Smart Debt at Scale

When you own $3M in paid-off assets, borrowing at 2.8% beats liquidating appreciated stock. Here's the math that changes the conversation about debt.

The email hit my inbox at 4:47pm.

Rate sheet from the private lender. I read the number. Read it again. Then called my wife immediately because my brain needed verification that I wasn't misreading the zero.

2.8%.

On a $2.1M portfolio-backed loan.

In a market where the Fed funds rate is sitting above 4%, where conventional mortgages are pushing 6.5%, where margin loans top out around 8%. I'm staring at a loan on my balance sheet that costs less than inflation.

The rental property—that $3M house we'd paid off in full back in 2015—finally had a purpose beyond Airbnb bookings and tax depreciation.

But here's where my lizard brain started screaming.

I've spent fifteen years building the mental architecture that debt is what happens to people who can't make it work. Debt is failure. Debt is other people's problem. I paid off this rental property specifically to never owe anything on real estate again. That was the goal. That was the win.

Now I'm sitting with a rate sheet that says: use the equity. Borrow $2.1M at 2.8%. Redeploy cash into the portfolio. Let the mathematics speak.

And the mathematics were loud.

The Math That Changes Your Mind

Here's the actual scenario staring me down.

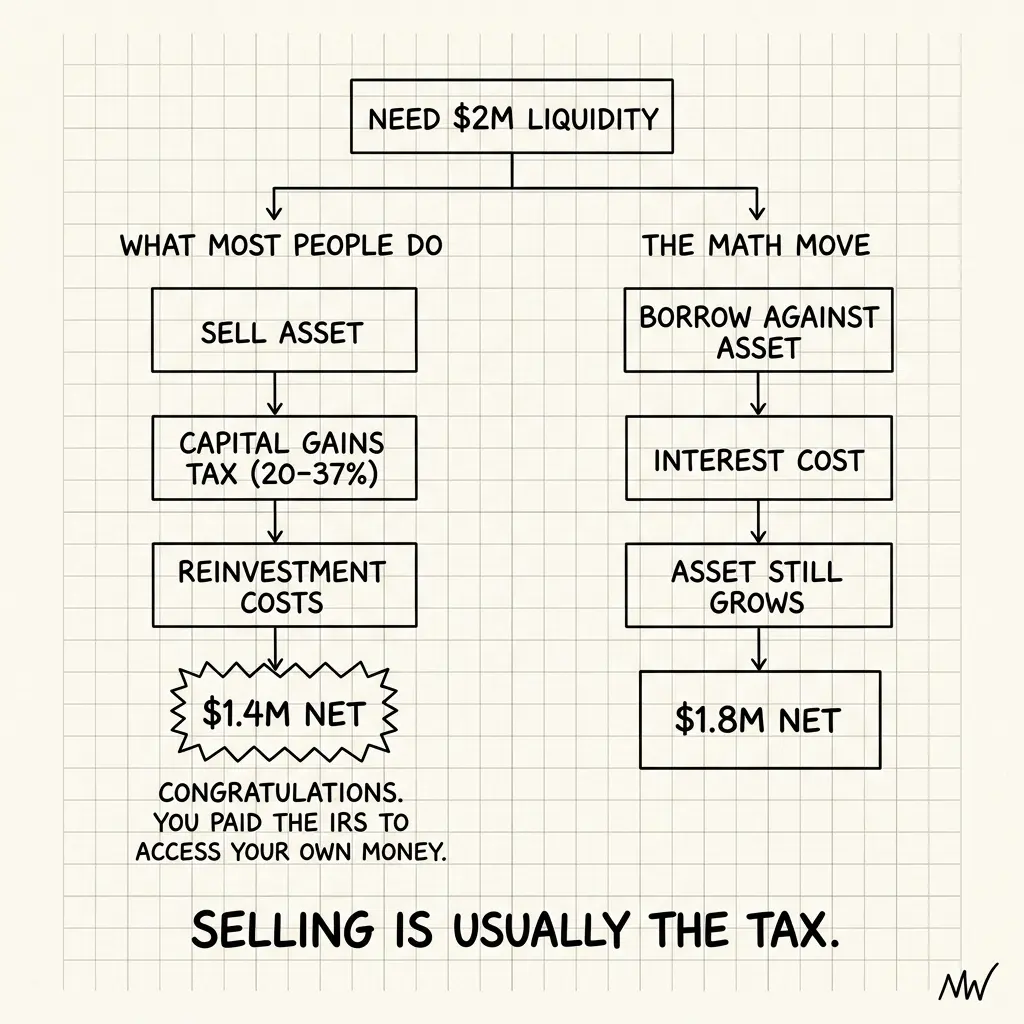

I could liquidate $2.1M of appreciated stock to fund a strategic acquisition—something I'd been sitting on for six months because liquidating felt like wrong for tax reasons. Long-term capital gains tax on $2.1M of gains? Figure 25-28% in combined federal and California rates depending on bracket. That's $525K-$588K in taxes just to move the money.

I'd also lose the future appreciation on that stock. That $2.1M of appreciation isn't static—it's growing. Even at a 7% annualized return, that's $147K a year in growth I'd sacrifice by selling. Over five years, that's $735K in foregone gains.

Or I could take the 2.8% loan, keep the stock (and all its future appreciation), and pay $58,800 a year in interest on the borrowed capital.

The math isn't even close.

$525K in taxes plus $735K in foregone growth plus ongoing opportunity cost. That's—conservatively—over $1.2M in total cost to liquidate.

Versus $58,800 a year in interest that I can deduct, that costs me money I'm earning, and that lets me keep a $2.1M equity position that's doing its job.

