Should I Pay Off My Mortgage With an Inheritance?

You have $400,000 left on your mortgage at 6.75%. You just inherited $3M. The math seems obvious. But you've been sitting on this decision for four months, and something keeps stopping you.

That hesitation is not irrational. It's information.

The question "should I pay off my mortgage with my inheritance" is one of the most common searches that brings people to financial content after inheriting money. The reason it is common is that the answer is not obvious, even though it appears mathematical.

There is a mathematical case. There is a psychological case. And there is a third option most people don't consider. Let's walk through all three.

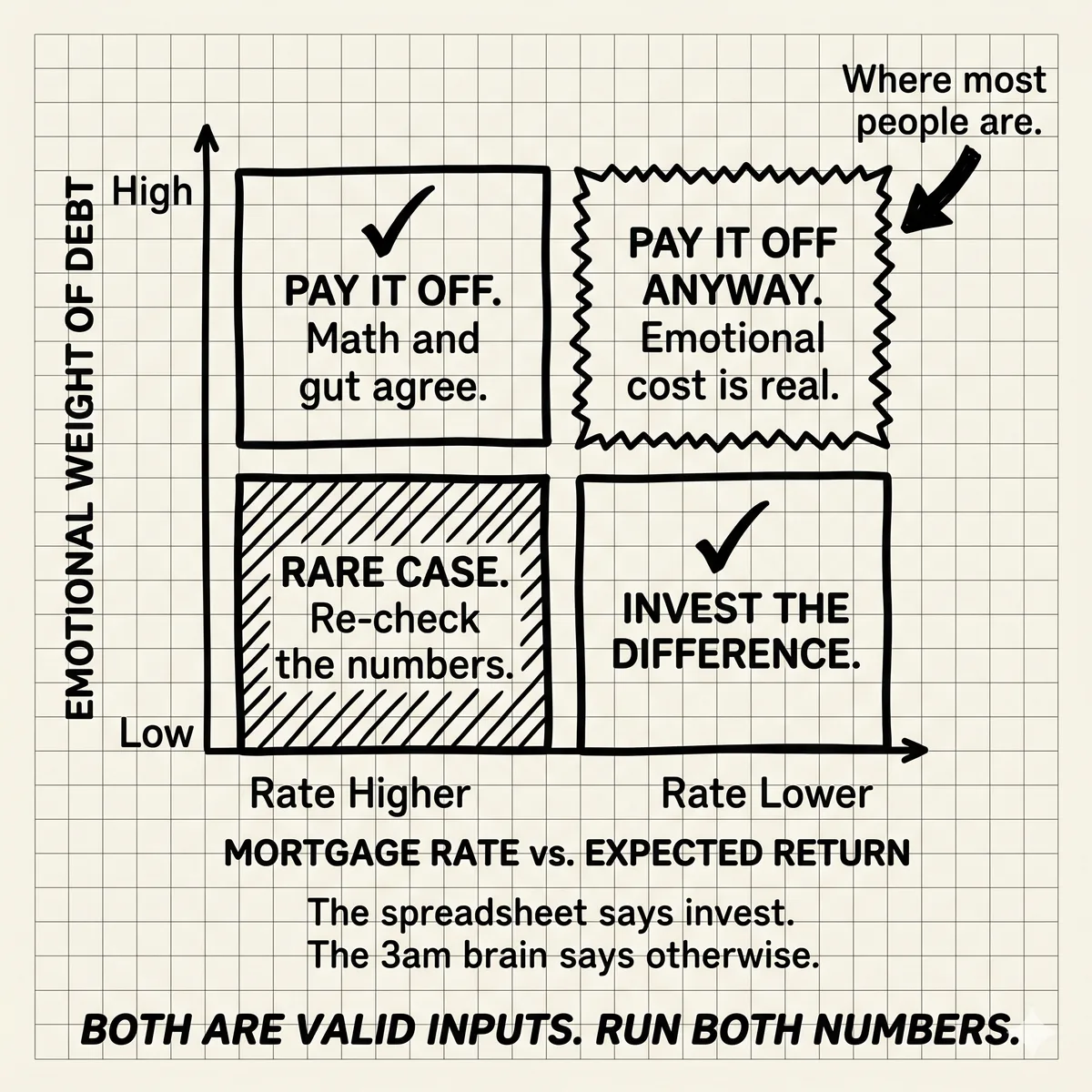

The Mathematical Case

If your mortgage rate is 6.75%, paying it off is a guaranteed 6.75% after-tax return. No volatility. No sequence-of-returns risk. No market timing. Every dollar you put toward the mortgage saves you 6.75 cents per year in perpetuity.

The question is what you would do with the money instead. If the alternative is a money market fund at 4.8%, paying off the mortgage is mathematically superior by nearly 2 percentage points. On $400,000, that is $7,800 per year in the math column.

If the alternative is a diversified stock portfolio expecting 7-10% average annual returns over the long run, the math flips. Historically, a broad stock index has returned around 7% after inflation over long periods. A 6.75% mortgage rate is below that expected return. In a pure expected-value calculation, keeping the mortgage and investing produces more wealth over 20 years.

But expected value is not the same as guaranteed value. The stock market's 7% historical average includes years of -30%. Your mortgage rate is 6.75% every month, without exception. You are comparing a certain cost to an uncertain return, and that comparison is not as simple as subtracting the numbers.

