Burned Out at $400K With $2M in the Bank. What Would People Like You Actually Do?

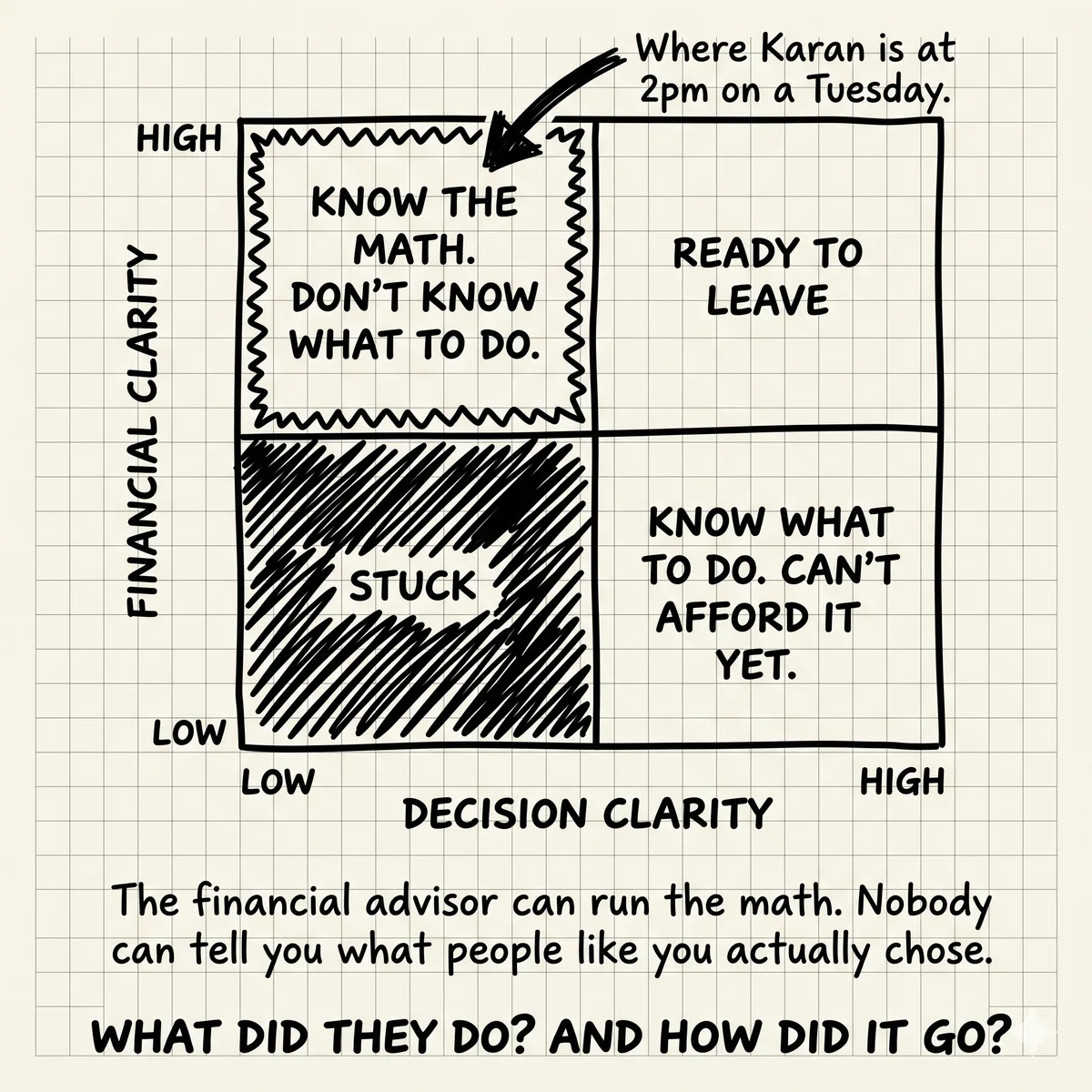

He sent the message at 2pm on a Tuesday. During work hours. Which already told you something.

Karan is 38. He earns $410K a year. He has $2.1M in the bank, spread across a brokerage account, two 401(k)s, and some RSUs that vested last spring. He hasn't taken a real vacation in two years. Not one where he actually disconnected. The last trip, he answered Slack from the beach in Tulum.

His message was short. "I'm done. But I don't know if I'm done-done or just burnt-out-and-need-a-month done. And I don't know anyone who's made this call who I can actually talk to about it."

Then the real question. "What do people like me actually do? And how does it go?"

He didn't want projections. He already had those. He wanted peer data.

