOR window: 2 years (through March 2027). Her Roth conversion: she'd done $60K in 2023 when her income was lower than usual. That Roth balance grows tax-free in the US indefinitely.

Her 401K distribution plan: $80K per year over 3 years. Year 1 (RNOR, FY24-25): $80K, 10% US withholding = $8K, India treatment: RNOR foreign income exemption. Effective rate: 10%. Year 2 (RNOR, FY25-26): another $80K, same structure. Year 3 (post-RNOR, FY26-27): $80K, US 10% withholding, India taxes the distribution at her marginal Indian rate (30%), credits the 10% US withholding, owes 20% to India. Effective rate: 30%.

The difference between taking the third tranche in year 2 (during RNOR) versus year 3 (after RNOR): 20 percentage points of tax. On $80K: $16,000. She adjusted her schedule to take the third distribution in year 2 of RNOR.

The CA had given her the pieces. The sequence gave her the synthesis. That's the difference between knowing about the RNOR window and using it.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

Before You Leave the US for India: The RNOR Window, the 401K Decision, and Everything Else

Vikram had spent 11 years at Microsoft. He knew about the RNOR window — he found out about it 14 months after returning to Pune. The first two 401K distributions had already been taxed at India's full marginal rate. The RNOR window had been open. He hadn't known what to do with it. This checklist is for the version of Vikram who's still in the US.

Your H-1B Is In Transfer. You Have 60 Days. Here Is What To Do With Your Money.

Kevin got the layoff message Thursday at 4pm. He called his immigration attorney immediately. He didn't call anyone about his financial situation. Six months later: a corrected W-2 with 30% NRA withholding on RSUs he hadn't known had accelerated. The 60-day grace period is also a financial window. Nobody told him.

Before You Leave the US for the Netherlands: The 30% Ruling Doesn't Do What You Think It Does

Sarah moved from New York to Amsterdam and was excited about the 30% ruling. Then her US CPA explained: the ruling reduces Dutch income tax — which reduces the Dutch foreign tax credit she can apply against her US liability. In some income bands, the US takes more, not less. And the ruling application window is exactly 4 months from day one. Miss it permanently.