RSU Sourcing: How Your Workdays Between Grant and Vest Determine Your Tax Bill Across Two Countries

There is a formula. It's based on your workdays, not where you live when the shares vest. Your employer may or may not be running it correctly.

Ananya's grant was $400K on the day she joined. Three years in Bangalore before the San Francisco transfer. RSUs granted in India, vesting over four years. By year two she was in California. The W-2 showed Box 1 income she didn't understand. Her tax preparer pulled out a workday ratio. Ananya had never heard of sourcing allocation before that conversation.

Most people in Ananya's situation hadn't heard of it either. The rules aren't obscure — the IRS established the sourcing principle for equity compensation decades ago and has applied it consistently. What's obscure is that nobody in the vesting chain has an incentive to explain it to you. Your employer's payroll team runs a calculation. Your equity platform shows you a vest. Your CPA reports the income. The sourcing allocation happens in the background, and if it's wrong, you usually find out through a corrected W-2 or an unexpected tax bill.

This post explains how sourcing allocation works, how to calculate it yourself, and how to verify whether your employer is getting it right.

The Principle: Services, Not Residency

RSU income is sourced to the period of services rendered between the grant date and the vest date. This is the IRS's longstanding position on equity compensation, derived from Revenue Ruling 74-9 and extended through subsequent guidance. The income isn't sourced to where you live when the shares vest. It's sourced to where you worked during the time the shares were being earned.

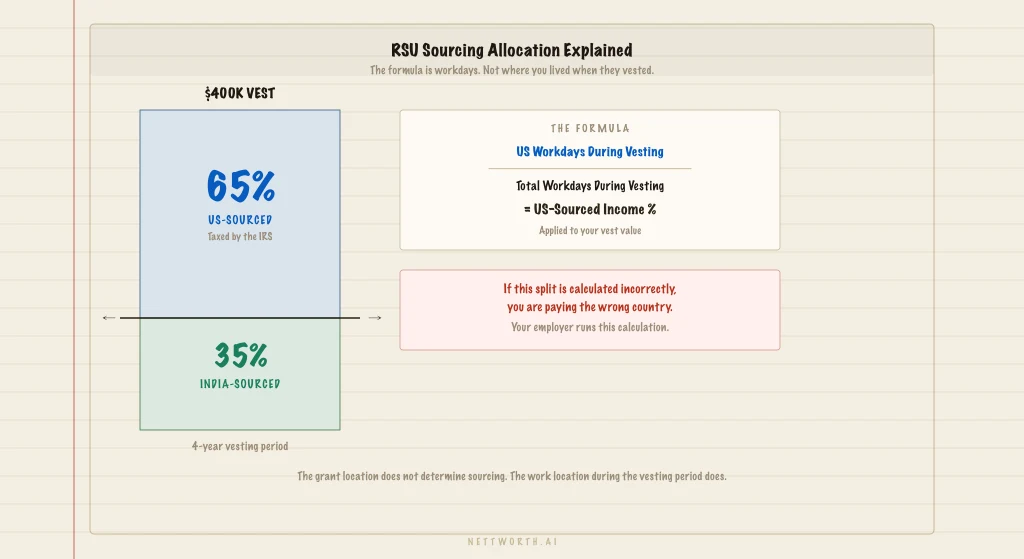

The allocation is proportional to workdays. If you worked in the US for 500 days during a 1,000-day vesting period, 50% of the RSU income at vest is US-sourced. If 800 of those 1,000 days were in the US, 80% is US-sourced.

What the sourcing determines: which country has primary taxing rights over that portion of your income. Your home country (or countries) applies its own sourcing rules, which may not be identical to the US approach. Where the two countries' calculations overlap, you face potential double taxation — resolved (where a tax treaty exists) through the treaty's competent authority provisions and the Foreign Tax Credit.

The Calculation

The formula is straightforward. For each RSU vest:

US-Sourced Percentage =

US Workdays During Vesting Period

÷ Total Workdays During Vesting Period

US-Sourced Income = Vest Value × US-Sourced Percentage

The vesting period runs from the grant date to the vest date for each tranche. If your RSUs vest in equal quarterly installments, each installment has its own vesting period — the grant date to that specific quarterly vest date.

A worked example

Grant date: January 15, 2023 (while working in Bangalore). Vest schedule: 25% per year, with the 4th tranche vesting January 15, 2027. Transfer to San Francisco: March 1, 2025.

For the January 2027 vest (4th tranche, vesting 4 years after grant):

Total vesting period: January 15, 2023 to January 15, 2027 = approximately 1,044 workdays. Bangalore workdays (Jan 2023 – Feb 2025): approximately 536 workdays. US workdays (Mar 2025 – Jan 2027): approximately 508 workdays.

US-sourced percentage for this tranche: 508 / 1,044 = 48.7%.

If the 4th tranche is 500 shares vesting at $90 per share ($45,000 total): US-sourced income is $21,915. India-sourced income is $23,085.

The US taxes $21,915 as ordinary income. India taxes $23,085 under its own rules (which may differ from the US computation). The double-taxation risk on the $21,915 depends on whether a US-India DTAA mechanism applies to your specific fact pattern.

Where Employers Get This Wrong

Employer payroll errors in RSU sourcing fall into two categories. Both are common. Both can create significant tax problems.

Error 1: Treating all vest income as current-country income

The most frequent error: your employer treats the RSU vest as entirely sourced to wherever you're currently located. If you're in Singapore at vest, they report the entire amount as Singapore-sourced. If you're in the US at vest, they withhold on the full amount as US income.