The tax dimension

If you itemize deductions and deduct mortgage interest, the after-tax cost of your mortgage is lower than 6.75%. At a 32% federal marginal rate, a 6.75% mortgage costs roughly 4.6% after deducting interest. That changes the math meaningfully.

But if you're in the situation where your inheritance generates new income (dividends, interest), your marginal rate in the year you inherited may be unusual. And the standard deduction ($29,200 for married filing jointly in 2026) means many people don't itemize anyway, which means the mortgage interest deduction is already worth zero to you.

Ask your CPA: "Am I currently itemizing, and if so, what is the actual after-tax cost of my mortgage?" That one question gives you the real number to use.

The Psychological Case

The spreadsheet doesn't capture what it feels like to not have a mortgage payment.

For many people, the monthly mortgage payment is the primary source of financial anxiety. It is the number that defines what "can't lose the house" means. Eliminating it changes the baseline of your life. You need less income to feel secure. You have more flexibility in your career. You have more room in a down market to ride out a bad year without fear.

This psychological benefit is real. It does not appear on a spreadsheet. Financial theory sometimes dismisses it as "irrational." This is a mistake. Security has value. The specific value is different for every person. Some people genuinely don't lose sleep over debt. For others, the no-mortgage life is worth a few percentage points of expected return.

Ask yourself honestly: if you paid off the mortgage tomorrow, would you feel materially better? Would you carry yourself differently? Would you make different career decisions from a place of security rather than necessity?

If yes, that is a real return. Price it accordingly.

There is also a grief dimension that doesn't show up in the financial literature. Some people describe paying off the house with an inherited parent's money as a meaningful act. Not wasteful. Not irrational. An act of honoring. "Dad's money bought the house we didn't have to worry about anymore." That is not nothing. It is a legitimate reason to make the choice.

The Third Option: Partial Paydown

Most of the discussion around this question assumes a binary choice: pay it off or don't. There is a third option that most people don't consider.

You can make a large additional principal payment that reduces your balance significantly without eliminating the mortgage entirely. If you have $400,000 left and you put $200,000 toward principal, you now have a $200,000 mortgage. Your required monthly payment drops. Your amortization schedule shortens. Your guaranteed return on that $200,000 is exactly your mortgage rate.

This matters for a few reasons:

- Liquidity. Once you put money into a house through mortgage payoff, you can only get it back by selling or refinancing. A partial paydown retains more flexibility. The remaining balance can be managed over time.

- Psychological relief at lower cost. For many people, getting the mortgage below a certain threshold (say, below $200K or below what feels manageable) delivers most of the psychological benefit of full payoff without locking up all the liquidity.

- Staging. You can pay down $200K now, invest the rest, and reassess in two years. The full payoff option doesn't go away. The investment opportunity also doesn't go away. You're not choosing once forever.

The partial paydown option is underrated in the financial advice literature because it doesn't fit a clean narrative. It's not "be debt-free" and it's not "invest everything." But for people who are genuinely uncertain, it often fits better than either extreme.

Questions to Ask Yourself Before Deciding

- What is my actual mortgage rate? Not the APR. The interest rate. And am I currently itemizing to deduct it?

- What is my investment horizon? The expected return advantage of investing over paying off debt compounds over time. If you need the money in 5 years, the math is different than if you won't touch it for 25.

- How do I actually feel about carrying debt? Not how you think you should feel. How you actually feel, at 2am when you can't sleep.

- What is my current income situation? If you have stable high income with good career security, you can absorb the debt comfortably. If your income is variable or you're considering a career change, the monthly mortgage payment has higher risk.

- Have I fully funded tax-advantaged accounts first? If you have the option to max a 401(k), Roth IRA, or HSA, those should generally come before paying off a sub-7% mortgage. The tax advantage on those accounts changes the math.

- Is this the house I'm staying in? If you're planning to move in 5 years, paying off a mortgage you'll sell anyway has lower value. You'll get the equity back at sale regardless.

The Answer That Isn't Universal

There is no rule that covers everyone. At 6.75%, the mortgage is expensive enough that paying it off is a reasonable choice even on pure expected value. At 3.5% (common for mortgages originated in 2020-2021), the math strongly favors investing. At 6.75%, it's genuinely close.

The people who regret paying off the mortgage are usually those who did it because an advisor told them to, without thinking through what they actually wanted. The people who regret not paying it off are those who watched their portfolio drop 30% in 2022 while their mortgage continued to compound.

This is one of those decisions where getting the psychology right matters as much as the math. Run the numbers. Be honest about what the numbers mean to you. And remember that you can always invest more money next year. You cannot get back the principal you put into a house without selling it or refinancing.

The third option (partial paydown) is on the table. Most people asking this question should at least run the numbers on it before choosing between the two extremes.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

How to Actually Invest an Inheritance (Without a Finance Degree)

Low-cost index funds outperform most actively managed alternatives over any 15-year period. The three-fund portfolio and target-date funds are not cop-outs — they are the approach most economists would actually use. Here's the jargon-free version.

Geography Arbitrage

Elon's leaving California. Bezos to Miami. Headlines in Jan 2026 miss the real story—which was decided 18 months ago.

Concentrated Tech Equity: The Diversification Decision (With Math)

Your advisor says diversify. But diversification has a real cost. Here is the math on when holding wins, when selling wins, and what wealthy founders actually do.