Questions & Answers

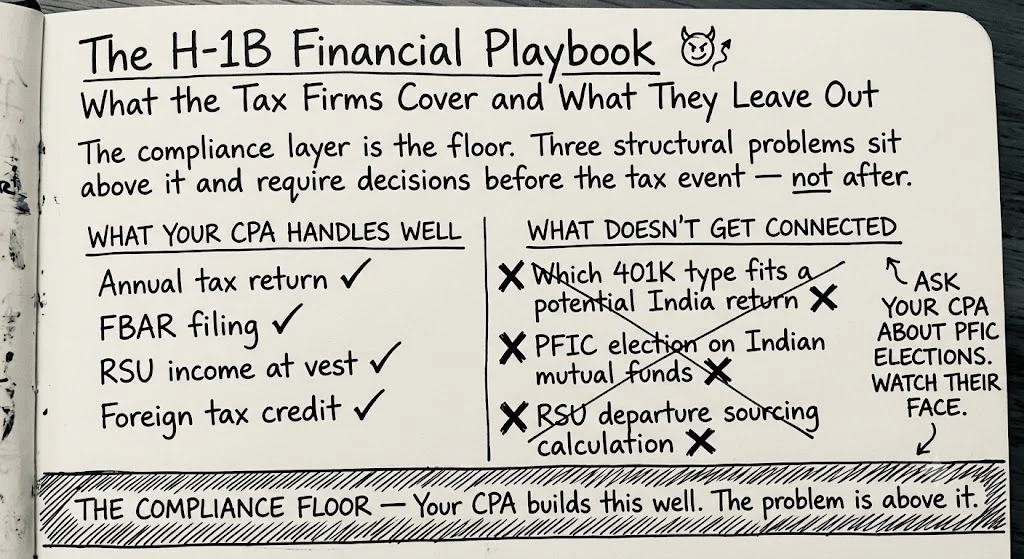

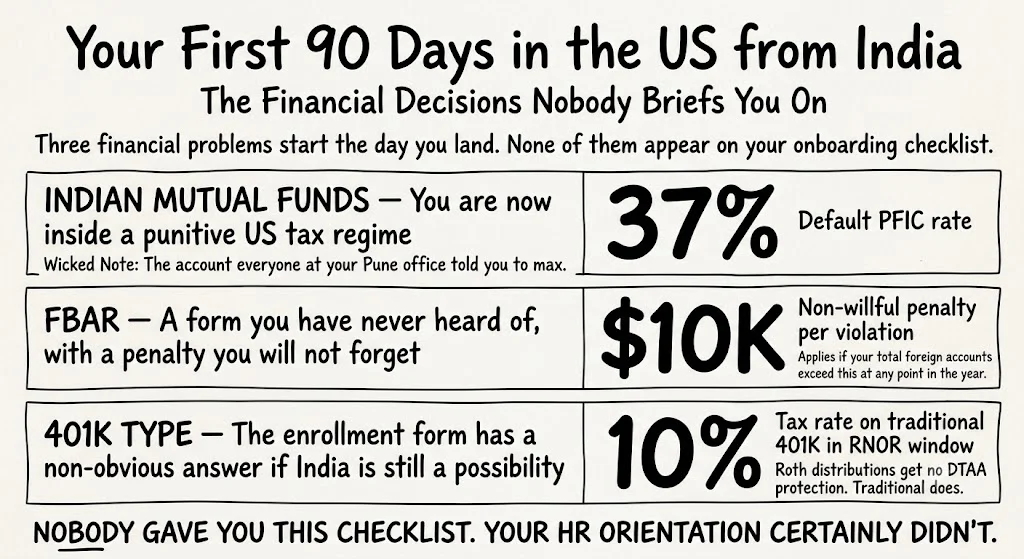

Should I choose Traditional 401K or Roth 401K as an H-1B holder?

It depends on where you plan to retire. If you plan to return to India: the US-India DTAA Article 20 allows India to tax 401K distributions for Indian residents. India does not recognize Roth accounts as tax-exempt — distributions may be taxed as ordinary income in India regardless of which 401K type you contributed to. If you plan to retire in the US permanently, the standard Roth vs. Traditional analysis applies. For anyone with an uncertain timeline, the correct answer is to model both paths before defaulting to 'max out Traditional.'

