Document Problem: What Your Advisor Doesn't Have

Quick Answer

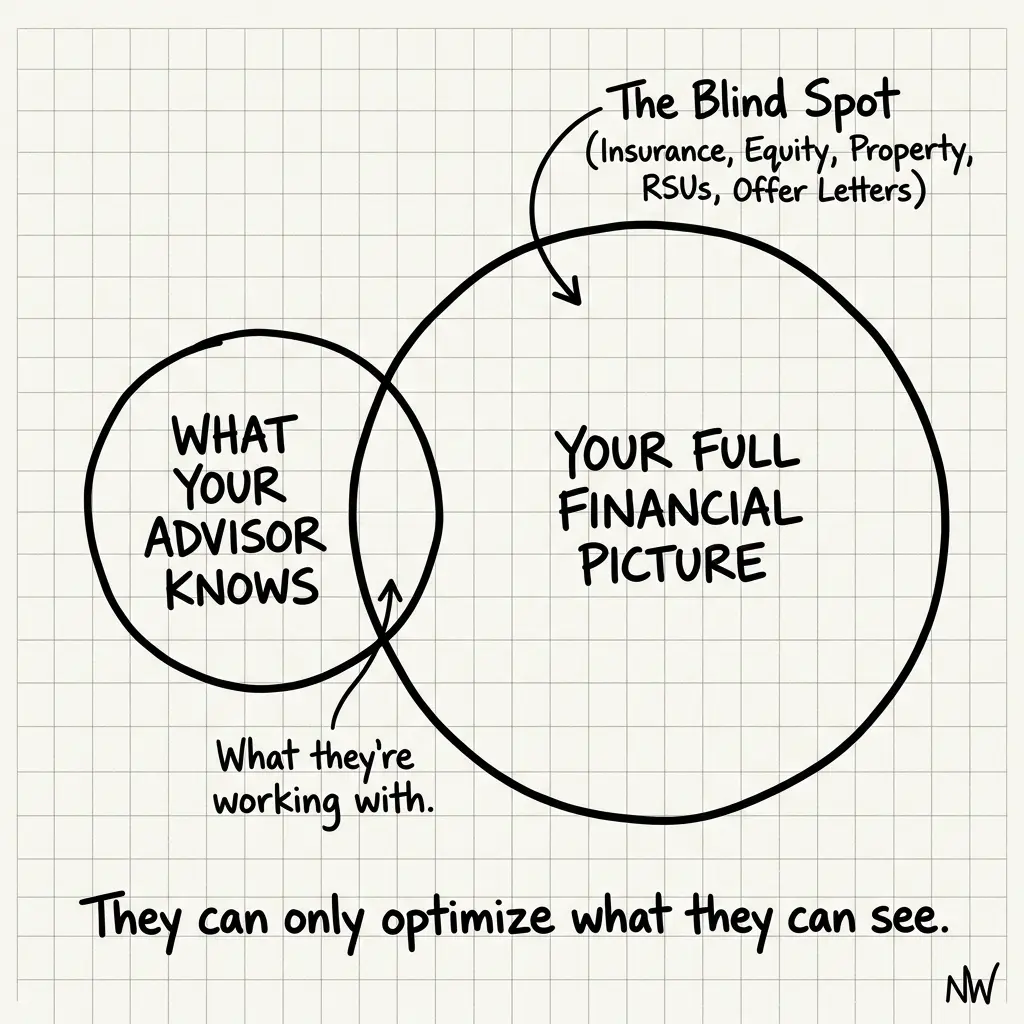

Your financial advisor has your account statements. They don't have your offer letter, your equity grant agreements, your insurance policy, your lease, or your mortgage terms. That information gap is where expensive mistakes happen. For a tech exec, missing a single document clause—an options exercise deadline, a clawback provision, a personal guarantee—can cost $50,000 to $500,000. The document problem is the blind spot everyone has.

I found out I'd left the company by accident. Not from the company. From Carta.

