What to Do (and Not Do) in the First Six Months After Inheriting Money

The Schwab statement arrived on a Tuesday. The number at the bottom was $3,100,000. You stared at it for a long time and didn't feel rich. You felt like you were holding something breakable that wasn't yours.

That feeling is accurate. And it should slow you down.

The financial industry has a different opinion. Your phone has the voicemails to prove it. "I worked with your father for years." "We specialize in exactly this situation." "I'd love to set up a 30-minute call." They found you because probate filings are public records in most states. The obituary runs, the estate clears, and the cold-call machinery starts.

Here is what they are not telling you: the first six months after inheriting money are almost entirely about not making irreversible mistakes. They are not about investing. Not about optimizing. Not about finding the right advisor. The most valuable thing you can do is slow down in a world that is actively trying to speed you up.

This post is a practical sequence for the first six months. Not a comprehensive financial plan. Just the order of operations that protects you from yourself and from everyone else.

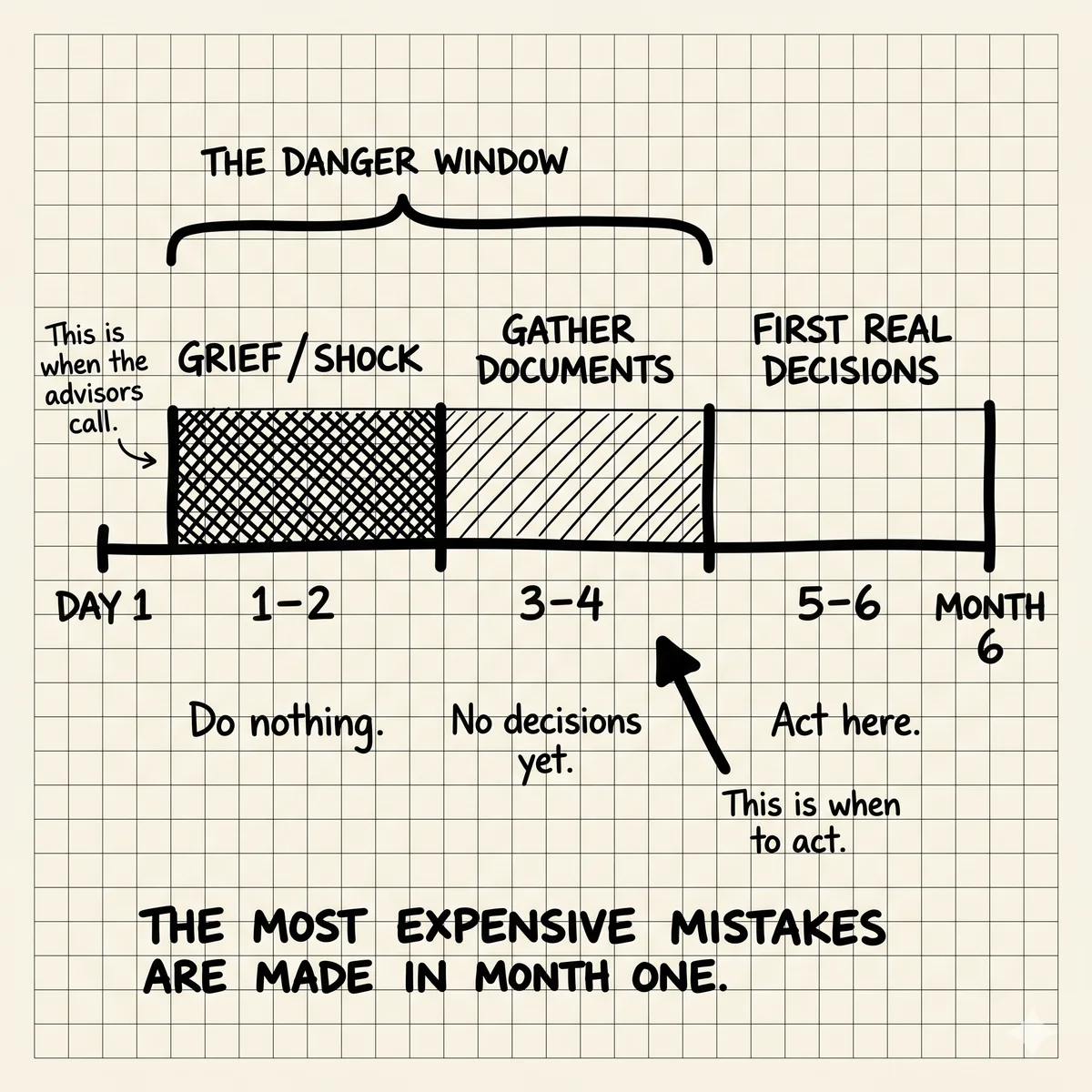

First: The Cash Holding Position Is Fine

Most inherited brokerage accounts land in a money market fund while probate clears. Yours is probably sitting there earning somewhere between 4% and 5% right now. That is not a mistake. That is not "wasted" time. The advisors calling you would like you to believe otherwise. They are wrong.

4.8% on $3M is $144,000 a year. You are not losing money while you think. You are being paid to think carefully. The urgency to "put the money to work immediately" benefits them, not you. It generates a transaction. It starts the relationship. It creates a dependency before you have had time to understand what you actually have.

The one exception: inherited IRAs. If you inherited a traditional IRA, there are required withdrawal rules that have a 10-year clock. We cover that separately. But an inherited brokerage account in a money market fund? You have time. Use it.

Month One: The Inventory

Before you do anything else, you need to know what you actually have. This sounds obvious. It is harder than it sounds.

Inherited wealth often arrives fragmented. A brokerage account at Schwab. A savings account at a local bank you've never used. Half ownership in a Florida condo. A life insurance payout that hasn't hit yet. Possibly a small pension with a survivor benefit. Often there is something the CPA finds three months later that nobody knew about.

Start here: make a simple list. Not a financial plan. A list.

The inventory list:

- What accounts exist and at which institutions

- What the approximate value is in each

- Whether each account has a named beneficiary or went through probate

- Whether there is any real property (house, condo, land)

- Whether there is a trust structure you are now a beneficiary of

