Wealth Bounded by Physics: Why Time is the Ultimate Constraint

Last Thursday, 5pm. Google Meet with Patrick Sullivan.

Patrick is 67, based in Tampa, and technically retired. Which means: absolutely not retired.

He spent decades building wealth management software. Sold it. Then got restless.

Now he writes books, learns to code (vibe-style, which I've been teaching him), and every week we trade: I show him how to ship software fast, he mentors me on what wealth management software should do but never does.

Last week, he told me a story I can't stop thinking about.

The Client Who Couldn't Catch Up

Patrick called him David. (Not his real name, but a real situation.)

David was 52. Software exec. Good income—$250K a year. About $400K saved across retirement accounts and taxable.

Lifestyle: nice house, two kids finishing college, aging parents he was helping support. The kind of life you build when you're earning well and living well.

And a goal: Retire at 60 with $2.5M. Not unreasonable. That's the number the financial media tells you. That's the benchmark.

Patrick's software did the math. Even with:

- Maxing out 401(k) contributions

- 7% real returns (optimistic, not crazy)

- Perfect tax optimization

- No major surprises

David would hit maybe $1.5M by 60. Not $2.5M. $1.5M.

Patrick had to tell him: "We need a new goal."

The Fight

David didn't take it well. He thought Patrick's software was wrong. Or too conservative. Or missing something.

So he hired another advisor. One who told him what he wanted to hear:"If we move you into alternatives... if we capture tax alpha here... if markets cooperate... you can hit $2.5M. Maybe even more."

David spent a year chasing that story. And $40K in fees.

Then he came back to Patrick. Quietly. Embarrassed.

"You were right. The math doesn't work. I just didn't want to hear it."

The Reframe

Patrick helped him ask a different question. Not: "How do I get to $2.5M?" But: "What life can I actually build with $1.5M—or $1.8M if I work until 62?"

The answer surprised David.

→ He could downsize (something he and his wife were already considering)

→ He could work part-time for a few years doing something he actually enjoyed

→ He could stop carrying the anxiety of a goal he'd never hit

He's one of Patrick's happiest former clients now. Not because he hit the number he wanted, but because he stopped chasing a benchmark set when he was 25 and started optimizing for the life he could actually live.

"The hardest part of building wealth management software isn't the algorithms or the portfolio optimization. It's getting people to accept what's possible from where they actually are. You can't fight physics."

— Patrick Sullivan

That line has been stuck in my head for four days.

The Wealth Parallel to Physics

A person who is 60kg overweight cannot lose it all in six months. Not because they lack discipline. Not because they're not trying hard enough.

Because biology has constraints. Because the human body is bounded by the laws of physics and the arrow of time. And because life happens...

We accept this intuitively in health. We know that skipping the gym for twenty years has a cost. And we know that cost can't be fully paid off in a single season, no matter how motivated you are.

Yet in wealth, we pretend constraints don't exist.

That's the equivalent of telling someone 60kg overweight:

"Just do HIIT and intermittent fasting and you'll look like you're 25 again."

