First Million: When Wealth Shifts to Stewardship

Quick Answer

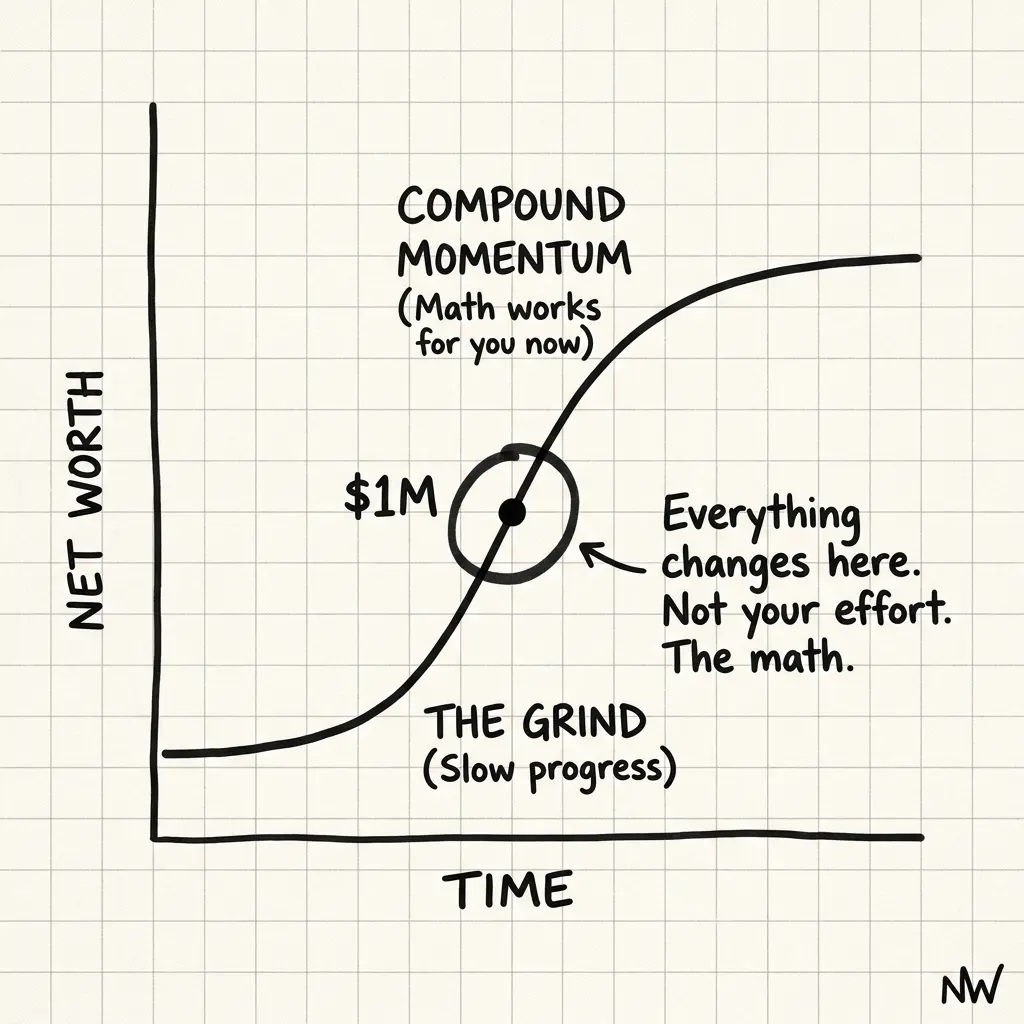

The first million dollars isn't a number. It's a threshold where your definition of wealth shifts. For most people, it marks the moment when "growing wealth" stops being the only question and "stewarding wealth" becomes equally important. The belief change: from "How do I earn more?" to "What do I pass on?" That reframing changes every financial decision you make afterward.

I'd earned more money than my parents had ever accumulated.

I wasn't thinking about it in those terms when I hit the number. I was thinking about rate of return. Tax optimization. Asset allocation.

My parents built a life on solid ground. They saved. They invested conservatively. They gave us a good education. By the time they retired, they had maybe $600,000 to their names. Enough. Not excessive. Stable.

When my net worth crossed $1M, I didn't feel $1M richer. I felt different.

Not because of the number itself. But because of what it represented: I'd now earned more than they'd accumulated over 40 years of work. Through a different economy. With different opportunities. Better timing.

That's when it clicked. This isn't just my money. It's a generational story.

The Shift

Before $1M, all financial thinking was accumulation-focused:

- "How do I earn more?"

- "How do I grow this faster?"

- "What's the optimal return?"

- "Am I on track to hit my number?"

These are healthy questions. But they assume you're still building. That there's a future state you're reaching toward.

Hitting $1M created a psychological inflection point:

The question shifted from earning to stewarding.

Now the questions were different:

- "What do I want this money to do?"

- "What happens to it if something happens to me?"

- "What am I trying to build for the next generation?"

- "How do I ensure this doesn't dissolve or get lost?"

These aren't optimization questions. They're architecture questions.

The Specific Realization

I sat with my wife and did the math: If I wanted each of our kids to inherit more than my parents left us, I needed to think differently about structure.

