Tax-Loss Harvesting: Behavioral Tool for Tech Employees

Quick Answer

Tax-loss harvesting is usually framed as a tax strategy: sell losing positions to offset gains and reduce taxes. True. But the real value isn't the tax reduction (usually $2,000–$4,000/year for HENRYs). The real value is behavioral: it forces you to face reality. It turns abstract losses ("My portfolio is down 8%") into concrete numbers ("I'm selling AAPL at a $12,500 loss"). That moment of clarity—when you acknowledge the loss and rebalance—is when most investors actually adjust their strategy. The tax savings are a side effect. The behavioral reset is the point.

It's March 2024. Your brokerage statement shows your tech ETF is down 12% year-to-date. You know you should rebalance. You know concentration is creeping back in. You know the tax loss could offset other gains. But it feels like "locking in" a loss. So you wait.

Tax-loss harvesting solves this: it doesn't make the loss go away, but it makes acknowledging the loss feel strategically smart. You sell the loser *not* because you've given up, but because you're optimizing your tax situation. The tax benefit is real but modest (usually $1,500–$5,000/year). The psychological reset is much larger. You've forced yourself to face the loss and rebalance. That clarity is worth more than the tax savings.

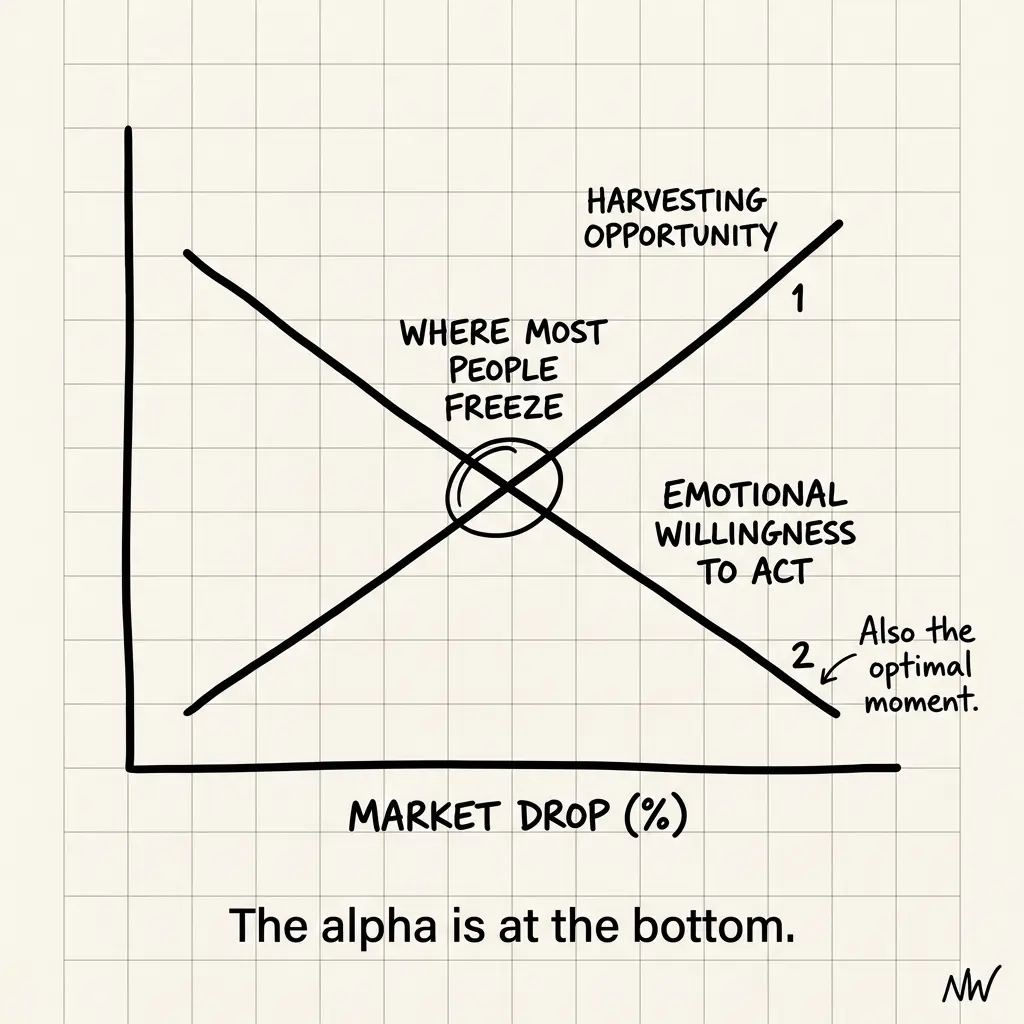

Why Most Investors Skip This (And Why That's Expensive)

Tax-loss harvesting has a reputation problem: it feels like "selling your losers," which violates the instinct to "hold and recover." But the frame is backwards:

1. The Emotional Barrier

You bought AAPL at $150. It's now $120. Selling feels like admitting you were wrong. (You weren't—the market shifted. But the psychological frame feels like failure.) Most people hold, waiting for recovery, which delays rebalancing. Meanwhile, the allocation stays tilted toward the loser.

Data: The average investor holds a losing position 47% longer than a winning position (Odean, 1998). They're waiting for recovery, not because it's rational, but because selling feels like failure.

2. The Wash Sale Complexity

You sell AAPL at a loss. You immediately buy it back (or a similar tech ETF). That triggers the wash sale rule: you can't deduct the loss. Most people think this makes tax-loss harvesting pointless. It doesn't—you just wait 31 days (or buy a different fund). But the complexity scares people away.