The Math Is Not the Problem

By the time someone like Karan sends that message, they've already run the numbers. Multiple times. In multiple spreadsheets. They know the 4% rule. They've looked at their monthly burn. They've modeled a 20% market drop. They know what the portfolio looks like at 55, 60, 65 under different scenarios.

The math is not ambiguous for most people at this crossroads. $2.1M at 38, with no kids in college, a paid-off car, and a manageable mortgage, is enough to do something radically different. The portfolio doesn't care what Karan decides. It just grows or it doesn't.

What stops people isn't math. It's the absence of peer context. You don't know what the person who was in your exact situation actually chose. You don't know how they describe it eighteen months later. You don't know if the guy who took the severance is relieved or terrified. You don't know if the woman who downshifted to a lower-stress role regrets not going further.

The gap nobody talks about

Financial advisors can model your future. Reddit can give you raw anecdata. But nobody can show you a clean distribution of what people with your exact financial profile chose, and how each path played out. That's the information Karan actually needs.

What They Actually Want

Karan's question shows up in different forms across r/HENRYfinance and r/fatFIRE constantly. "Burned out at $400k — pushing for severance." "37, LOI in hand, struggling with the decision." "Two years of runway, two kids, can't tell if I'm being rational or just tired."

What people in these threads want isn't validation that the math works. They know the math works. What they want is a case file. Someone who was in roughly the same place, made a call, and lived to report back. They want the texture of what it was like. Did the anxiety go away? Did it change shape? Did they run out of things to do? Did the marriage get better or worse?

That's why the best Reddit threads on this topic aren't the math ones. They're the retrospective ones. The person who quit at 36 and is now writing at 39 about what actually happened. Those posts get 400 comments. People are starving for peer data.

The Three Paths

For someone at Karan's crossroads, there are really three distinct moves. Not variations on a spectrum. Three actual paths with different mechanics and different downstream effects.

Path 1: Severance and Reset

You negotiate a clean exit with severance, ideally 3-6 months. You take the time off without a plan. You let the decompression happen. You resist the urge to start something new for at least 90 days.

The people who describe this path a year later mostly say the first 30 days were harder than expected. The anxiety doesn't disappear. It changes form. Instead of "I have to respond to this Slack," it becomes "I should be doing something productive." That second anxiety is actually harder for high performers because there's no one to answer to.

But the people who got through that first 60 days mostly describe month three and beyond as a reset they didn't know they needed. Some found consulting work they actually liked. Some started something small. Some just took their family to Southeast Asia for a month and came back different.

Path 2: Downshift

This is the same company, a lower-stress role, a meaningful pay cut, or a move to a smaller company with less intensity. You keep the income but you dial back the pressure.

The honest Reddit read on this path: it works if the source of the burnout is workload. It doesn't work if the source is the industry, the type of work, or the fundamental mismatch between what you're doing and what you care about. People who downshift into the same kind of work at lower pay often find themselves back in the same place 18 months later, just with less money.

The downshift that works is usually a meaningful change in the nature of the work, not just the intensity. Moving from an IC role to an advisory role. Going from a 300-person company to a 40-person company. That kind of shift.

Path 3: Full Exit

You stop drawing a salary entirely. You live off the portfolio. You figure out what comes next from a position of no obligation.

At $2.1M and $410K income, this is a real option for Karan. His lifestyle floor is probably $120-150K a year. That's a 5.7-7.1% withdrawal rate on $2.1M, which is aggressive. But at 38, he has a lot of working runway. Even one consulting project a year changes the math dramatically.

The people who take this path and report back at 24 months break into two groups. The ones who had something to move toward — a project, a city, a person, a craft — mostly describe it as the best decision of their life. The ones who left without a toward destination often describe a 6-18 month period of directionlessness that was harder than the burnout.

The Real Question

The path matters less than what you're moving toward. The burnout data says: leaving toward something works. Leaving away from something transforms the anxiety but doesn't dissolve it.

What Reddit Actually Says

The r/fatFIRE "37, LOI in hand" thread is one of the more honest ones. The poster had $3.2M, a LOI for a VP role at a company he wasn't excited about, and a choice to make. Comments ran to 300+. The top-voted ones weren't about the math.

The ones that got the most engagement were from people who had been at similar crossroads and were writing about it years later. "I took the LOI and regret it three years later." "I passed and started consulting and the first year was scary but I'm a different person now." "I took 18 months off and then found something that actually fit."

The r/HENRYfinance burnout threads have a different character. These are people with more income and less accumulated wealth, often earlier in their career. The conversations there are less about "can I afford to leave" and more about "what is leaving going to cost me in terms of trajectory."

