Roth IRA Is a Tax Trap for NRIs Returning to India

My CA in Bangalore had been doing US-India returns for 15 years. The first time I sat with her, she was walking me through a returning client's US accounts — anonymized, with his permission, because she wanted me to see the pattern. 401(k). Brokerage. Then she stopped at the Roth, quiet for a moment, and said, "This one wasn't set up for India."

I asked what she meant.

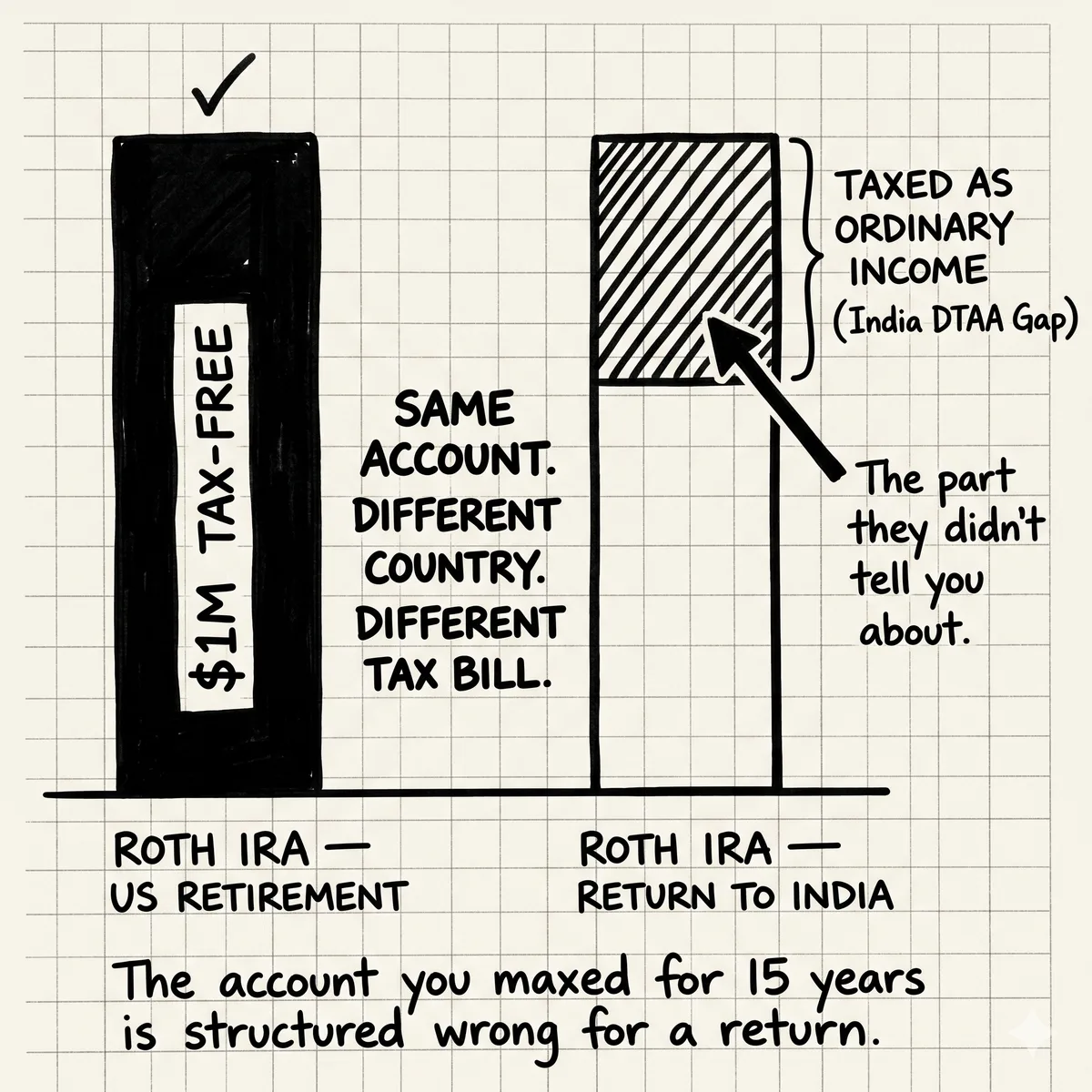

She wrote his Roth balance on her notepad. Then she wrote a second number beside it: what India would take. The gap between the two was the whole reason she'd wanted me to see this file.

