RSU Disposition: Sell to Cover vs. Same-Day Sale

The form came during onboarding. Page four of the equity plan documents. Three options. A default pre-selected. You signed.

Most people don't change the default. Sell to cover. HR presents it as the responsible middle ground — not too aggressive, not too conservative.

The problem: sell to cover at 22% withholding, when you're in the 37% bracket, means you're deferring a five-figure tax liability to April. Every vest. Every year.

Let's fix this.

Quick Answer

At vest, you have three choices: same-day sale (all cash, no shares retained), sell to cover (sell enough to pay withholding, keep the rest), or hold (pay taxes from other cash, keep all shares). The right choice depends on your marginal tax rate, available capital losses, stock concentration in your portfolio, and cash position. For most HENRYs in the 37% bracket, the withholding gap is real, concentration risk is underestimated, and the answer changes with every vest.

The Withholding Gap Nobody Warns You About

Your company withholds RSU taxes at the IRS supplemental wage rate: 22% federal. Some employers escalate to 37% for high-earners. Most don't.

At $350,000 in total income — W-2 plus RSU vesting — you're in the 37% federal bracket. California adds 13.3%. New York adds 10.9%.

Here's the math on a $200,000 RSU vest:

// The Withholding Gap

Vest value: $200,000

Company withholds at 22% federal: -$44,000

CA state (~9.3%+): -$22,000

You think you're covered.

Actual federal tax owed (37%): -$74,000

Gap: $30,000 — due in April, with potential underpayment penalty

This isn't an edge case. It's the default outcome for anyone in the top brackets whose RSUs are withheld at the supplemental rate. The onboarding form didn't mention this.

The withholding gap is why April is expensive for HENRYs — not because taxes are high, but because the collection mechanism is miscalibrated for their bracket.

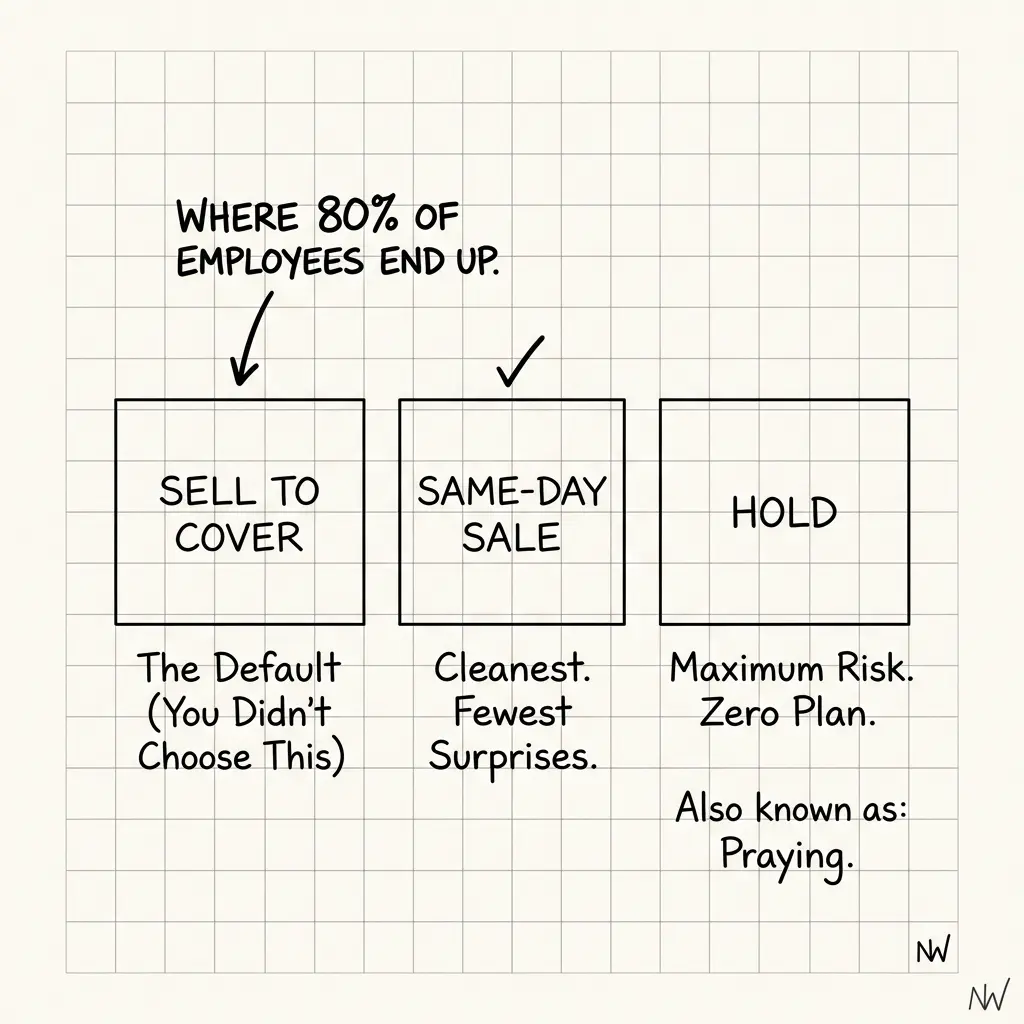

The Three Options, Actually Explained

Option 1: Same-Day Sale

All shares sell at vest-date price. You receive cash equal to the full vest value minus withholding. Zero shares retained.

Tax treatment: 100% ordinary income at vest value. No capital gain created — no holding period to trigger one.

Best when: You have capital losses available to offset future gains. You want immediate diversification. Your employer stock already represents more than 10% of your net worth. You believe the stock is fairly valued.

