Questions & Answers

Do I need to file FBAR if I have accounts in another country?

Yes, if the aggregate value of all foreign financial accounts exceeds $10,000 at any point during the calendar year, FinCEN Form 114 (FBAR) is required by April 15 (with automatic extension to October 15). This is separate from FATCA Form 8938, which has different thresholds and applies to specified foreign financial assets. Non-willful failure penalties start at $10,000 per account per year; willful failure penalties can reach the greater of $100,000 or 50% of the account balance.

How is a UK pension treated for US tax purposes?

UK workplace pensions and SIPPs are generally taxable in the US, with the US-UK tax treaty (Article 17) providing some relief. The complexity: contributions to UK pensions aren't deductible in the US, creating potential double-taxation. Many cross-border professionals have significant unrecognized pension assets — the UK pension exists in British pounds in a British institution, and no US-facing financial tool consolidates it with US retirement accounts. This creates a systematic undercount of total retirement assets.

What is the wealth impact of holding assets in multiple currencies?

Currency risk is the most underestimated factor in cross-border net worth. A 10% USD/GBP movement creates a 10% swing in the USD value of UK assets — with no market movement required. Over a decade, unhedged multi-currency exposure can erode effective purchasing power by 8–15%. True net worth for a cross-border professional requires currency-normalized consolidation to a base currency, updated regularly.

How is PPF (Public Provident Fund) treated for US tax purposes?

PPF is not automatically treated like a Roth IRA. The IRS position is ambiguous — some practitioners treat it as a foreign trust requiring Form 3520; others report only distributions. The asymmetry matters: most NRIs have been contributing for years without knowing their US reporting obligations. PPF also appears on the FBAR threshold calculation if combined with other foreign accounts, which many people miss. NettWorth flags your India-side account structure against your current FBAR filing profile so your CPA has the complete picture before filing.