He'd maxed the Roth for 11 years. Every year, the same US advice: max it, it's tax-free forever. He maxed it. The account had grown well. Nobody had ever asked him what "tax-free forever" means when "forever" includes living in a different country.

It doesn't mean tax-free forever. It means tax-free in the US. India takes a different view, and India's view governs the years that matter most.

The account everyone told you to max is structured wrong if you're returning to India. Most people find this out too late to fix it.

How Roth IRAs Work (The Part You Know)

You contribute after-tax dollars. The money grows tax-free. Qualified distributions in retirement are tax-free. No required minimum distributions. You can pass it to heirs tax-free. In the US, this is one of the best retirement vehicles available.

The pitch is simple: pay taxes now at your current rate, and never pay taxes on that money again, even as it grows to 3x or 5x what you put in.

For someone who retires in the US, this pitch is largely accurate. The US honors the Roth's tax treatment. Distributions aren't taxed. The IRS doesn't touch them again.

For someone who returns to India, the pitch breaks down at the most important moment.

The India Treaty Problem

The US-India Double Tax Avoidance Agreement (DTAA) was signed in 1989. It covers a lot of income types. It does not specifically recognize Roth IRAs.

The treaty predates Roth IRAs. Roth IRAs were created in 1997. The treaty hasn't been substantially updated to address them.

As of 2026, that's still the case: no Roth-specific provision in the treaty, and no CBDT guidance telling an Indian assessing officer to treat a Roth as anything other than ordinary income from a foreign retirement scheme. That silence is the default you inherit when you land.

The India Income Tax Act treats Roth IRA distributions as income from a "retirement benefit scheme." The exemption that makes Roth distributions tax-free in the US is a US law exemption. Indian tax law doesn't recognize it.

The practical result: when you take a distribution from your Roth IRA as an Indian tax resident, India taxes it as ordinary income. The 30% slab rate applies above INR 15 lakhs. At the income levels most returning NRIs have, you're looking at 30% Indian tax on distributions you already paid US tax on when you contributed.

This isn't double taxation in the classic sense.

Classic double taxation is paying tax on the same income in two countries simultaneously. This is different. You paid US tax when you contributed. You paid no US tax on growth or distributions. India now taxes your distributions. The tax wasn't "double" at any one moment, but across the lifecycle of the account, you paid US tax going in AND Indian tax coming out. The tax-free growth gets taxed at exit. You got the growth and then paid for it.

The Actual Math: $1M Roth vs. $1M Traditional on Return to India

Scenario: $1M Roth IRA, return to India at 60, draw down over 25 years

- Annual withdrawal: $40,000 (4% rule)

- US tax on withdrawal: $0 (Roth, qualified distribution)

- India tax on withdrawal (as Indian tax resident): 30% on income above INR 15L threshold

- At current exchange rates (~84 INR/USD), $40,000 = INR 33.6L

- India tax on INR 33.6L: roughly 25-28% effective rate after slab calculations

- India tax per year: approximately $10,000-$11,200

- Over 25 years: $250,000-$280,000 in Indian income tax on after-tax Roth money

Scenario: $1M Traditional IRA, return to India at 60, draw down over 25 years

- Annual withdrawal: $40,000

- US tax: 10% withholding under DTAA Article 20 (can be reduced/refunded depending on structure)

- India tax: Same ordinary income treatment, 25-28% effective rate

- DTAA credit: India allows credit for US withholding tax paid

- Net India tax (after DTAA credit): approximately 15-18%

- India tax per year after credit: approximately $6,000-$7,200

- Over 25 years: $150,000-$180,000 in total tax on pre-tax Traditional IRA money

Note: Traditional IRA benefits from DTAA credit mechanism that Roth doesn't get because there's no US tax withheld on Roth distributions to credit against.

The Traditional IRA, which everyone treats as the inferior option for high earners in the US, turns out to be the superior vehicle for India returnees. You deferred US tax on the way in. India taxes on the way out. But you get DTAA credit for the US withholding. Net effective rate is lower.

The Roth, which everyone treats as superior, has the worst India outcome. No US tax on distribution means no DTAA credit. India taxes the full distribution with no offset.

The Timing Problem

Here's what makes this particularly painful: the people who maxed Roth IRA aggressively are usually the high earners who did it during their peak earning years. That's the correct US strategy. The Roth makes the most sense when you're in the highest tax brackets and expect your retirement income to be lower.