Here's the sequence: I left a company. I knew when. I knew why. I'd done the transition smoothly. Packed up my desk. Handed over projects.

Three months later, I was reviewing my equity positions. I logged into Carta, the cap table management platform where I'd been tracking my options in that company.

And I saw it: My status had changed to "Departed Employee."

I should have known. I did know, intellectually. But the company had never updated my records in Carta. So there was a three-month window where I had terminated employee status everywhere *except* in the system that manages my ability to exercise those options.

That three-month gap cost me the ability to exercise those options at all.

The Mechanical Failure

Most companies give departing employees 90 days to exercise their vested options. After 90 days, they expire.

That 90-day window is supposed to be a courtesy. Time for you to figure out whether exercising makes sense, time to raise the cash if needed, time to understand the tax implications.

The system doesn't require you to *do* anything. It just requires you to *know* the window exists and plan accordingly.

Here's the problem: The information that triggers this window—your departure—lives in three separate places:

- Your company's HR system (where your employment status was updated on my last day)

- Your equity management platform (Carta, Pulley, eShares—where your vesting schedule and exercise rights live)

- Your personal knowledge (you know you left; the system hasn't caught up yet)

If those three things aren't in sync, you have a problem.

In my case, they weren't synced. And I found out by accident, three months late.

What the Documents Should Have Told Me

Here's what I should have had in front of me on Day 1 of my departure:

1. My Offer Letter (or Equity Grant Agreement)

This document specifies the exact 90-day window. Some companies say 90 calendar days. Some say 90 business days. Some have accelerated exercise policies for "good leavers." Mine was plain: 90 calendar days, no acceleration.

2. My Vesting Schedule

How many options had vested as of my departure date. How many were still unvested and would be forfeited. The strike price. The current FMV for tax calculation purposes.

3. A Departure Checklist

The company should have provided a document saying: "You have 90 days from [date] to exercise vested options. Here's the exercise process. Here are the tax forms you'll receive."

They didn't. I got a termination letter with a paycheck calculation. No word on options.

4. Current Cap Table Status

A contemporaneous snapshot showing: "As of [departure date], you hold X vested options at strike price Y. These expire on [90-day-deadline]."

Instead, I found this on Carta, three months late, because I happened to log in.

I had *none* of these documents organized. Not because I'm disorganized. Because the company never gave me a clear, structured departure package. And I wasn't paranoid enough to ask for one.

Why This Matters at Your Income Level

You make $300K–$600K. You have 50–200 basis points of net worth in options at various companies.

For most HENRYs, that means $50K–$500K in potential optionality sitting in documents you've never organized.

Here are the documents you probably have scattered across email, downloads, and your filing cabinet:

- Offer letters with equity terms buried in a PDF you skimmed when you were excited to take the job

- Equity grant agreements that came after the offer, often months later, with terms you didn't read carefully

- ISOs vs. NSOs vs. RSU election forms that determine your tax treatment but disappear after you sign them

- 401(k) enrollment docs with beneficiary designations you haven't updated since you got married

- Mortgage promissory notes with prepayment penalties or refinancing restrictions you never reviewed

- Insurance policies with exclusions that kill the claim when you need it most

- Lease agreements with personal guarantees you didn't realize you signed

- Prenups or trust documents with distribution rules you haven't re-read in five years

There's a sharper version of this problem, and it has nothing to do with being disorganized. If part of your financial life sits in another country, your documents don't just scatter. They split across two professionals who never reconcile. Your US CPA has your W-2 and your brokerage statements. They've never seen the deed to the property you hold abroad. The accountant who handles things back home has seen the deed. They've never read your RSU grant.

I still keep a deed to family land written in Kannada. For years, no advisor I hired could tell me what it meant for the rest of my balance sheet: they couldn't read it, and they didn't have the other half of the picture anyway. When you're cross-border, the document problem isn't a filing problem. It's that the two people holding your papers have never been in the same room.

Each of these documents contains a decision point or a deadline or a clause that affects your financial life. And most of them are invisible until they stop being invisible—usually when something goes wrong.

