From the NettWorth Research Library

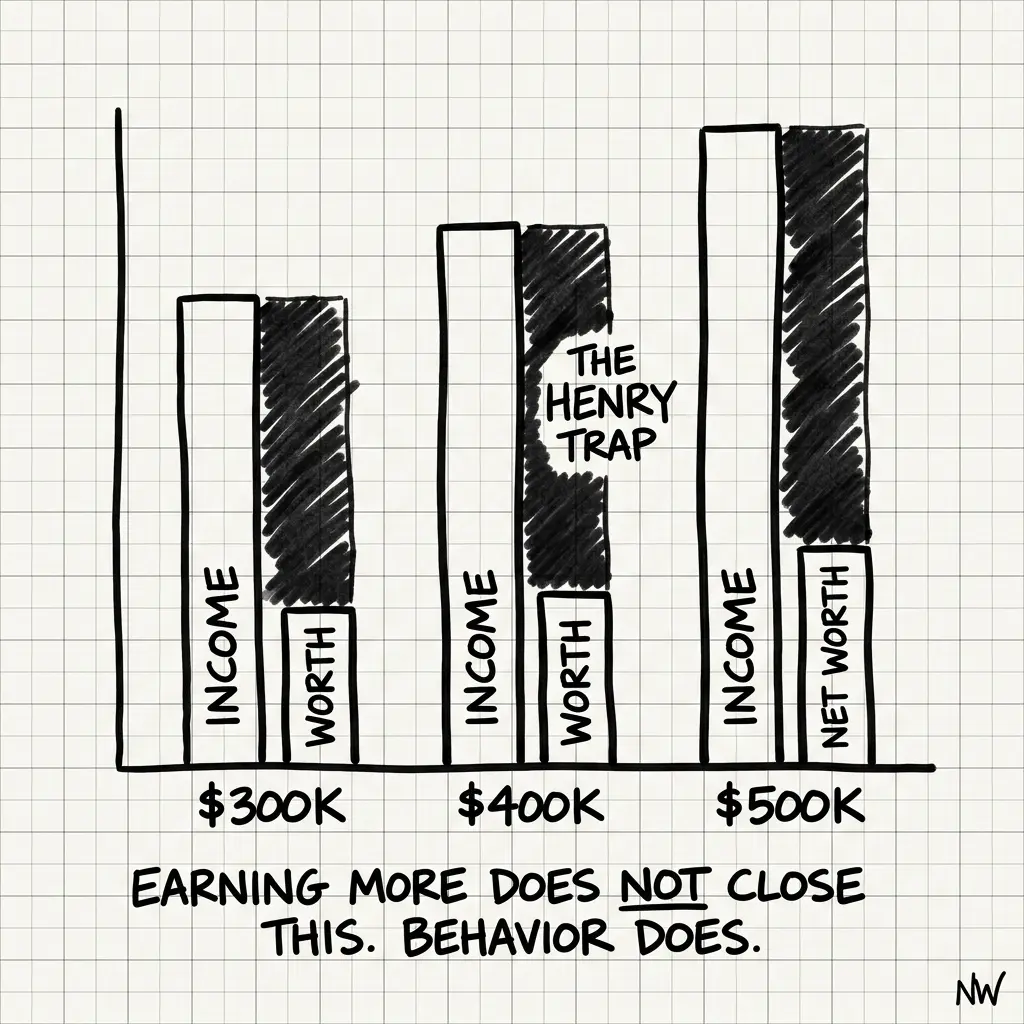

The Wealth Gap

Why the top 5% of earners aren't in the top 5% of wealth-builders — and the three structural causes.

