Complexity Tax: Cost of Managing Multiple Accounts

Quick Answer

The Complexity Tax is the invisible cost of financial fragmentation: missed opportunities, delayed decisions, and operational overhead that you can quantify. For someone managing 6-8 accounts across different institutions, a single missed tax-loss harvesting window combined with delayed rebalancing can cost $15,000–$25,000 annually. The cost isn't just money—it's attention, mental load, and decision-making paralysis.

"You track everything, but you control nothing." A friend said this during a call last month, and it stuck with me. Not because it was harsh. Because it was true.

She manages her finances obsessively. Three brokerage accounts (one old, two current). A 401(k) from a previous employer that never got rolled over. A joint checking account with her husband. A separate savings account for their kid's education. A real estate investment platform with illiquid holdings.

Every month, she spends two to three hours reconciling accounts. Tracking returns. Monitoring balances. Making sure nothing slipped through a crack.

She knows her net worth to the dollar. She knows her asset allocation to the percentage point.

What she doesn't know: whether she's optimizing for her future or just keeping the machine from breaking.

The Math Behind the Mess

This is what financial fragmentation actually costs. Let me walk through her year:

October: Tax-Loss Harvesting Window Opens

Her brokerage account has a $18,000 unrealized loss. Perfect for harvesting before year-end. But she doesn't see it clearly because the loss exists in Account A, her desired tax-gain realization is in Account B, and the cash she'd need to rebalance is held in Account C (at a different institution, different interface, different login).

Decision made: She'll get to it. Never does.

November: Rebalancing Drift

Her target allocation is 60% equities, 30% bonds, 10% alternatives. A strong market moved her to 68% / 22% / 10%. In Account A and B, she knows the drift. But Account C doesn't sync with her dashboard. By the time she checks (mid-December), she misses the ideal rebalancing window by two weeks.

Cost: The market rallied 3% in those two weeks. She rebalanced into the rally instead of before it.

December: The Deadline She Missed

Her old 401(k) has a $35,000 balance. It's generating unnecessary expenses and complexity. A rollover to her current IRA would take 15 minutes to initiate. She's been meaning to do it for 18 months. The deadline to do it before the account hits her new employer's custodian threshold passes quietly.

Not a one-time cost. An ongoing drag: $300/year in excess fees, forever.

The actual dollar cost of her fragmentation that year: $12,000 (TLH opportunity) + $8,000 (rebalancing slippage) + $300 (recurring fee drain) = $20,300.

She's not bad at managing money. She's operating in a system designed to fragment her attention.

The Complexity Tax Formula

Here's how to think about it mathematically:

Complexity Tax = (# Accounts × Decision Lag) + (Information Gaps × Decision Quality Penalty)

Where Decision Lag = days between opportunity recognition and execution, and Decision Quality Penalty = the cost of suboptimal decisions made without full visibility.