Option 2: Sell to Cover (the default)

You sell enough shares to cover the tax withholding. You keep the rest.

Tax treatment: Ordinary income on full vest value. Future appreciation on retained shares = capital gain (short-term until 12 months held; long-term after that).

Best when: You want equity exposure and don't have cash to cover taxes out-of-pocket.

The trap: If company withholding is 22% but your marginal rate is 37%, you've created a $30,000 April liability. The taxes aren't handled — they're deferred.

Option 3: Hold (Cash Exercise)

You pay the full tax bill from other cash sources. You keep all vested shares.

Tax treatment: Ordinary income on full vest value at vest date. All future appreciation above vest-date value is capital gain.

Best when: You have sufficient liquid cash. You have strong conviction on the stock. Company stock represents less than 10% of your net worth.

The trap: Concentration risk compounds silently. Every "hold" decision layers more single-stock exposure. At 20%+ of net worth in one security, you've made a concentrated bet you didn't consciously choose.

The Concentration Risk Calculation

Before each vest date, run this number:

(Existing company stock + This vest value) ÷ Total net worth

If that ratio is above 10%, "hold" requires explicit justification — not just conviction in the company.

If it's above 20%, you're running a concentrated single-stock portfolio whether you intended to or not.

Institutions cap single-security exposure at 5-10% for good reason. A company that's both your employer and your largest investment means a bad quarter at work hits your paycheck and your net worth simultaneously. That's not a bet — it's a structural fragility.

What Most People Get Wrong

Sell to cover feels responsible. The moderate choice. Not greedy, not reckless.

But moderate is not a tax strategy. Moderate at 22% withholding when you owe 37% is a deferred liability disguised as a decision.

Same-day sale feels like abandoning confidence in your company. But if you have capital losses available, same-day sale followed by a strategic repurchase after the 30-day wash sale window can be more tax-efficient than holding — because you avoid the future ordinary income wedge entirely.

Hold feels like conviction. Sometimes it is. Sometimes it's concentration risk masquerading as conviction.

The answer isn't about your feelings about the company. It's about your specific tax situation, your portfolio composition, and whether the default form you signed in onboarding still makes sense for who you are now.

The RSU Decision Checklist (Before Each Vest)

What is my actual marginal federal + state rate including this vest as income? (Not the company withholding rate — my real rate for this dollar.)

Do I have capital loss carryforwards available from prior years?

What percentage of my total net worth is employer stock, post-vest?

Do I have sufficient liquid cash to cover the full tax bill if I choose hold?

Is there a QSBS or ISO holding period I'm managing this year that affects the sequencing of taxable events?

If you can answer all five, you're making an informed decision. If you can't, you're guessing. And guessing on a $200,000 taxable event is expensive.

FAQ

Can I change my RSU disposition election between vesting events?

Usually yes. Most equity administration platforms (Schwab Equity, E*TRADE Stock Plan, Shareworks, Morgan Stanley At Work) allow you to change your election before each vest date. You cannot change after the vest executes. Check your platform's deadline — often 2-5 business days before vest.

My company only offers sell to cover. What do I do about the withholding gap?

Some companies restrict choices, especially pre-IPO. If sell to cover withholds at 22% and your marginal rate is higher, make estimated tax payments (IRS Form 1040-ES) by the quarterly deadline. Q1 deadline is April 15, Q2 is June 16, Q3 is September 15, Q4 is January 15 of the following year. Paying late costs ~8-9% annualized in penalties.

What's the wash sale rule and how does it affect RSU decisions?

If you sell RSU shares at a loss within 30 days before or after buying substantially identical stock, the loss is disallowed. In practice: same-day sale at vest has no loss to disallow (vest value = cost basis). The wash sale rule matters more when you're tax-loss harvesting existing position declines, not typically on the vest-day transaction itself.

If I hold my RSUs for 12 months, do they get long-term capital gains treatment?

Partially. The vest-date value is always ordinary income — regardless of when you sell. Only appreciation above the vest-date value qualifies for long-term capital gains treatment after a 12-month holding period. Example: 1,000 RSUs vest at $50 ($50,000 ordinary income). You hold and sell at $65 twelve months later. The $15,000 gain above $50 is long-term capital gain at 15-23.8% (depending on income level) rather than ordinary income at 37%.

Does RSU income affect the NIIT?

RSU ordinary income is W-2 income — it doesn't directly trigger the 3.8% Net Investment Income Tax. But it pushes your total income higher, which can drag investment income you already have (dividends, capital gains, interest) into NIIT territory above the $200,000 single / $250,000 MFJ threshold. Factor this into your total effective rate calculation.

Managing ISOs, NSOs, or QSBS alongside RSUs?

RSU decisions don't exist in isolation. The Equity Comp Decision Stack covers how to sequence all your equity instruments in the same tax year — because the order of operations changes the total bill.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

Concentrated Position Paradox: Managing Single-Stock Wealth Risk

Conviction vs. concentration risk: when 30% of net worth is in one stock, behavioral lock-in clouds every financial decision. Master diversification without abandoning company belief.

Equity Comp Decision Stack: ISOs, RSUs, NSOs, QSBS

Six decision windows per year: ISOs, RSUs, NSOs, and QSBS must be coordinated. Master the decision order that saves $100K+ in the same tax year.

What AI Lab Employees Are Actually Doing With Their Equity

S has $3.2M in unvested equity at a major AI lab and genuinely doesn't know what to do. Not because she's unsophisticated — because nobody around her is being honest. Three camps, one clear pattern, and what peer data actually solves here.