This gets the US-sourced income wrong in both directions. If you're in Singapore, the US is being under-reported — you'll owe US tax at filing that wasn't withheld. If you moved to the US from India and your employer sources 100% as US income, your India-sourced portion is being over-reported — you may be double-taxed unless you claim a treaty credit.

Error 2: Using the wrong vesting period dates

Some employers calculate the vesting period starting from the vest date and looking backward only to the most recent anniversary date, rather than back to the original grant date. This is especially common with ratable vesting schedules where payroll systems treat each installment as a stand-alone grant.

The correct calculation uses the original grant date as the start of the vesting period for each tranche. If your employer uses a different start date, the US-sourced percentage will be wrong.

How to Verify Your Employer's Calculation

You have the right to ask your employer's equity or payroll team for their sourcing calculation methodology. Specifically, ask for:

1. The grant date and vest date they're using for each tranche. Confirm the grant date matches your equity grant agreement, not the transfer date or hire date in the US.

2. The workday counts they're using. Ask whether they're using calendar days or workdays. The IRS's approach is workdays (excluding weekends and holidays). Some employers use calendar days, which produces slightly different results.

3. How they're handling partial years. If you transferred mid-year, ask how they determined your US start date and whether they're capturing a full count from that date.

Once you have their numbers, compare to your own reconstruction: pull your employment records, your I-94 entry dates, your pay stubs showing which country's payroll you were on, and build the workday count yourself. If the numbers diverge materially, you have a basis for requesting a corrected calculation before the W-2 is issued.

Performance-based RSUs

Performance RSUs (PRSUs) where the vest date is contingent on achieving milestones add a layer of complexity. When the performance milestone isn't known at grant, the IRS guidance suggests the sourcing period may be measured from grant to the date the performance condition is satisfied, or from the date the award is granted to the date it is reasonably certain to vest. The analysis is more fact-specific than time-based RSUs. If you have PRSUs and a cross-border employment history, a specialist needs to look at this — don't rely on standard payroll sourcing.

What This Means for Cross-Border Planning

Understanding your sourcing percentage matters most in three scenarios.

Scenario 1: You're about to transfer internationally

If you have a large unvested position and you're considering a move from the US to Singapore, UK, India, or any other country, calculate your current US-sourced percentage on each unvested tranche before you accept. The US portion is determined at vest regardless of where you live. If 80% of your vesting period has already been spent in the US, moving to Singapore doesn't reduce the US tax on future vests very much — 80 cents of every dollar of future vest income is still going to the US.

This calculation should inform the equity refresh negotiation. New grants made after you arrive in Singapore start the clock fresh — a new grant from Singapore Day 1 has a 0% US-sourced percentage that grows slowly over the vesting period. Asking for a larger cash component or new grants rather than an accelerated vest of existing grants is a rational response to this math.

Scenario 2: You've already transferred and your employer might be wrong

If you've been in your destination country for one or two vesting cycles and haven't reviewed the sourcing calculation, do it now. Compare your own workday reconstruction to what Box 1 of your W-2 shows. If there's a significant discrepancy, you either owe more than was withheld or less. Correcting a multi-year under-withholding is significantly more complicated than catching it at the first vest.

Scenario 3: You transferred TO the US from another country

This is Ananya's situation. If you were granted RSUs while employed outside the US and transferred to the US mid-vesting, the US sources only its own workdays. Your prior-country workdays are not US-sourced. This is a favorable fact pattern — the US is not taxing the entire vest, only its proportion.

The risk: your employer may withhold on the full vest as if it's entirely US income. If they do, you're over-withheld and will get a refund — but you need to file correctly to claim it. The refund isn't automatic. You need to calculate the correct US-sourced percentage and report only that amount on your US return, using Form 1116 for any foreign tax credit on the non-US portion if applicable.

The Core Point

RSU sourcing allocation is not a gray area or an advanced tax strategy. It's a mechanical calculation that determines which country has taxing rights over portions of your income. The calculation is knowable before you accept a relocation offer, before your first post-transfer vest, and before your employer files your W-2.

Most people don't run it because nobody in the chain tells them it exists. The equity platform sends a notification when shares vest. The employer withholds and reports. The CPA reports what the W-2 says. If the W-2 is wrong, the error propagates into the return unless you're looking for it.

Ananya's tax preparer ran the calculation because Ananya asked why her Box 1 number didn't match what she'd expected. That question is worth asking.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

Leaving the US for Singapore With RSUs: Why 'No Tax Treaty' Is the Detail Everyone Misses

Alex said yes to the Singapore offer on a Tuesday. Six months in, a W-2 arrived showing $200K in income he didn't understand. His employer had sourced the RSU vesting period correctly — US workdays divided by total vesting days. The US taxes that portion regardless of where you live at vest. Singapore has no income tax treaty with the US. There is no protective mechanism.

Before You Move to the US from Europe: The Financial Checklist for German, Dutch, and French Professionals

Thomas had been contributing to his German bAV for nine years. His cross-border accountant explained: Germany's pension tax deferral is a German decision. The US didn't agree to it. His employer's contributions were still taxable US income in the year contributed. Three countries, one checklist.

NRE and NRO Accounts: What Changes the Day You Become a US Tax Resident

NRE interest is tax-free in India. The day you become a US tax resident, it becomes US taxable income at ordinary rates — and most NRIs find out two or three years late. NRO interest has a different problem: 30% TDS generates a Foreign Tax Credit, but the credit math depends on your US bracket. FBAR applies to both accounts from year one. The gap exists because the Indian CA says 'tax-free' and the US CPA never asks.