My parents' $600K was split among three of us. We each got roughly $200K. That's a meaningful foundation. It helped with down payments, career transitions, recovery from failures.

But it wasn't generational. It didn't compound. Each of us started with a cushion and had to build from there.

I wanted something different for my kids: A foundation that wasn't just a cushion, but a *structural advantage*. Something that compounds over their lifetime. Something that lets them make choices from abundance, not scarcity.

That realization changed every financial decision after it.

How It Changed My Decisions

The belief shift wasn't theoretical. It had concrete effects:

1. Estate Planning Became Urgent

Before $1M: "I should probably get a will someday." After $1M: "I need a structure in place now." Wills, trusts, beneficiary designations, guardianship plans—suddenly these weren't theoretical documents. They were the architecture that determined whether my kids inherited $1M or $300K (after legal fees and estate taxes).

That urgency shifted the priority. It became a Q1 project, not a "someday" project.

2. Asset Protection Became Real

Before $1M: "I should look into liability insurance." After $1M: "I need a structure that protects this from lawsuits." That meant evaluating LLCs, trusts, and insurance strategies differently. Not to optimize taxes. To ensure wealth was defensible.

The cost of asset protection (legal fees, structure complexity) made sense when the asset being protected was substantial.

3. Family Governance Became Important

Before $1M: "We talk about money as a family occasionally." After $1M: "We need family financial conversations." How do I explain wealth to kids who didn't earn it? How do I instill values around money if they're growing up with it? How do I involve them in decisions about family wealth?

This led to family meetings, conversations about intention, and explicit discussions about what the wealth is *for*.

4. Diversification Strategy Changed

Before $1M: "I want maximum growth. I'm young." After $1M: "I want stability and diversification. I can't afford to lose this." When the base is smaller, you can take concentrated bets. When you hit $1M and think about passing it on, concentration becomes a liability.

My equity allocation shifted from 80% stocks to 65%. Not because I was old. Because the stakes changed.

5. Charitable Giving Became Strategic

Before $1M: "We donate to causes we care about." After $1M: "Can we create a family charitable foundation? Can we make giving structural?" The math works differently when you have $1M+ vs. $500K. You can afford the infrastructure (DAF, foundation, donor-advised fund) that makes giving more efficient.

Giving went from spending to structure.

What Most People Don't Realize

The first million feels like a destination. In wealth benchmarking, it's treated as a milestone. "First millionaire." That sounds final.

It's not. It's an inflection point.

The first million is when you stop thinking like an accumulator and start thinking like a steward. The second million is when you stop thinking like a steward and start thinking like a legacy-builder. Each milestone shifts the frame.

What Most People Get Wrong

People think "first million" is purely financial. They focus on the achievement and the math. How fast you got there. What you did right. What the return was.

The actual shift is philosophical. It's about where you stand in the intergenerational story. It's about realizing that you're not the end of the wealth story; you're a chapter in it. That realization changes your purpose.

The Questions That Matter

If you lost everything tomorrow, what would your kids inherit? What do you want them to inherit?

The gap between those two answers is the point. Building wealth is one thing. Structuring it so it actually transfers to the next generation is another.

Have you thought about wealth as a conversation with your kids, not just an accumulation number?

Most parents avoid talking about money with their children. But if you're building wealth to pass on, that conversation is essential. What are you building for? What are they expected to do with it?

Do you have a clear structure (trust, will, foundation) that actually transfers what you've built?

Without structure, wealth tends to dissolve through taxes, legal fees, and family disagreements. With structure, it compounds.

What does your wealth *mean*? What is it for?

This isn't a rhetorical question. If you can't articulate why you're building wealth beyond "I want more money," you won't know when you have enough. And you won't know how to pass it on meaningfully.

The Deeper Shift

The first million taught me something that no financial textbook covers: Wealth is generational.

My grandparents built something. My parents sustained and grew it. I benefited from what they'd done and added to it. Now I'm building a foundation for my kids to build on.

That's not a financial statement. That's a story.

And the moment you see wealth as a story rather than a number, everything changes. You stop asking "How much?" and start asking "What for?" You stop measuring success by growth rate and start measuring it by what lasts.

The first million is when you realize you're not building for yourself anymore.

You're building for the future. The one your choices make possible for your kids.

I'd earned more money than my parents had ever accumulated. And instead of that being the end of the story, it became the beginning of a new one.

The first million isn't a finish line. It's a threshold where you realize you're holding something bigger than yourself.

If you're approaching or have passed the first million—

The question changes. It stops being "How do I earn more?" and starts being "What legacy am I building?"

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

180-Day Window: Critical Steps After Liquidity Event

After exit or IPO, 6 months determine everything: over-concentration, tax errors, lifestyle lock-in, estate planning failures. Sequence the right decisions before permanent lock-in.

The Family CFO: When Tracking Everything Still Leaves You Blind

She tracks every dollar across five platforms. She rebalances quarterly. But she still can't answer the million-dollar question: Are we on track?

The Widow's Cashflow: You Are The Single Point of Failure

You have spent decades optimizing your career for efficiency. Why is your family's safety engineered so poorly? The mindshift from 'Provider' to 'Architect'.