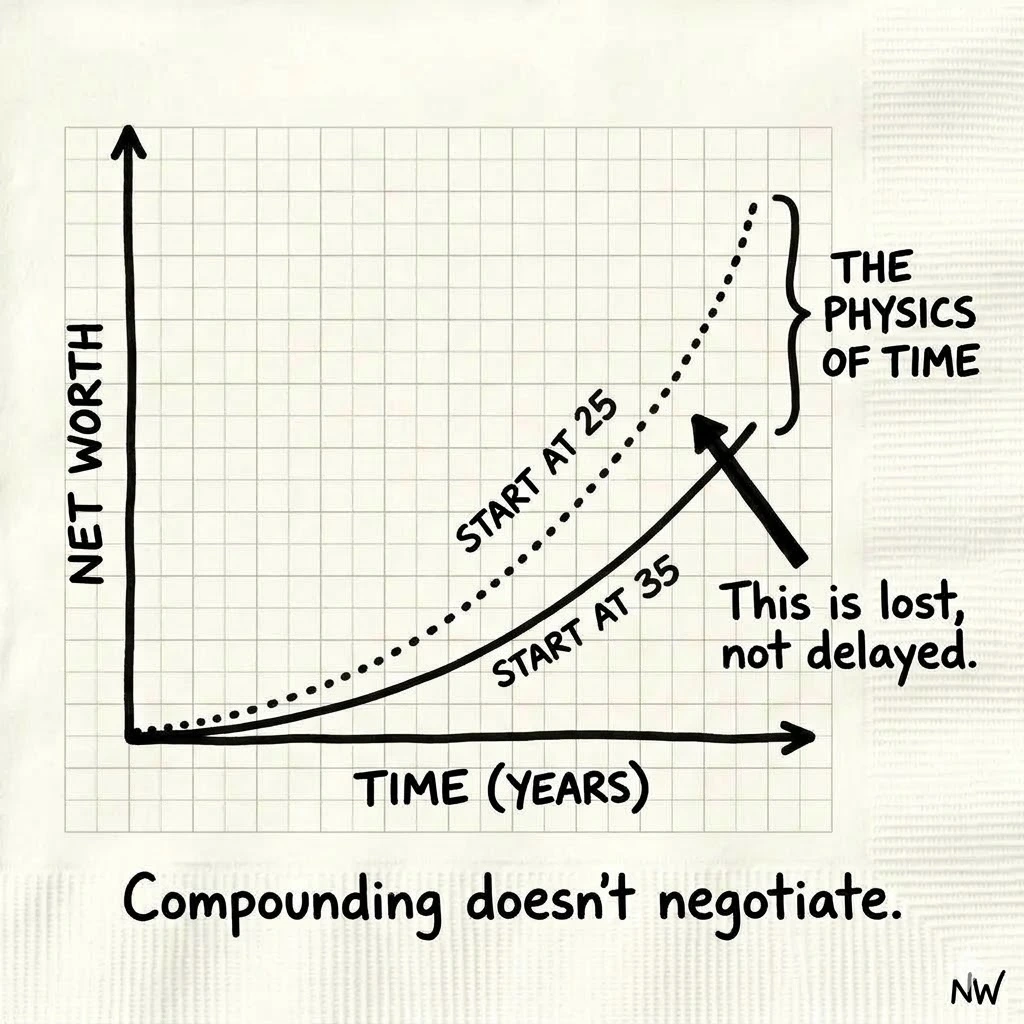

Where You Start > Where You Want to Go

Most financial advice ignores two things: Your starting point and how much time you actually have.

Your "Target Net Worth" is treated like a destination you can simply navigate to—regardless of the fuel in your tank or the weather ahead.

But wealth is path-dependent.

If you're 52 with $400K, you cannot realistically produce the same outcome as someone who started compounding at 30 with the same income. You cannot take the same risks. You cannot aim for the same finish line.

And pretending you can is where catastrophic financial decisions come from.

The Line That Almost No One Says Out Loud

There is a point where chasing the original goal becomes irrational.

Where the marginal effort required to hit a youthful benchmark exceeds the time horizon for that outcome to even matter. Beyond a certain point, the goal has to shift:

From

- "Maximum net worth"

- "Beating the market"

- "Catching up"

To

- "Resilience and simplicity"

- "Predictable income & protection"

- "Not screwing up what I have"

But people don't make that shift. They cling to benchmarks set when they were 25. And that is exactly where anxiety—and bad decisions—come from.

The Real Failure of Wealth Management

The greatest failure of modern wealth management isn't high fees or poor returns. It's the failure to re-anchor goals to reality.

Good wealth management—whether it's software or a human advisor—should have the courage to say:"This is no longer a growth problem. This is now a preservation and regret-minimization problem. This is about avoiding the one mistake that ends the game."

It isn't giving up. It's maturity.

What I'm Building Into NettWorth

When you tell NettWorth your goal—"I want $2.5M by 60"—we won't say "great, here's an aggressive portfolio."

We show you the math.

From where you actually are. With your actual constraints. With your actual risk tolerance and family obligations and lifestyle reality. If you're 52 with $400K and a lifestyle you're not willing to cut—we'll show you what's possible.

Maybe it's $1.5M, not $2.5M.

Maybe you need to work until 63, not 60.

Maybe you need to take more risk than you're comfortable with—and we'll show you exactly what "more risk" means in downside scenarios.

We show you the trade-offs before you waste years—and fees—chasing a goal that physics won't allow.

The service won't just optimize for maximum returns. It tells you the truth about what's achievable. And if your goal needs to change, it helps you find one that's actually worth pursuing. One that fits your life. Not someone else's benchmark from 1995.

If This Is You

If you're 40+ and wondering whether you're on track—or if the goals you set at 25 still make sense—DM me.

I'm 3 weeks from alpha launch. Building this for people who are done with motivational fluff and ready for reality.

You can't fight physics.

But you can master it.

— Roy

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

Income vs. Wealth: Why $500K Salary Doesn't Guarantee Wealth

Same $500K salary, vastly different wealth by age 55 ($3M-$5M gap). The difference isn't investing skill—it's spending discipline. Optimize for the right variable.

First Million: When Wealth Shifts to Stewardship

The first million is a psychological inflection: from accumulation to stewardship. At this point, estate planning, asset protection, and family governance become urgent decisions.

AI Knows the Market. It Doesn't Know You.

Every Davos panel is a purchased narrative. AI amplifies those narratives. But the S&P hitting new highs tells you nothing about whether you should sell your RSUs or refi your mortgage.