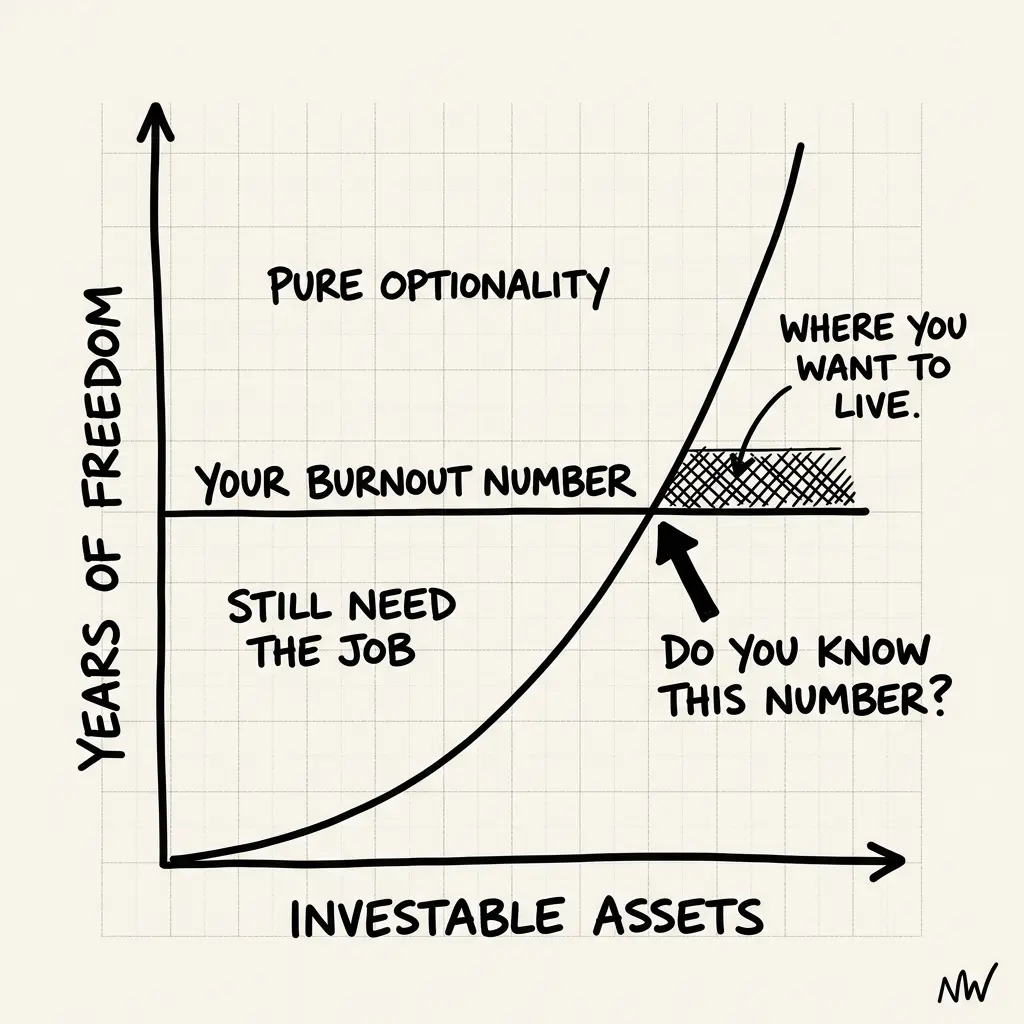

The Burnout Number

The specific number that separates "I have to work" from "I choose to work" — and how to calculate yours.

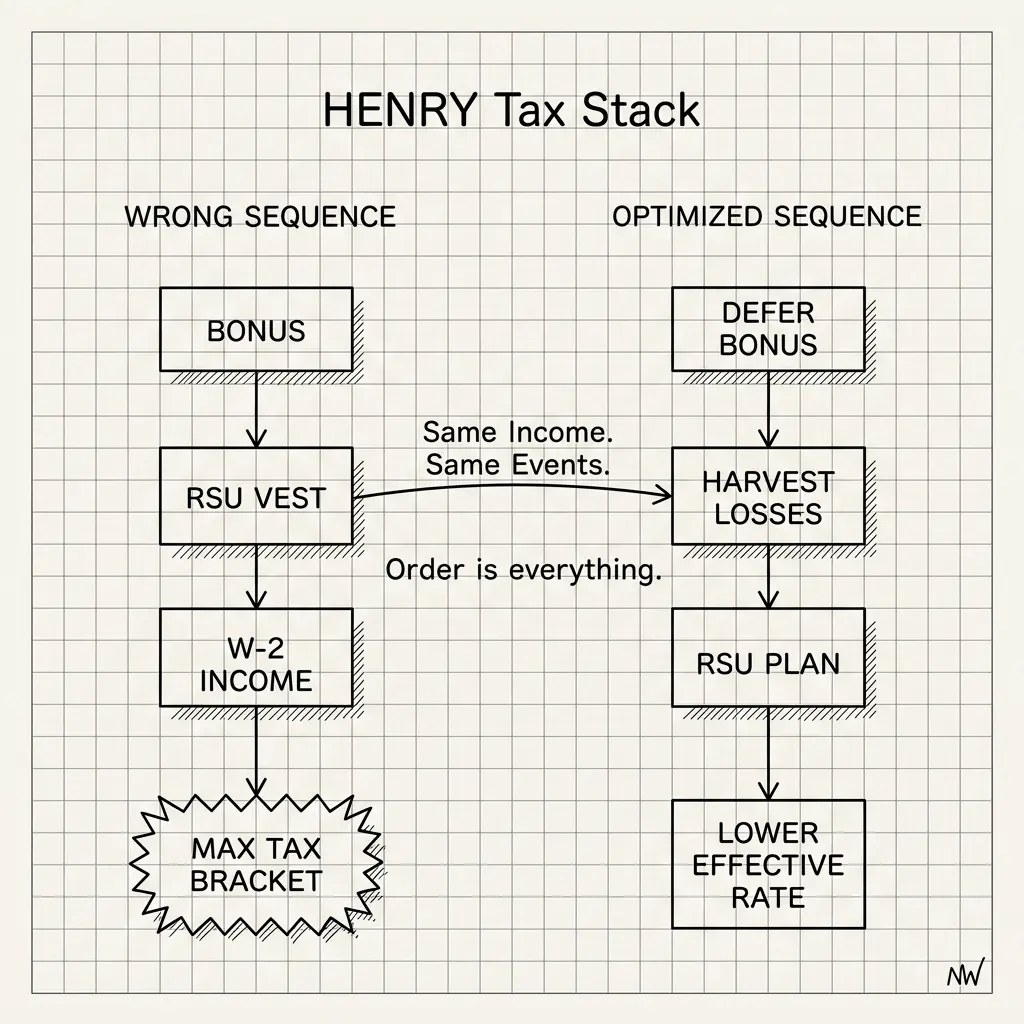

The High Earner Tax Stack

The ordered sequence of tax-advantaged moves every high earner should exhaust before touching taxable accounts.