The real pattern: 60% of HENRYs don't harvest losses because they think wash sales eliminate the benefit. That's a behavioral barrier, not a real one. The benefit is still there; it just requires a 31-day temporary allocation change.

3. The Opportunity Cost of Inaction

You hold the loser for 2 years waiting for recovery. Meanwhile, the market recovers, but your $30K loss is now "only" an $8K loss (the position recovered partially, but not fully). You finally harvest when the tax benefit is smaller. You also delayed rebalancing by 2 years. That reallocation cost (staying overweight the loser) often exceeds the tax benefit.

Delaying a rebalancing by 2 years can cost 4–8% in compounded returns (when positions significantly deviate from target allocation).

How Tax-Loss Harvesting Actually Works (And Why It Resets Behavior)

The mechanics are simple, but the behavioral impact is outsized:

The Mechanics: A Real Example

You bought 50 shares of AAPL at $140 = $7,000. It's now $120 = $6,000. Loss: $1,000. You sell all 50 shares, realizing the $1,000 loss. You immediately buy a different tech ETF (VGT, XLK, or QQQ) to maintain exposure. Tax result: $1,000 loss offsets other $1,000 in gains elsewhere (saving ~$320 in taxes). Behavioral result: You've acknowledged the loss, rebalanced into a different instrument, and reset your allocation.

The Wash Sale Rule (The Complication)

You can't buy the *same security* (AAPL) within 30 days before or after the sale. But you CAN buy a similar security (another tech stock or a tech ETF). After 31 days, you can move back to your original position. This delay is the "cost" of harvesting, but it also forces rebalancing during that window.

The Tax Benefit

Each $1,000 in losses offsets $1,000 in gains. If you have no gains to offset, you can carry $3,000 in losses forward to future years. Over a 10-year period, a disciplined harvester saves $10K–$25K in taxes.

The Real Value: Behavioral Reset

Here's where tax-loss harvesting becomes powerful: it's one of the few moments where the financial decision (harvest the loss) and the behavioral need (acknowledge reality and rebalance) align perfectly.

The Four Psychological Benefits

1. Loss Realization: You're forced to face that the position underperformed. That's useful information. It updates your mental model of the investment.