But the high earners who maxed Roth in their peak years are often doing so because they're in the US on H1B or green card, making FAANG-level compensation in the $250K-$500K range. These are exactly the people who have a non-trivial probability of returning to India at some point.

They built the tax liability without knowing they were building a tax liability. The advice was correct for a US-retirement scenario. Nobody flagged that it was wrong for a return scenario.

The mega backdoor Roth compounds this problem. If you've been doing the mega backdoor and have $800K-$1.2M in Roth accounts, the India tax exposure is substantial. You paid tax going in. Growth was untaxed. Now India wants 25-30% on every dollar you pull out.

What to Do Instead

If you're still in the US and have time to restructure, you have options. None of them are simple. All of them require planning ahead of your return.

The RNOR Window Strategy

When you return to India, you pass through a status called RNOR (Resident but Not Ordinarily Resident) for 2-3 years. During RNOR, foreign income is generally not taxed in India. This window is the optimal time for Roth conversions in reverse, or more accurately, for taking large Roth distributions because India won't tax them during RNOR.

The problem: most people arrive in India and figure this out a year into RNOR. They've already wasted part of the window. The entire strategy has to be set up before you leave the US, not after you arrive in India.

Strategic Distribution Timing

If you're in RNOR, take large Roth distributions during those 2-3 years. You pay no US tax (qualified Roth distribution). India doesn't tax foreign income during RNOR. This is the window when Roth distributions are actually tax-free on both sides.

After RNOR status ends and you become ROR (Resident and Ordinarily Resident), all foreign income including Roth distributions becomes fully taxable in India. The window closes.

Traditional IRA Preference Going Forward

If you know you're returning to India and you're still contributing to retirement accounts, Traditional IRA and 401(k) contributions are often better than Roth for your situation. Pre-tax contributions, DTAA credit on US withholding at distribution, lower effective India tax rate. The tax stack for HENRYs with cross-border exposure is fundamentally different from the tax stack for US-only retirees.

72(t) SEPP Distributions

If you're under 59.5 and returning to India, 72(t) substantially equal periodic payments let you take penalty-free distributions from Traditional IRA before 59.5. Combined with RNOR status and DTAA credit, this can be an efficient way to access retirement funds early while tax costs are minimal.

The rule of thumb nobody gives you

If your probability of returning to India is above 30%, maximize Traditional 401(k)/IRA over Roth. If your probability of returning is above 60%, consider stopping Roth contributions entirely and let existing Roth balances sit for strategic RNOR-window distribution.

The Roth vs. Traditional decision is not just a US tax bracket question. It's a retirement country question. The accounts that win the US tax game lose the India tax game.

The Broader Lesson

Every US financial product is optimized for a US life. The tax code assumes you'll stay. The treaties assume you're either fully here or fully gone, not building a life across two systems simultaneously.

Roth IRA is the clearest example of this problem, but it's not the only one. HSAs have similar India treatment issues. Some 529 plan distributions have India complications. The structure of US equity compensation (particularly ISOs) creates India tax events that US advisors don't model.

The financial advice industry is built for people who stay. NRIs don't stay. Or they might not stay. Or they stay until they don't. The advice needs to reflect that uncertainty, not ignore it.

The CA in Bangalore who stopped at that Roth wasn't being dramatic. She was being accurate. The account wasn't built for India. Nobody builds accounts for India when you're 28, earning your first real US salary, and someone shows you the Roth growth chart.

The fix isn't complicated once you understand the problem. The backdoor Roth mechanics and the India tax treatment of foreign retirement accounts are both knowable. You just have to ask the question before you've already built the position.

The account everyone told you to max was built for a life you might not live.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

The RNOR Window: The 2-3 Year Tax Opportunity Most NRIs Miss

Your first 2-3 years back in India, foreign income is largely tax-free. It's the window for Roth conversions and asset restructuring. Almost nobody plans for it before they leave the US.

Your EPF Balance Is Probably Taxable in the US. Nobody Told You.

The IRS has not issued clear guidance classifying EPF as a qualified pension plan. The conservative position: interest accruing annually in your EPF is US-taxable income, even if you haven't withdrawn a rupee. Most NRIs in the US have never reported it.

NRI Selling Property in India: The Two-Tax Hit Nobody Explains Clearly

India taxes the property. Your country of residence taxes you. The DTAA doesn't eliminate the second hit — it sequences them and gives you a credit. On a large Indian property sale, the combined effective rate is closer to 24% than the 12.5% India rate most people quote.