The honest pattern across both communities: people who waited until they were truly broken describe recovery taking longer. People who left while they still had something to give describe rebuilding faster. The "wait until you're sure" advice is probably backwards.

The Variables That Actually Determine the Outcome

The financial number isn't the primary variable. For people at Karan's level, the number is usually fine. The variables that actually determine how the transition goes are different.

Spouse income and alignment

If your spouse earns $180K and is fine with you stepping back, the risk profile changes completely. If your spouse is also burned out and you're the sole earner, a full exit is a different conversation. The joint income picture matters more than the portfolio number.

Health and time horizon

This one gets undersaid. The burnout threads with the most urgency are often from people who have started noticing physical symptoms. Sleep disruption, blood pressure, persistent illness. At that point, the calculus changes. The cost of staying gets real in ways the spreadsheet doesn't capture.

Illiquid assets

Pre-IPO equity, vesting schedules, deferred comp. Karan's $2.1M is mostly liquid. If 40% of his wealth was locked in unvested RSUs at a company he hated, the decision tree looks different. Knowing exactly what's liquid and what's locked changes the options available.

Identity

This is the hardest one to model. If your identity is tightly bound to your title and your comp, the first year of a full exit is harder than you expect. The people who navigate it best either had a prior identity outside their career, or found one quickly after leaving.

The burnout number post covers the math in more detail. The formula is cleaner than people expect. But the number alone doesn't tell you what to do with it.

Why Financial Advisors Can't Give You This

A good financial advisor can run the scenarios. They'll model path one, two, and three with different return assumptions, different withdrawal rates, different tax treatments. They'll show you a Monte Carlo simulation with 89% success on a 3.5% withdrawal rate over 50 years.

That's useful. That's not what Karan is asking for.

What Karan is asking for is: "Among the people who had $2M+ at 38, with a similar lifestyle, a similar job type, a similar family situation, what did they actually do? And how do they describe the decision in hindsight?"

No advisor has that data. Not for their individual client base. And even if they did, the incentive structure makes the advisor reluctant to share it. A client who exits the workforce at 38 with $2.1M and never touches the portfolio is a less valuable client than one who keeps earning, keeps contributing, and keeps growing AUM.

The advisor's model is projections. What Karan needs is peer data.

This connects to a bigger truth about wealth intelligence at this level. The quantitative picture is easier to get than ever. The peer picture is nearly impossible. That gap is where people get stuck. As I wrote in wealth bounded by physics, the constraint at Karan's level isn't mathematical. It's informational.

The Peer Data Problem

Here's what NettWorth is specifically being built to answer.

When Karan asks "what do people like me actually do," the honest answer today is: we don't have a clean way to show you. We have Reddit threads that are useful but not structured. We have advisor case studies that are curated and anonymous. We don't have a distribution of choices and outcomes for people who were in your specific financial situation.

The portfolio that changes this is a corpus of real decisions from people with real financial profiles. Not synthetic. Not fabricated. Real choices made by real people at real crossroads, with the financial context attached.

What the founding cohort of NettWorth users is building, by logging their financial situation honestly, is the peer data that the next Karan will actually be able to use. Not "here's what I project for you." Here's what people who were where you are actually chose.

That's a different kind of clarity. And it's the one that actually helps people like Karan decide, not just calculate.

On the income vs. wealth question

Karan's $2.1M and $410K income look like the same picture from the outside. They're not. The income is what keeps the lifestyle running. The wealth is what gives him the option. Understanding which one is doing which job is how you think clearly about this decision. The income vs. wealth guarantee framework is a useful lens here.

Karan sent that message at 2pm on a Tuesday. The message itself was the data. He's not undecided about whether he wants out. He's asking for permission. Not from you. From evidence that people like him made this call and it turned out okay.

That evidence exists. It's just not organized yet.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

You're Making $400K and You Still Don't Feel Wealthy. Here's Why the Benchmark Is Wrong, Not You.

Priya earns $420K in San Francisco, has $800K saved, and feels behind. She's comparing herself to HENRYfinance posters who have no parents to support, no cross-border obligations, no Bay Area cost structure. The benchmark is wrong, not her.

The Burnout Number: Calculating the Price of Your Freedom

You earn $350k a year, have $3M in the bank, but you are miserable. Here is the exact math to know if you can quit today.

You Can't Share This With Anyone Who Won't Make It Weird

You typed the text. Then deleted it. The people who most need peer context are the ones most isolated from it — family has baggage, friends have context mismatch, advisors have incentive misalignment. This is the problem NettWorth was built to solve.