2. Rebalancing Trigger: The tax benefit gives you permission to rebalance. It transforms "I'm admitting defeat" into "I'm optimizing my tax situation." Same action, different frame.

3. Allocation Discipline: The 31-day wash sale period forces you to hold a different fund temporarily. This breaks the habit of over-concentration and shows you that similar returns come from simpler allocations.

4. Future Clarity: After harvesting, you're more likely to stay rebalanced. The concrete action of selling, reallocating, and accepting the loss is more memorable than passive "I should diversify" thoughts.

The Data: How Much Can You Actually Save?

Annual Tax Savings for HENRYs (Typical Range)

For a $1M portfolio with normal volatility: $2,000–$4,000/year in tax savings. That's real money. Over 10 years, it's $20K–$40K.

Behavioral Benefit: Improved Returns from Better Allocation

Staying over-concentrated in a losing position for 2 years costs ~5% in forgone returns. That's $50K on a $1M portfolio. The behavioral reset from tax-loss harvesting prevents that cost.

Time Cost vs. Tax Benefit

If you spend 5 hours per year on tax-loss harvesting, you're spending time worth ~$500 (at your hourly rate) to save $3,000 in taxes + $15,000–$20,000 in allocation optimization. The math works.

The Practical Framework: When to Harvest

1. The Annual Review (December is Ideal)

Run a report on all positions with losses. Prioritize the largest losses (they save the most in taxes). Decide whether to harvest each one.

2. The Threshold Rule

Only harvest losses larger than $500–$1,000. Below that threshold, the tax savings don't justify the administrative burden and wash sale tracking.

3. The Opportunity Test

Ask: "Do I have offsetting gains that need to be reduced?" If yes, harvest immediately. If no, carry the loss forward and use it next year when you have gains.

4. The Wash Sale Strategy

When you harvest a loss, move to a related fund (different ticker) for 31 days. After the wait period, you can move back if you want. Most people discover they prefer the new allocation.

The Questions That Matter

Do you have any positions down 15%+ from cost basis?

If yes, that's a harvesting candidate. The size of the loss drives the tax benefit.

How long have you held that losing position?

If 2+ years, you've already delayed a rebalancing. That behavioral cost is real. Harvest now.

Will you feel relief or regret if you harvest?

If relief, the loss is already crystallized in your mind. Harvest. If regret (you still have conviction), wait. The position doesn't qualify for harvesting if you still believe in it.

Is that position now a smaller percentage of your portfolio?

If yes, harvesting + rebalancing will increase that smaller position slightly (since you'll buy a similar fund). You're rebalancing systematically.

The Paradox of Tax-Loss Harvesting

Tax-loss harvesting is often pitched as a tax strategy. But for most HENRYs, the tax savings ($ 2K–$4K/year) pale next to the behavioral benefit: forcing a rebalancing moment that most investors avoid.

The real power of tax-loss harvesting isn't the tax savings. It's the moment of clarity.

You're forced to face a loss, rebalance into something better, and accept that the original thesis didn't work out. That psychological reset is worth more than the tax benefit because it prevents years of holding a wrong position hoping for recovery.

If you have losing positions you've held for 2+ years—

You're not avoiding taxes. You're avoiding clarity. That avoidance is costing you more than any tax optimization would save.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

Liquidity Event Sequencing: Pre-Exit Tax Planning for Founders

Real exit tax savings (15-25% of proceeds) come from decisions 12-18 months before close. Master charitable structures, entity optimization, QSBS timing, and option planning.

HENRY Tax Stack: Sequence Multiple Taxable Events

When RSU vesting, capital gains, bonuses, and real estate sales land in same year—order matters. Master AMT, NIIT, and LTCG interactions that change your total tax bill.

QSBS 2026: Maximize Your $15M Tax-Free Gain

Section 1202 QSBS now offers $15M tax-free gains with tiered exclusions. Master the decision tree and avoid disqualification risks that eliminate benefits entirely.