180-Day Window: Critical Steps After Liquidity Event

Quick Answer

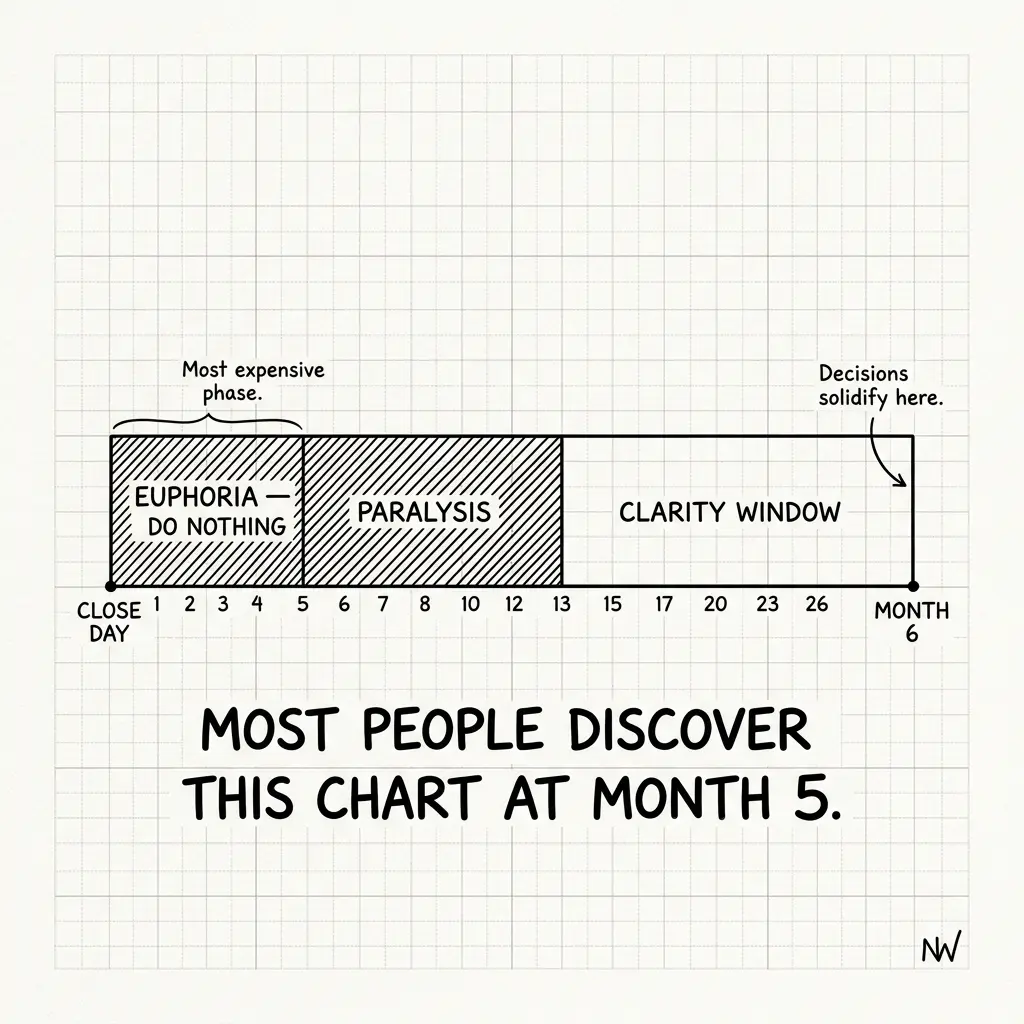

The 180 days after a liquidity event (exit, IPO, secondary sale) are the most critical and least planned. You get an offer → you accept → you sign → there's a lock-up period → then silence. In that silence, most founders make expensive mistakes: over-concentrated holdings they later regret, tax decisions that trigger audits, lifestyle commitments that lock them in, or estate planning failures that could cost millions if something happens. The window where you *can* make changes without massive tax consequences is shorter than you think. Here's what actually happens in those 180 days.

Day 1 after close: He has more money than he expected to have. Day 180 after close: He understands what he did wrong.

His biotech company sold to a larger pharma outfit. Not a mega-exit, but substantial: $420M acquisition price. He'd been co-founder and CTO. His ownership was 3.2%, which meant roughly $13.4M to him, pre-tax.

The acquisition closed on a Tuesday. He had a wire into his account by Thursday.

On Friday, he got drunk and bought a Range Rover. Not because he needed a car. Because he could now afford to.

That Range Rover was the first of a cascade of decisions, each one made in the disorientation of sudden wealth, each one with consequences that wouldn't become clear for months.

The 180-day window is when you make irreversible decisions while emotionally unmoored.

Week 1: The Euphoria Phase

Days 1–7: Disorientation

He tells people: "I'm rich." It doesn't feel real. His checking account says $13.4M. But it doesn't *feel* like $13.4M. It feels like the same thing, but with bigger numbers.