What Most People Get Wrong

People think the document problem is a filing problem. They buy better document storage. They ask their advisor to review their insurance. They hope that organizing things better will prevent disasters.

The actual problem isn't your filing system. It's that your advisor doesn't have access to the documents that affect your decision-making the most. Your financial advisor sees your accounts. They don't see the clause in your offer letter that could change your tax strategy. They don't see the personal guarantee on your lease that affects your asset protection strategy. They don't see the insurance exclusion that means you're under-insured.

The Real Cost

My missed options exercise deadline cost me the value of those vested options. That's quantifiable. But it's not the only cost.

The broader cost of the document problem:

Timing Misses

Deadlines you didn't know existed. Exercise windows. Refund periods. Rollover deadlines. The 60-day rule on 401(k) distributions. ISOs vs. NSOs tax treatment windows.

Tax Miscalculations

A clause in your offer letter changes how your RSUs are taxed. An insurance exclusion means you can't claim a loss. A mortgage restriction prevents you from refinancing when rates drop.

Liability Surprises

You signed a personal guarantee on your business lease five years ago. You've forgotten about it. A lawsuit against the business puts your personal assets at risk.

Incomplete Planning

Your advisor doesn't know about your prenup or your trust. They can't advise you on estate planning because they don't know what you've already agreed to.

The Questions That Matter

Do you have a single, organized repository of every document that affects your financial decisions?

Not your email inbox. Not scattered across downloads and cloud folders. A single place where you (and your advisor) can find every offer letter, grant agreement, insurance policy, lease, mortgage, and trust document.

Could your financial advisor answer these questions about you right now?

"What's the strike price of your current options?" "Do you have a personal guarantee on any leases?" "What does your insurance actually cover?" "When does your next equity vest?" If the answer is "I'd have to ask you," then your advisor is flying blind.

Have you ever missed a deadline because you didn't realize a document existed?

Not a tax deadline. A deadline buried in a document you signed years ago. An options exercise window. A refinancing cutoff. A rollover deadline.

Who would know if one of your documents had a clause that invalidated your financial plan?

If you had to re-read every agreement you've ever signed to surface that answer, you've found the problem.

The Path Forward

The document problem has one solution: Make your documents visible to the decisions that depend on them.

That means:

1. Centralized Document Storage

Every material document in one place: offer letters, equity grants, insurance policies, wills, trusts, leases, mortgages, prenups. Searchable. Timestamped.

2. Metadata Extraction

The key facts from those documents (deadlines, strike prices, exclusions, guarantees, distribution rules) need to be extractable and queryable. Not buried in a PDF.

3. Decision Integration

When your advisor is helping you make a tax decision, they should be able to see the relevant documents. When you're evaluating a job offer, you should be able to compare it to your existing equity grants.

This isn't about having more information. It's about having the right information at the moment you need to make a decision.

The documents you've signed define your constraints. They should also inform your strategy.

Right now, they're invisible. Making them visible is the path to smarter decisions.

I found out I'd left the company by accident. You shouldn't have to discover your deadlines the same way.

Your documents matter. They should be impossible to ignore.

If you're managing multiple offer letters, equity grants, insurance policies, and agreements—

Your documents should inform every financial decision. Right now, they probably don't.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

Net Worth by Age Charts Are Wrong

The SCF benchmark is the most rigorous household wealth dataset in the US — and it doesn't count your EPF, your Hyderabad apartment, your unvested RSUs, or your NRE FDs. For cross-border HENRYs, the standard benchmark is measuring the wrong person.

Complexity Tax: Cost of Managing Multiple Accounts

Managing 6-8 accounts costs $15K-$25K yearly in missed opportunities. Use the Complexity Tax calculator to see your hidden costs and consolidation strategy.

The Remittance Fee That Costs You $9,400 Over 20 Years

$800/month to family through your bank at 3% all-in? That $192 annual savings from switching to Wise compounds to $9,400 over 20 years. Most people never run this math.