This is where the belief started to crack.

Debt isn't bad. Debt is a tool that's only dangerous when you're using it wrong. When you're borrowing to spend, when you're borrowing on unsecured credit, when you don't have a margin of safety—that's dangerous. That's the debt that kills balance sheets.

But debt when you have a $3M paid-off asset backing it? Debt at 2.8%? Debt that lets you keep $2.1M of appreciating assets while you deploy cash into something that'll compound?

That's not failure. That's not a problem.

That's leverage.

And leverage—real leverage, backed by real assets, at rates that make the math work—is how balance sheets actually expand.

How Asset-Backed Mortgages Work

The mechanism is simpler than most people think.

When you have substantial assets (paid-off real estate, concentrated stock positions, investment portfolios), lenders will lend against those assets at rates better than traditional mortgages. Why? Because they have a clear collateral position. They're not betting on your credit score—they're betting on your assets.

Asset-based mortgages typically work like this:

You pledge $3M in equity (from a paid-off property). The lender lends you 70% of that value at a negotiated rate. You get $2.1M in cash. You keep the collateral. The lender has a mortgage against it.

The magic:

You get institutional-grade rates (2.8%-4.0% depending on market and creditworthiness) without selling a single asset. You keep the tax benefits of ownership. You keep the appreciation. And you have access to capital to deploy into whatever comes next.

The cost is simple: interest only, no amortization required, with the principal due at maturity (typically 5-10 years). You're paying for the use of money, not for a declining principal balance.

Margin loans work differently.

You pledge your portfolio as collateral and borrow against it at call-loan rates (typically prime + 0.5%-1.0%, so ~5.5%-6.5% in current markets). Lower rates than asset-based mortgages, but with a catch: they're callable. If your portfolio drops 20%, the lender can demand repayment. That's the risk.

HELOCs sit in between.

You pledge your primary residence, get a line of credit, and draw when you need it. Rates are typically 1-3% above prime (so 5.5%-7.5% currently). The advantage: flexibility and no upfront capital requirement. The disadvantage: callable if home values drop significantly.

For me, the asset-backed mortgage was the right tool because:

- I had substantial equity in a paid-off property

- I wanted a fixed rate (not callable)

- I didn't need the full $2.1M immediately (so HELOC's flexibility didn't matter)

- I had a specific deployment plan that would generate returns above the cost of capital

The Belief Flip

Old belief: "Debt = failure. Paid-off assets = victory."

New belief: "Debt is a tool. Using your balance sheet is how you expand it."

This isn't credit card debt. This isn't borrowing to spend on a vacation or a new car. This isn't leverage that amplifies your personal spending habits.

This is using one part of your balance sheet (your real estate equity) to deploy capital into another part (your investment portfolio or a strategic acquisition) at a rate that's mathematically advantageous.

The prerequisite: You need assets. Real assets. Paid-off property, concentrated stock, investment portfolios. You need the collateral equation to work.

But if you've spent ten years accumulating—if you've got $3M in paid-off property sitting there—you're probably leaving opportunity on the table by being afraid of debt.

When This Works (And When It Doesn't)

This strategy works when:

- You have substantial equity in assets you don't want to liquidate

- You have a specific deployment plan (acquisition, portfolio rebalancing, business investment)

- The math works: your cost of capital is lower than your expected return

- You have income stability to weather rate changes or portfolio volatility

- You can handle optionality risk—the rate or terms could change before you're done using the capital

This strategy doesn't work when:

- You're borrowing to spend (vacations, lifestyle)

- You're leveraging into volatile assets (concentrated stock positions you're uncertain about)

- Your income is unstable

- You're borrowing because you need the cash (that's a different problem—that's a liquidity issue, not a leverage opportunity)

- You have existing debt that's already dragging on your finances

For most HENRYs, the constraint isn't asset base—it's deployment plan. You have the collateral. You just don't have a clear answer to "what am I actually going to do with $2.1M?"

That answer has to come first. The leverage is the tool, not the goal.

The Real Question

What leverage is sitting in your balance sheet right now?

If you've got $5M in net worth—$2M in paid-off real estate, $2M in appreciated stock, $1M in liquid investments—you're probably leaving $2M-$5M in deployment capacity on the table.

That $2M in paid-off property could be generating $1.4M-$2M in capital at 2.8%-4.0% rates. That capital could go into:

- Acquiring another property (diversify your real estate)

- Rebalancing concentrated stock (reduce your single-company risk)

- A strategic business investment (your side project that needs capital)

- A portfolio acquisition (if you're evaluating businesses to buy)

The cost of that capital? Lower than the cost of liquidating appreciated stock. Lower than the opportunity cost of staying fully invested in single-name risk.

But here's the hard part: you have to believe that debt—strategic debt, backed by collateral, at rates that make mathematical sense—isn't failure.

It's just math.

And if you've spent fifteen years believing paid-off property = victory, it takes a rate sheet at 2.8% to prove you wrong.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

H1B Homebuying: The 20-Year Math Nobody Runs

Visa uncertainty breaks conventional homebuying logic at year 5-7, not month 1. Nobody models the full timeline with immigration risk factored in — here's the math.

Concentrated Tech Equity: The Diversification Decision (With Math)

Your advisor says diversify. But diversification has a real cost. Here is the math on when holding wins, when selling wins, and what wealthy founders actually do.

How to Actually Invest an Inheritance (Without a Finance Degree)

Low-cost index funds outperform most actively managed alternatives over any 15-year period. The three-fund portfolio and target-date funds are not cop-outs — they are the approach most economists would actually use. Here's the jargon-free version.