- Whether there are any ongoing expenses (property taxes, HOA, maintenance) you are now responsible for

Don't move anything. Don't consolidate anything. Just know what exists.

One practical note: if the brokerage account transferred to you through beneficiary designation (not probate), the cost basis should have stepped up to the date-of-death value automatically. Confirm this with the brokerage. This matters enormously for taxes. We explain it in detail separately (see the piece on basis step-up). But right now, just confirm the basis was updated and write it down.

Month Two: The CPA Conversation

If your parent had a CPA, call that person first. Not because they will manage your investments (they won't and shouldn't), but because they have financial history on the estate that nobody else has. They know what was sold in the last few years, what the carryover losses are, whether there are any estate tax filings still open.

If you have your own CPA, bring them in now. This is the year your tax return gets complicated. There will be a final estate return for your parent. There may be estate tax filings depending on the total size. There will be a new Form 1099 situation for dividends and interest starting from the date the account transferred to you.

The question to ask your CPA: "What do I need to know and do before the end of this calendar year that I cannot undo later?" That is the right question. The answers are usually about basis documentation, inherited IRA distribution timing, and whether you need to make any estimated tax payments on new income.

What you do not need to do: ask your CPA where to invest the money. Most CPAs are not investment specialists. The good ones will tell you this. The ones to be cautious about are those who pivot quickly from "here's what you owe in taxes" to "and here's my colleague who manages money." That referral may be fine. It may also be a fee arrangement neither of them will volunteer to disclose.

Month Three: Estate Matters That Still Need Closing

Even after probate clears, estates trail loose ends. Property in another state may have its own process. A brokerage account that didn't have a beneficiary named may still be in the estate's name. A condo you inherited may need a new deed, new insurance, and a decision about whether to rent it, sell it, or use it.

The estate attorney who handled probate can tell you what is still open. If there wasn't an estate attorney (smaller estates often go through simplified probate), the probate court clerk in the county where your parent lived can usually tell you what needs to be filed.

Real property deserves special attention. An inherited house or condo comes with its own basis step-up (the fair market value at the date of death becomes your cost basis for capital gains purposes). Get a formal appraisal now, not later. The IRS requires a "qualified appraisal" for estate purposes. If you wait a year and then sell, you will have a harder time establishing what the value was at death.