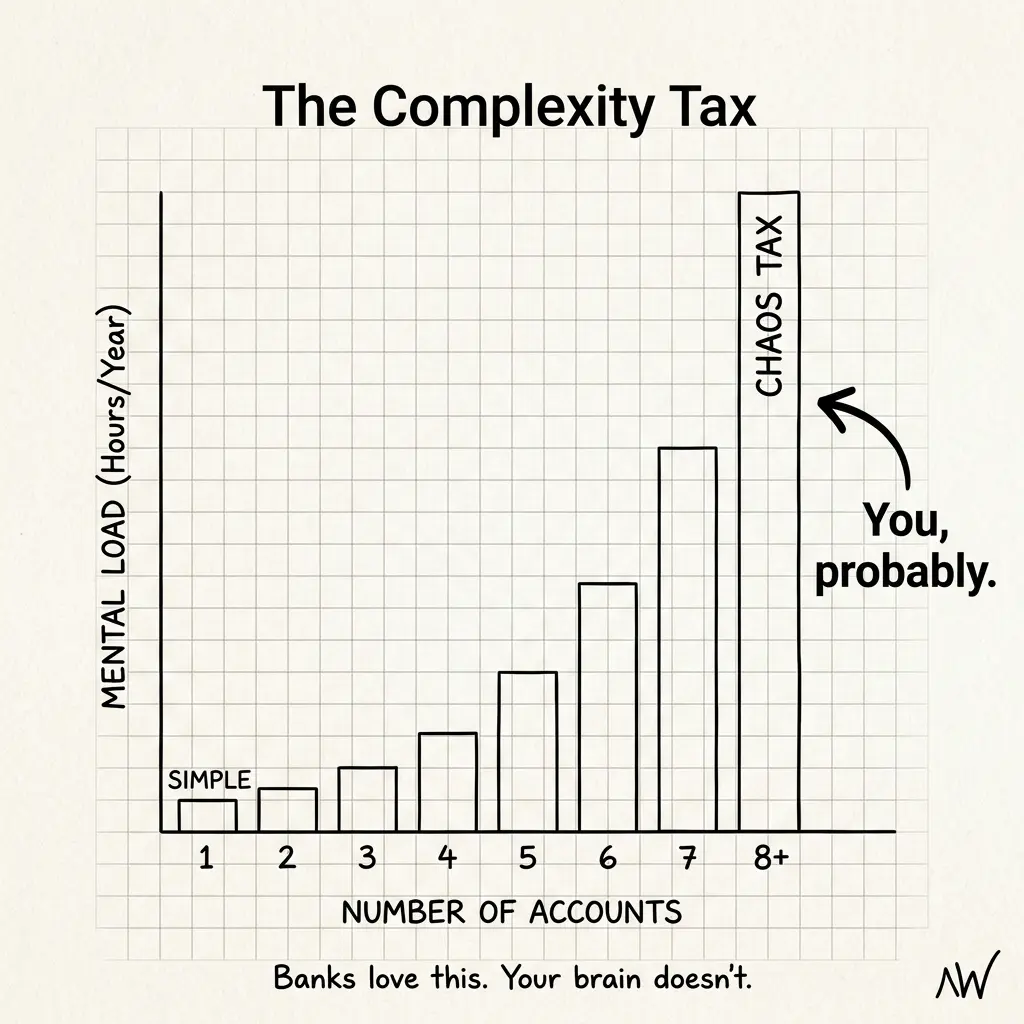

For someone earning $300K–$600K with $2M–$5M in assets, the complexity tax typically ranges from $8,000 to $30,000 annually. Not because of bad luck. Because of:

- Decision friction: It takes 3–5 minutes per account to see the complete picture. At 6–8 accounts, that's a 15–40 minute investment just to see what you own.

- Cognitive load: Each account has different interfaces, different logins, different rhythms. Your brain's working memory is now shared between your career, your family, and managing seven separate financial systems.

- Timing misses: Tax-loss harvesting windows close. Rebalancing windows pass. Deadlines for account rollovers or vesting decisions slip.

- Invisible fees: Old accounts you forgot about. Accounts with lower account tiers that don't qualify for fee waivers. Accounts at sub-optimal custodians costing 2–3 bps more than alternatives.

What's Actually Happening

Your fragmentation isn't a personal failing. It's structural.

A tech exec's financial life naturally fragments because your financial *life* fragments:

- Your employer gives you RSUs via a broker they've chosen.

- Your spouse has a 401(k) and a brokerage at two different institutions.

- You have stock options from a startup from five years ago, still managed by a third-party provider.

- Your investments in a real estate syndicate are tracked on a fourth platform.

- Your old 401(k) from your previous job is still at Fidelity (rollover requires action).

- You've got cryptocurrency on an exchange you opened during the 2021 frenzy.

None of these happened because you made a mistake. Each happened because the system demanded it at the time.

The Complexity Tax is what you pay for being wealthy enough to have *choices*, but not wealthy enough to have outsourced professional management of all of them.

