The Burnout Number: Calculating the Price of Your Freedom

I have an ex-colleague from a startup I once worked at to whom I am writing this post. A, man, if you're reading, I am sending you my love.

It's Sunday evening and you have the blues and dread what Monday will bring. You earn $350k a year, have $3M in the bank, and you are arguably one of the most smartest people you know.

But you are miserable and you're making everybody else at home as miserable as you feel.

El Padron is so unbearable, that you find excuses not to have to talk to him, your equity is trapped in golden handcuffs, and you haven't sat down for dinner with your family during the week in ages. You want to quit. You need to quit. But you don't.

Why?

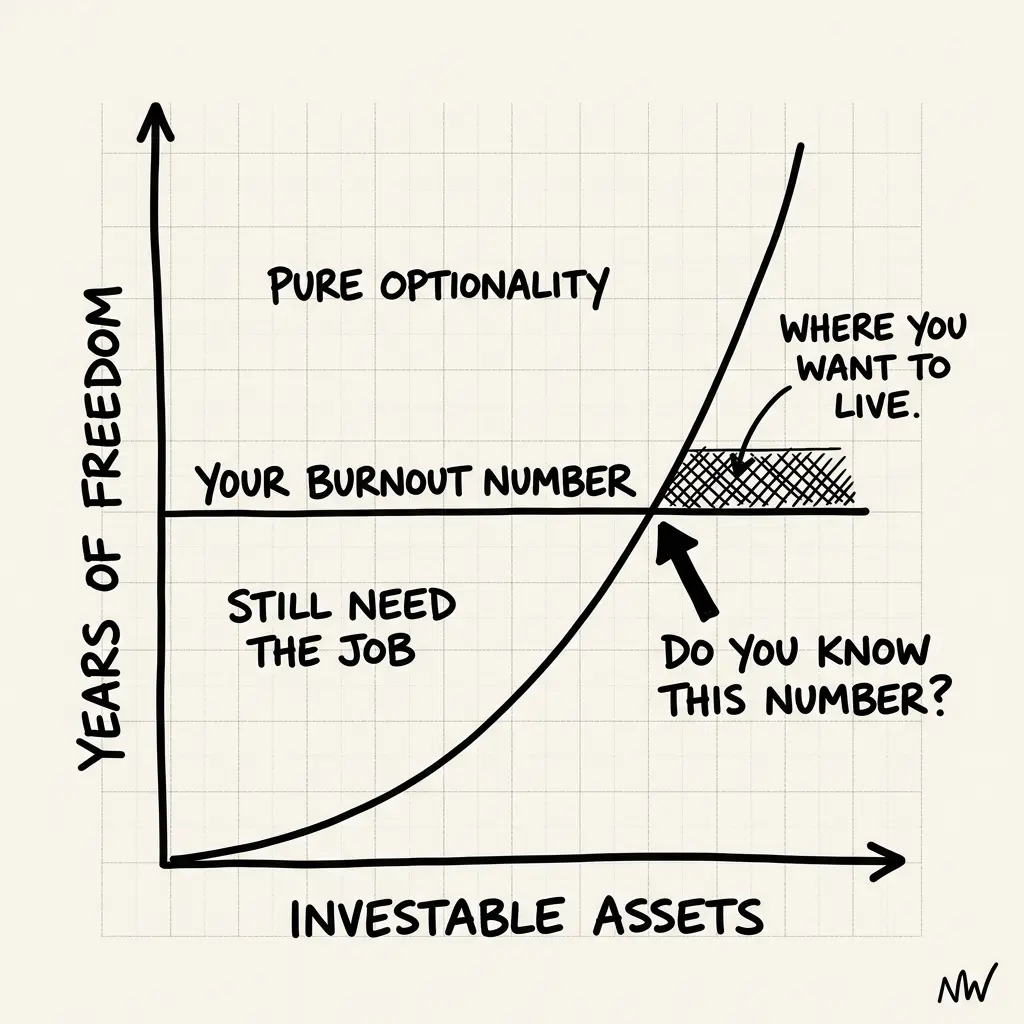

Because you don't have a number. You have a vague cloud of anxiety that screams "if the income stops, the lifestyle collapses."

The RIA industry loves this anxiety. It keeps you working, accumulating, and paying their AUM fees. They tell you to "stay the course" until 65.

But you can't wait until 65, you won't live that long if you continue down this path. You need to know if you can leave today.

Here is the math.

The Variable: Your "Lifestyle Floor"

Most calculators use your current spend. This is wrong. Your current spend is inflated by "anxiety coping costs"—the takeout dinners, the convenience services, the "I deserve this because I suffered today" luxury vacations.

To find your Burnout Number, calculate your Lifestyle Floor:

- Mortgage/Tax/Insurance: (The fixed nut)

- Groceries/Utilities: (The survival nut)

- Kids' Fixed Costs: (School/Activities)

Ignore entirely: Travel, Dining Out, Gadgets, Cars.

These are variable dial-knobs. You can turn them down to buy freedom, or turn them up when you consult later.

The Calculation: (Floor x 25) + The Bridge

The traditional 4% rule (Spend x 25) assumes a 30-year retirement. But you aren't retiring; you are pivoting. You likely won't earn zero forever. Hell, you already have alternative income streams.

The Burnout Number Formula

Burnout Number =

(Floor × 25) + The Bridge

The Bridge is 2 years of pure cash (Lifestyle Floor x 2) held in short-term treasuries.

- Why 25x? It generates a perpetual 4% income stream from your portfolio to cover the basics.

- Why the Bridge? It prevents "Sequence of Returns Risk" (selling stocks in a crash) and, more importantly, Psychological Sequence Risk (panicking because you see your balance drop in month 1).

The Simulation: Exec at $3M Net Worth

- Current Income$350,000

- Current Spend$180,000 (bloated)

- Lifestyle Floor$120,000 (Essentials)

The Math:

- Target Portfolio: $120k x 25 = $3.0M

- The Bridge: $120k x 2 = $240k

- Total Burnout Number: $3.24M

The Verdict: You have $3M. You are $240k short of total perpetual freedom.

The Decision Matrix

You have three choices:

1. The Grind

Stay for ~9-12 months to hit $3.24M. (Risk: Mental breakdown)

2. The Downgrade

Refinance or cut the Floor to $100k. New Number: $2.7M → You were free yesterday.

3. The Pivot

Quit now. Your portfolio already covers your floor ($120k). You bridge the gap with alternative income or consulting, never touching the principal.

Stop Guessing. Solve for X.

Anxiety thrives in ambiguity. We set out to build simulations that turn your panic into an equation.

We model your exact Balance Sheet, RSU vesting schedule, and spending data to find your precise Burnout Number.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

Burned Out at $400K With $2M in the Bank. What Would People Like You Actually Do?

Karan messaged at 2pm on a Tuesday — during work hours. He has $2.1M and earns $410K. He's not asking if he can afford to leave. He knows that. He's asking what people in his exact financial situation actually chose, and how it went.

You're Making $400K and You Still Don't Feel Wealthy. Here's Why the Benchmark Is Wrong, Not You.

Priya earns $420K in San Francisco, has $800K saved, and feels behind. She's comparing herself to HENRYfinance posters who have no parents to support, no cross-border obligations, no Bay Area cost structure. The benchmark is wrong, not her.

You're Probably Planning for the Wrong Retirement Country

If you assume India but stay in the US (or vice versa), every number in your retirement plan is wrong. The most important assumption in your plan is unspoken.