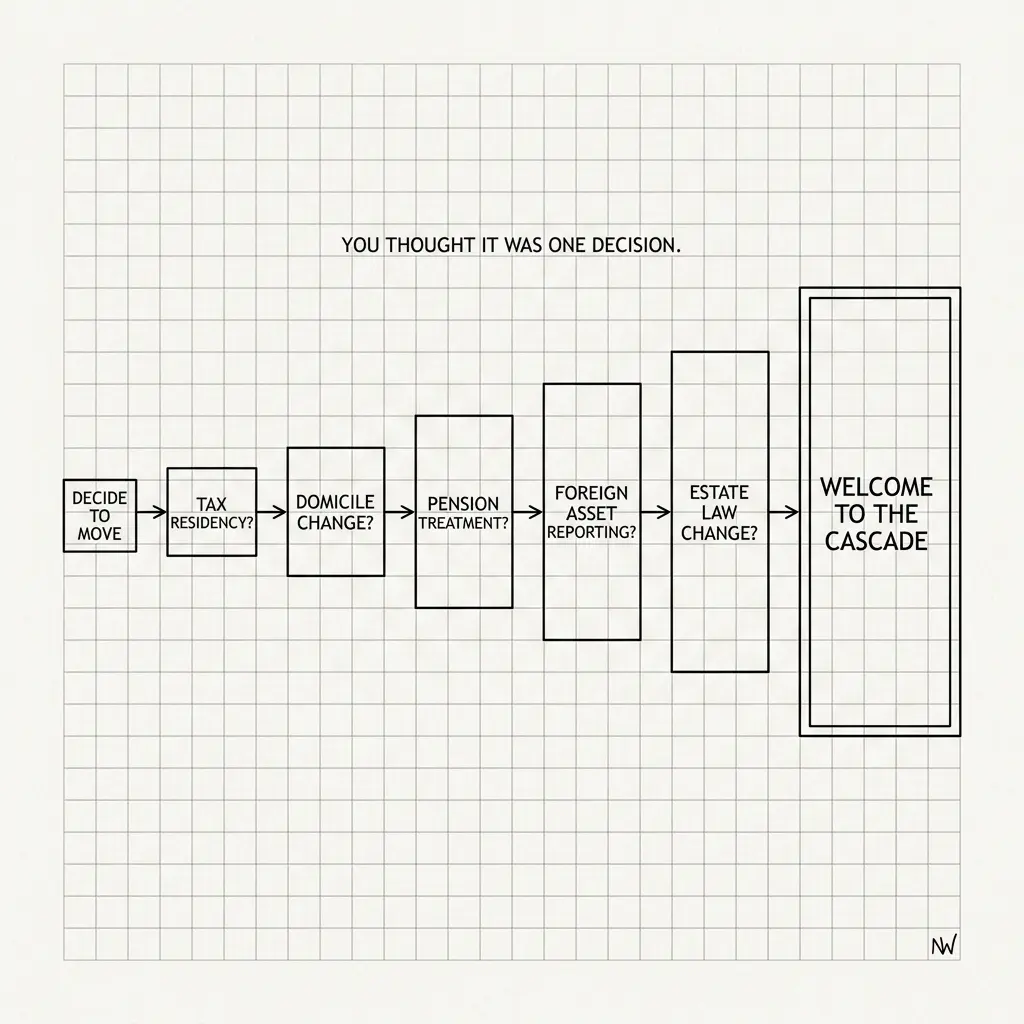

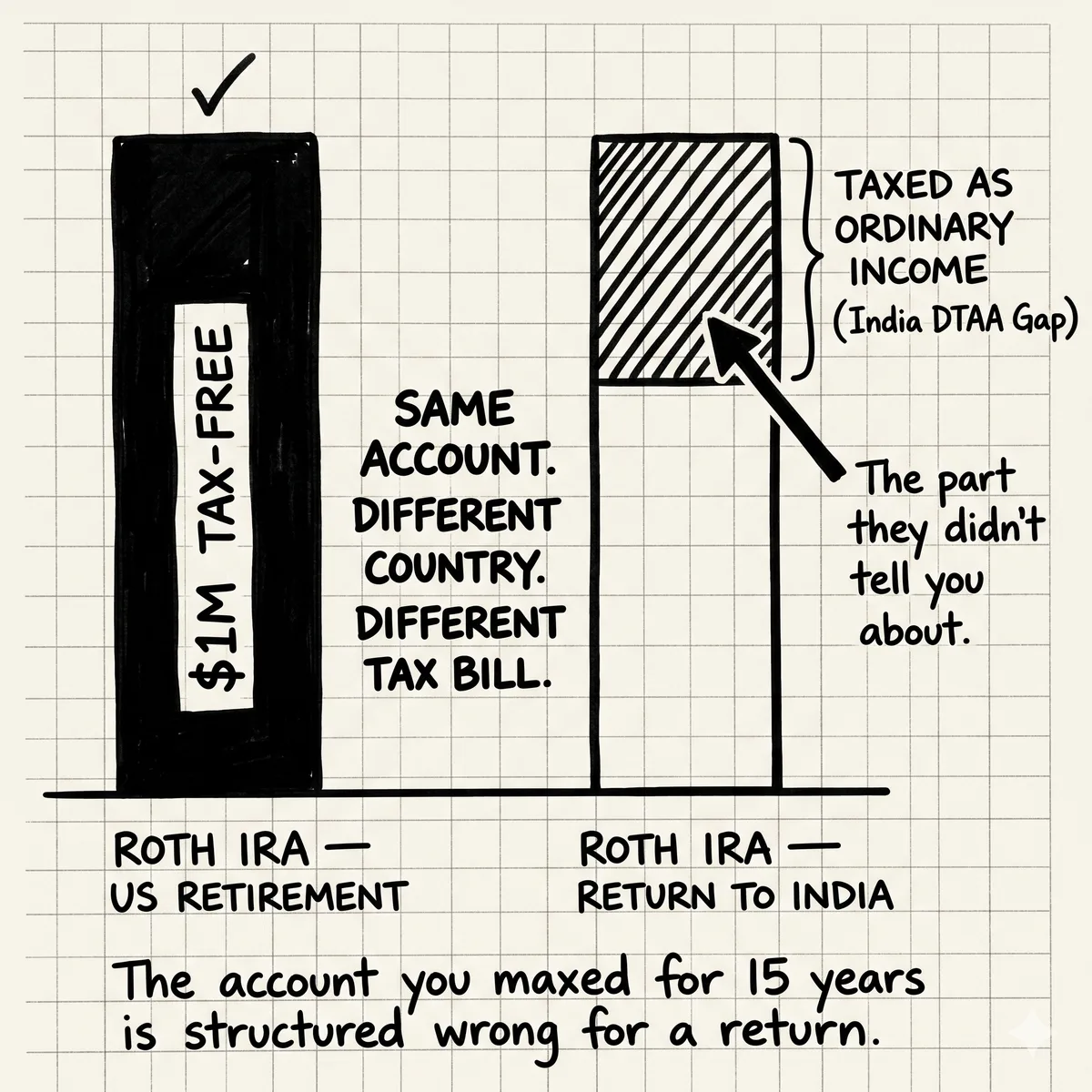

What is the RNOR window and why does it need to be planned before returning to India?

RNOR (Resident but Not Ordinarily Resident) is a 2–3 year status window after returning to India during which foreign income — including 401k distributions and US brokerage gains — may not be taxable in India. It's the most valuable tax window available to returning NRIs, and it has to be planned while you're still in the US. Decisions about Roth conversions, 401k distributions, and US property sales need to happen before your RNOR window opens, not during it. Most NRIs only discover this after they've moved — when it's too late to take full advantage.