The brain doesn't process sudden wealth well. Studies on lottery winners show decision-making gets *worse*, not better, in the first weeks after a major financial event. Your judgment is compromised by disorientation.

Mistake #1: Range Rover ($180K). Paid cash. No financing benefit. Impulse.

Mistake #2: Called his brother. "I want to help you." Committed to paying off his brother's house mortgage: $480K. No structure. No gift tax analysis. Just emotion.

Weeks 2–4: The Planning Phase (Where Mistakes Deepen)

Days 8–28: Action Without Framework

Now he's calling advisors. "I need to do something with this money." But his brain is still in exit mode. He's not thinking clearly.

His financial advisor suggests: "Let's diversify." He's been concentrated in his company stock for 10 years. That concentration was fine when he was illiquid (couldn't sell). Now he's liquid and wants to feel smart about the diversification decision.

He tells his advisor: "I'm holding $7M in stock. I want to move to a diversified portfolio. Let's do it over six months." His advisor says, "That's smart. Tax-loss harvesting opportunity too—we can offset some of your cost basis."

Mistake #3: Didn't ask about QSBS. The biotech stock qualifies under Section 1202. Holding for five years (from his purchase date) means $7M in tax-free gains (subject to the new $15M cap). But his advisor didn't mention it. He's liquidating too early, triggering capital gains that could have been tax-free.

Mistake #4: Didn't ask about lock-up periods and restricted shares. Some of his $13.4M is still subject to lock-up (6 months post-close). The rest is liquid. He should be sequencing the diversification around lock-up expiries. Instead, he's selling the liquid shares and holding the restricted ones (which seems logical but is tax-inefficient).

By Week 4, he's committed to selling $4M of biotech stock over six months. That will trigger $2.8M in capital gains (cost basis was $1.2M). At a 37% marginal rate (federal + state), that's $1.04M in taxes.

He hasn't thought about whether he should have held for QSBS relief. Nobody mentioned it.

Weeks 5–12: The Lifestyle Lock-In Phase

Days 29–84: Irreversible Commitments

Week 5: His wife finds a house. $4.2M. It's beautiful. It has everything they discussed: the backyard for the kids, the view, the room for his parents to visit. He puts down 20% ($840K) and closes by Week 7.

Now he has a $3.36M mortgage. The payment is $18K/month. With the property taxes in California, the all-in housing cost is $28K/month.

That's $336K/year in housing costs on a $13.4M net worth (2.5% of wealth on housing). It seems reasonable. But it's also locked him in.

Mistake #5: The house was bought with emotion, not strategy. If he'd held off six months, he would have realized: the $13.4M is pre-tax. After capital gains taxes on the stock sale, estate taxes later, and the cost of liquidity management, his actual spendable wealth is closer to $8M. A $4.2M house on an $8M sustainable wealth base is aggressive.

Week 8: His kids' school calls. Tuition is $45K/year per child (he has two). That's $90K/year recurring, for 10 years.

Week 10: His parents mention they're worried about retirement. He says, "Don't worry. I'll help." Commits to $5K/month for them. Another recurring commitment.

By Week 12, he's committed to:

- $336K/year in housing

- $90K/year in school tuition

- $60K/year in parental support

- Lifestyle inflation: additional $150K/year (higher quality of everything)

- Total recurring commitments: $636K/year

That's 4.7% of pre-tax wealth burning annually, just to maintain the lifestyle he's now locked into.

Weeks 13–24: The Estate Planning Failure

Days 85–168: The Document Problem

His estate plan was last updated when he had $500K net worth. A simple will. Beneficiaries listed as "my spouse and children, in equal shares."

Nobody has told him: He needs to update that will. He needs a trust. He needs to think about how the $13.4M transfers to his kids (directly? In trust? Over time?). He needs to think about estate taxes (his net worth is now high enough that every dollar matters).

Week 16: His buddy (from another startup) mentions casually: "Have you updated your estate plan?" He hasn't. He calls an estate attorney. The attorney says, "Let's start with a meeting. Fee is $5K just to assess."

He's annoyed at the fee and delays.

What he doesn't know: If something happens to him in the next month (before he updates his estate plan), his $13.4M passes through probate under his old will, subject to full estate taxes, with no structure to protect the wealth or ensure it goes where he wants.

The cost of delaying estate planning: If he dies in the next 90 days, his estate loses roughly 20–40% to taxes and legal fees ($2.7M–$5.4M). That's the cost of three months of inaction.

Week 25+: The Reckoning

By Day 180 (six months), he has:

- Spent $660K on impulsive/lifestyle commitments (Range Rover, brother's house, moving costs, home furnishings)

- Committed to $636K/year in recurring expenses that reduce flexibility

- Triggered $1.04M in unnecessary capital gains taxes (by not holding for QSBS)

- Failed to update estate plan (exposing $13.4M to probate and estate taxes if something happens)

- Not thought about charitable giving structure (could save $400K+ over lifetime with a DAF)

Total impact of the 180 days: $1.7M in avoidable costs + constraints. That's 12.7% of his wealth, burned through disorientation and lack of planning.