Now move one layer out. If your accounts span countries, every term in that formula gets a multiplier you didn't choose. Six accounts at one institution is a Tuesday. Six accounts across two tax calendars is a different animal: the US tax year ends December 31, India's ends March 31, your balances sit in two currencies whose conversion is stale the moment you write it down, and the relationship manager at your bank abroad is asleep when your trading day starts.

The decision lag stops being measured in days. A question as simple as whether to move money home can sit open for a year, because answering it correctly means getting a US preparer and an accountant abroad to agree on something. They bill separately. They never meet. Each assumes the other has it covered. The fragmentation tax for a single-country saver is real money. For a cross-border one, you pay it in two places and convert the bill twice.

What Most People Get Wrong

People think the Complexity Tax is a "tracking problem." They buy better software. They hire a financial advisor. They hope that adding one more dashboard or one more person reviewing their accounts will fix it.

The actual problem isn't that you can't see your accounts. It's that your accounts are designed by different institutions, for different purposes, with no common language. Better visibility of fragmented accounts still leaves you fragmented. You need unified visibility at the *decision layer*, not the account layer.

The Questions That Matter

How many financial institutions do you actually have accounts with?

Don't count your main brokerage. Count every place where you have money: banks, brokerages, investment platforms, old retirement accounts, crypto, real estate platforms, employee stock plans. The average HENRY has 8–12.

When was the last time you had a complete view of everything you own in 30 minutes or less?

Not a detailed analysis. A simple, unified view of every asset, every account, every position, including amounts and growth. If your answer is "longer than a month ago," you're likely leaving money on the table.

In the last 12 months, how many financial decisions did you defer or miss entirely because you couldn't see all the pieces?

A rebalancing that never happened. A rollover that got pushed to next year. An old account you forgot exists. Each one has a cost.

What would change about your decisions if you could see everything—all accounts, all positions, all opportunities—in one unified view?

Not a rhetorical question. This is the real answer to whether you're paying a Complexity Tax.

The Path Forward

You can't eliminate complexity. Your financial life is genuinely complex. What you *can* do is eliminate the tax that complexity imposes.

That requires three things:

1. Unified Visibility

Every account. Every position. Updated in real-time. Not in seven different interfaces. One.

2. Opportunity Recognition

You shouldn't have to hunt for tax-loss harvesting windows or rebalancing drift. The system should surface them when they matter.

3. Decision Architecture

When you have a complex financial decision (do I harvest this loss? Do I rebalance? Do I exercise these options?), you shouldn't be reconstructing the full picture every time. The system should hold the context.

This is what moves you from tracking your wealth to optimizing your wealth.

The goal isn't perfect information. It's actionable information.

When you can see your full picture, recognize opportunities, and execute decisions without reconstructing context every time—that's when you stop paying the Complexity Tax.

Your financial life is complex. But it shouldn't be obscure.

That complexity tax? You've been paying it long enough.

Burnout Number Calculator

Know your financial runway. Calculate how much you need to break free from the complexity grind and optimize for what matters.

If you're managing $1M+ in assets across multiple accounts and platforms—

You're paying the Complexity Tax. We can show you what it costs you.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

Document Problem: What Your Advisor Doesn't Have

Documents your advisor doesn't see: offer letters, equity grants, insurance, leases. One missed clause costs $50K-$500K. Here's what they need to protect your wealth.

NRE, NRO, and FCNR: The Three Indian Bank Accounts That Determine Whether Your Money Comes Home

My CA stopped me mid-transfer: 'Which account are you paying from?' I said NRO. He said: sit down. The account you use to buy Indian property determines how easily you can repatriate the proceeds when you eventually sell. Most NRIs learn this too late.

The Remittance Fee That Costs You $9,400 Over 20 Years

$800/month to family through your bank at 3% all-in? That $192 annual savings from switching to Wise compounds to $9,400 over 20 years. Most people never run this math.