NRI Tax Questions — Answered

Is NRE account interest taxable in the US?

Yes. NRE (Non-Resident External) account interest is tax-free in India under Indian income tax law. However, for US residents and citizens, interest income from NRE accounts is taxable in the US in the year it is earned. The Indian tax exemption has no effect on US tax obligations. Additionally, NRE accounts must be reported on FinCEN Form 114 (FBAR) if the aggregate balance of all foreign accounts exceeds $10,000 at any point during the calendar year. Most NRIs are unaware of this and have years of unreported NRE interest income.

Are Indian mutual funds PFICs for US tax purposes?

Yes. Indian mutual funds held by US residents are Passive Foreign Investment Companies (PFICs) under US tax law. PFIC treatment is punitive: gains are taxed at the highest ordinary income rate plus an interest charge on deferred taxes, rather than at favorable long-term capital gains rates. You have three elections (default, mark-to-market, or QEF), each with different implications. The QEF election requires annual information statements from the fund — which Indian mutual funds generally do not provide. Most cross-border CPAs recommend evaluating whether to liquidate Indian mutual fund positions before becoming a US resident, or shortly after. Form 8621 is required annually for each PFIC held.

What is the RNOR window and when should I plan for it?

RNOR (Resident but Not Ordinarily Resident) is an Indian income tax status that applies to most NRIs for 2-3 years after they return to India. During RNOR, foreign income — including US 401K distributions — may be exempt from Indian income tax. The US withholds 10% on 401K distributions to non-resident aliens under the US-India DTAA, and India does not additionally tax them during RNOR. This creates a window where 401K distributions are taxed at an effective rate of approximately 10%, compared to 30%+ after RNOR status expires. The RNOR window must be planned before you return: Roth conversions should happen while you are still a US resident, and distribution timing depends on knowing when your RNOR clock starts.

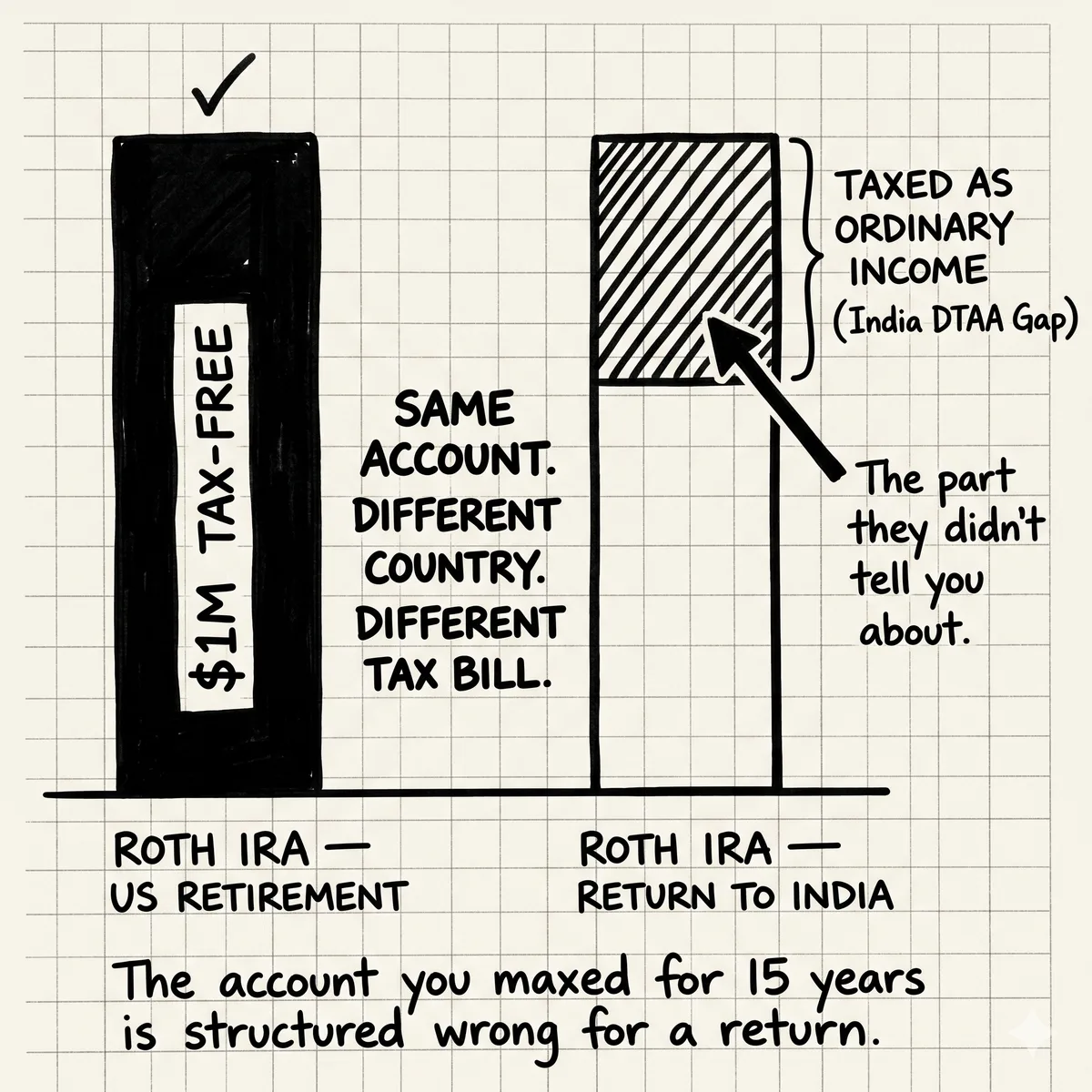

What is the best 401K strategy for H-1B holders who might return to India?

The 401K type decision (traditional vs. Roth) has a specific non-obvious answer for H-1B holders considering an India return. Traditional 401K distributions taken during the RNOR window are taxable only in the US at the 10% DTAA withholding rate — not additionally in India. Roth 401K and Roth IRA have no treaty protection in India; distributions may be taxable in India as ordinary income regardless of US tax-free status. For someone planning an India return, a traditional 401K maximized in the working years and distributed during the RNOR window after return is generally more tax-efficient than a Roth. The exception: if you're certain you will stay in the US permanently, the standard Roth optimization applies.

Do I need to report my EPF (Employees' Provident Fund) on my US tax return?

The IRS has not issued definitive guidance classifying EPF as a qualified pension plan exempt from annual reporting. The conservative position — taken by most cross-border tax professionals — is that interest accruing annually in your EPF account is US-taxable income in the year it accrues, even if you have not withdrawn any funds. EPF also counts toward FBAR reporting thresholds if combined with other foreign accounts. Additionally, EPF accounts may need to be listed on FATCA Form 8938 depending on your total foreign financial asset values. Most NRIs in the US have not been reporting EPF interest, creating potential unreported income exposure.

What happens to my RSUs if I leave the US before they fully vest?

RSU income is sourced to the workdays between the grant date and the vest date. If you move from the US to India mid-vesting-period, the US-sourced portion — calculated as US workdays divided by total vesting days — remains US-taxable regardless of where you live when the shares vest. Once you are a non-resident alien, your former US employer withholds at the non-resident alien rate (30%) on US-sourced RSU income, rather than at the graduated resident rate. The portion of RSU income sourced to India-workdays during the vesting period may be taxed by India under Indian income tax rules. Understanding your sourcing allocation before you leave the US allows you to plan your vesting decisions accordingly.