What Most People Get Wrong

People think the 180-day window is about "letting emotions settle." Take time. Don't make rash decisions. Let the dust settle.

The actual problem is more subtle: The 180-day window is when *irreversible decisions* get made. Some decisions (like tax planning) have a short shelf life. Miss the window, and you've locked yourself out of strategies that would have been available if you'd planned. Other decisions (like housing and lifestyle) lock you in for years. Make them in the emotional high of the exit, and you've committed to a financial structure based on feeling, not thinking.

The 180-Day Stack: What Should Actually Happen

Here's the sequence that prevents the $1.7M in mistakes:

Days 1–14: The Pause

Don't make any financial decisions. Let the wire clear. Understand what you actually have. Let the emotional high pass.

Action: Put the money in a high-yield savings account. Do nothing else.

Days 15–45: Advisors (Tax, Legal, Financial)

Simultaneously (in parallel, not sequence): (a) Meet with a tax advisor who knows section 1202 QSBS rules. (b) Meet with an estate attorney. (c) Meet with a wealth advisor.

These aren't independent decisions. They inform each other. The tax conversation affects the diversification strategy. The estate conversation affects the structure. The wealth conversation affects both.

Action: Get specific, quantified advice on: (i) QSBS holding periods and tax consequences, (ii) estate plan structure, (iii) diversification sequencing, (iv) recurring expense budgeting.

Days 46–90: The Plan, Not the Execution

Based on advisor feedback, build a 12-month financial plan: Which assets diversify first (taxable account)? Which hold? When do lock-ups expire? When do stock sales happen? How is the diversification phased to minimize taxes?

Action: Approved estate plan. Approved tax plan. Approved diversification sequence. Everything documented. Nothing executed yet (except estate plan).

Days 91–180: Lifestyle Decisions With Constraints

Now that you know your sustainable spendable wealth ($8M, not $13.4M), make housing and lifestyle decisions within that constraint. The house, the school, the family support—budget them against what's actually sustainable.

Action: Execute estate plan. Begin tax-optimized diversification (not all at once; per the plan). Commit to recurring expenses only after calculating what's sustainable.

The Questions That Matter

If you're approaching a liquidity event, have you pre-planned the first 90 days?

Not vaguely. Specifically. Who will you call? In what order? What questions will you ask each of them? Do they know the timeline?

Does anyone in your circle own the "don't let him make rash decisions" job?

A spouse, a close friend, an advisor—someone whose job is to slow you down during the emotional high. Someone who can say, "Wait. Let's think about this." Without that person, you'll buy the Range Rover.

What recurring commitments (housing, school, family support) are you considering?

Calculate them as a percentage of sustainable wealth (not gross wealth). If they total more than 3–4%, they'll constrain your optionality for years.

Does your current estate plan match your new net worth?

If the answer is "I don't know," update it in the first 60 days. The cost of updating is $3K–$10K. The cost of not updating (if something happens) is $2M–$5M.

The Real Window

The 180-day window isn't a celebration period. It's a planning period disguised as one.

The emotions are there: excitement, validation, relief. Those are real and deserve acknowledgment. But underneath the euphoria, you're making decisions that will constrain the next 20 years of your financial life.

The difference between founder who thrives after an exit and one who struggles is rarely luck. It's usually whether they slowed down enough in the first 180 days to make intentional decisions instead of reactive ones.

The 180-day window is when you decide whether the exit was a finish line or an inflection point.

Most founders treat it like a finish line and make decisions accordingly. The ones who treat it like an inflection point (and plan accordingly) end up in a completely different place five years later.

Day 1: He has $13.4M. Day 180: He understands what he should have done differently. Don't let it be a surprise when you get there.

The exit is over. The work begins in the first 180 days after.

If you're approaching a liquidity event or are in the first 6 months after—

The 180-day window determines whether you build wealth or spend it. Know the difference before you're living it.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

First Million: When Wealth Shifts to Stewardship

The first million is a psychological inflection: from accumulation to stewardship. At this point, estate planning, asset protection, and family governance become urgent decisions.

You Didn't Earn This Money. That Doesn't Mean You'll Lose It.

The feeling that you're not the kind of person who has this much money is extremely common after inheriting. It doesn't make you reckless — it makes you frozen. And 18 months in a money market fund while you 'figure it out' is a real financial cost, not a safe choice.

Liquidity Event Sequencing: Pre-Exit Tax Planning for Founders

Real exit tax savings (15-25% of proceeds) come from decisions 12-18 months before close. Master charitable structures, entity optimization, QSBS timing, and option planning.