Do I need to file FBAR for my NRE and NRO accounts as an H-1B worker?

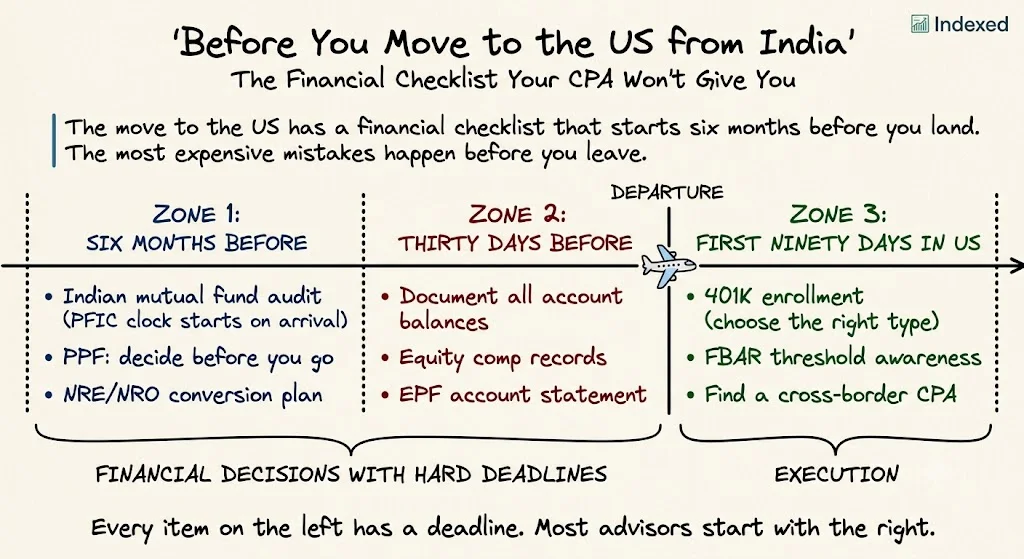

Yes. If the aggregate balance of all your foreign financial accounts — NRE, NRO, savings accounts, PPF, fixed deposits — exceeds $10,000 at any point during the calendar year, FinCEN Form 114 (FBAR) is required by April 15, with automatic extension to October 15. The NRE account's tax-free status in India does not affect FBAR filing requirements. FBAR is a US reporting obligation based on account existence and aggregate balance, not taxability. Non-willful failure penalties start at $10,000 per account per year.

Are my Indian mutual funds a problem now that I'm in the US on an H-1B?

Yes. Indian mutual funds held by US tax residents are classified as PFICs — Passive Foreign Investment Companies — under US tax law. The default tax treatment is punitive: gains are taxed as ordinary income at your marginal rate, plus an interest charge applied to each year's gains. The mark-to-market election (Form 8621) is the most practical alternative for most H-1B holders with Indian equity funds. The window to make this election in your first year of US tax residency is often the most important financial decision H-1B holders don't know exists. After that window closes, your options are worse.

What happens to my RSUs if my H-1B visa fails or I get laid off?

You have a 60-day grace period under USCIS rules after H-1B employment terminates. During that window: unvested RSUs from the terminated employer typically do not accelerate — your plan document controls this, and most people don't check it in advance. RSUs that vest during your grace period may be withheld at the 30% non-resident alien rate if your employer updates your tax status before the payroll runs. Your 401K stays in place and does not need to be moved. If you leave the US within the 60-day window, you may trigger dual-status filing complexity for that tax year.

Is NRE account interest taxable in the US for H-1B holders?

Yes. NRE account interest is exempt from Indian income tax for NRIs — that tax exemption is an Indian rule for Indian residents and NRIs. Once you become a US tax resident (which H-1B holders are, under the substantial presence test), NRE interest is taxable US income, even though the account remains technically an NRE account. The account type doesn't change. Your residency status for US tax purposes does. Most H-1B holders earn NRE interest for months or years before a CPA mentions this. The interest is reportable as ordinary income on your US return from your first day of US tax residency.

See your full picture — both countries, one number.

No bank passwords. No advisor required. Takes 4 minutes.