Months Four Through Six: The Decisions That Can Wait

Here is a partial list of things you do not need to decide in the first six months:

- How to invest the brokerage account

- Whether to pay off your mortgage

- Whether to set up a trust for your children

- How much to give to charity

- Whether to change your lifestyle

- What firm to move the assets to

- Whether to hire a full-time financial advisor

None of these are time-sensitive in the way advisors will imply. The brokerage account will not stop earning money while you think. The tax advantages are not going to expire in 90 days. The "limited window" to do something is almost always manufactured urgency.

The real time-sensitive decisions in the first six months are:

- Confirm basis step-up on inherited brokerage accounts (do this before you sell anything)

- Understand inherited IRA rules if one exists (there is a 10-year clock)

- Get an appraisal on any inherited real property while the date-of-death value is fresh

- Make sure ongoing expenses on inherited property are being paid (property tax, insurance, HOA)

- Check whether you need to make estimated tax payments on new income this year

That's the actual list. It's shorter than the advisors calling you want it to be.

The Grief Variable

There is a reason researchers call this decision period high-risk. It is not because inheritors are unsophisticated. It is because grief impairs the exact cognitive functions that financial decisions require: working memory, time horizon thinking, resistance to social pressure.

The advisors who contact you in the first three months of probate are not necessarily bad people. Some of them are excellent at what they do. But the timing is not coincidental. Someone who is grieving and suddenly responsible for more money than they have ever managed before is more likely to sign documents they haven't fully read, to hire based on personality rather than structure, to defer to confidence in the room.

The best thing you can do in this window is simply wait. Not forever. Six months is a reasonable horizon. Long enough to finish the inventory, do the CPA work, close the estate matters, and let the acute shock settle enough to think clearly.

You are not behind. You are not losing money. You are doing the thing that most inheritors who later regret their decisions failed to do: slowing down when every force around them was saying move fast.

What to Do When Someone Calls

You don't owe anyone a meeting. "I'm not ready to have that conversation yet" is a complete sentence. So is "I'm working with my CPA right now and will reach out when I'm ready."

If someone is pushing hard on urgency ("there's a window closing," "interest rates are moving," "you want to get ahead of year-end"), that pressure is almost always in their interest, not yours. Urgency is the primary sales tool in this industry. Recognizing it is protective.

If you do want to talk to someone in the first six months, look for fee-only fiduciary advisors. They charge flat fees or hourly rates. They do not earn commissions on what you buy. They have a legal obligation to act in your interest. Find them through NAPFA, the Garrett Planning Network, or the XY Planning Network. We cover this in more detail in a separate post on how to evaluate advisors.

The One Useful Framing

Your job in the first six months is not to "put the money to work." It is not to honor your parent's memory by investing wisely. Those are month-seven-and-beyond problems.

Your job right now is to not make a mistake you can't undo. That means: don't sell inherited assets before confirming the basis step-up. Don't sign advisory agreements when you're still in the fog of probate. Don't move money to a new institution until you understand what you're moving and why.

The money market fund is not failing you. It is holding space while you do the work that actually needs to happen first.

You have more time than everyone calling you is implying. Use it.

NettWorth is a financial intelligence platform, not an advisory firm.

We are building it for people who want to understand their own financial situation clearly before anyone else does. No commissions. No products to sell. If you are a recent inheritor navigating this for the first time, you're not trusting us with your money, but with the analysis that helps you make the decisions on what to do with it. If that framing resonates, you can join the founding cohort at nettworth.com.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

The Healthcare Horizon: Real Costs for Early Retirees (Ages 40–65)

You stress-tested recessions, sequence of returns, and market crashes. But the spreadsheet goes blank on healthcare. Here are the real numbers.

Life Insurance as Financial Tool

You can self-insure mortality risk. You cannot self-insure the gap between your wealth and your family's actual needs. Here's what actually matters when you have millions.

The Estate Planning Inflection: Structures That Work While You're Alive

Most people think trusts are for death. They're wrong. Here's what wealthy business owners do while they're alive to protect what they've built.