Before You Leave the US for India: The RNOR Window, the 401K Decision, and Everything Else

Vikram knew about the RNOR window. He found out about it 14 months after he'd returned to Pune. The first two distributions from his 401K had already been taxed by India at his full marginal rate. The window had been open. He hadn't known what to do with it.

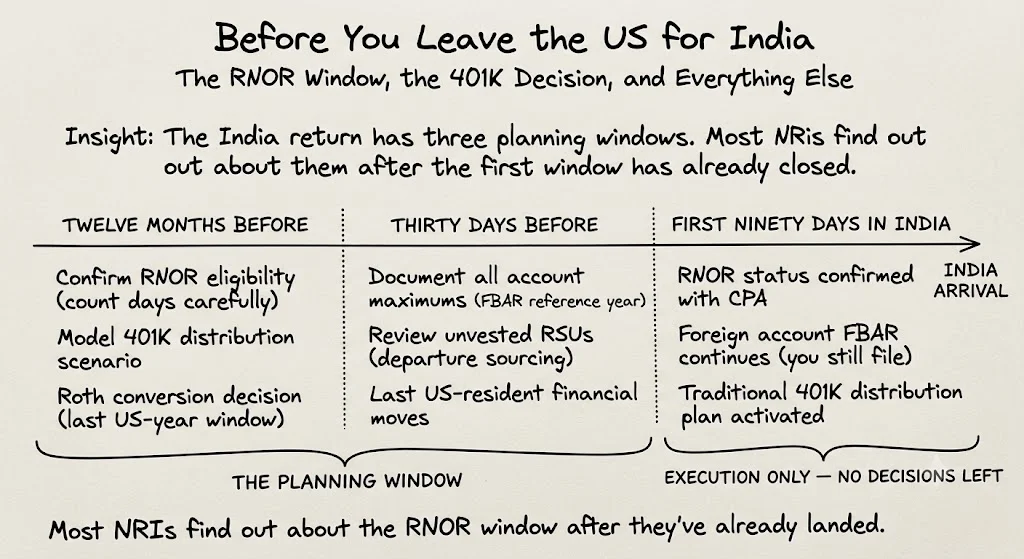

This checklist is for the version of Vikram who's still in the US, planning the return. The decisions below have deadlines. Some close before you board the flight. Most close when the RNOR window expires, which is 2 to 3 years after you arrive in India. The sequence matters.

The logistics of a return to India are mostly obvious. The financial picture is not. Here is what needs to happen, and when.

The RNOR window opens the day you land. It closes 2–3 years later. Everything builds toward maximizing what you can take during that window.

12 Months Before Departure

Calculate Your RNOR Window

The Resident but Not Ordinarily Resident (RNOR) status is the most valuable financial lever for returning H-1B holders. It is also the most misunderstood. Most returning NRIs either don't know about it or know about it too late to use it fully.

You qualify for RNOR if you've been a non-resident in India for 9 of the 10 years preceding the year you return. For most people who spent significant time in the US on H-1B, this test is satisfied. The window is 2 years. For those who've been abroad for 9 or more consecutive years, the window may extend to 3 years.

The window opens on the day you become an Indian resident again (the day you land with the intent to stay). It does not open retroactively. Days that pass before you understand the window are days you cannot recover.

What RNOR actually protects

During your RNOR period, India exempts foreign-source income from Indian income tax. This includes income earned outside India, income from a business controlled from outside India, and income from a profession set up outside India. A 401K distribution from a US account qualifies as foreign-source income. US interest and dividend income from a US brokerage account qualifies. The RNOR period is not a general tax holiday — Indian-source income (Indian salary, Indian dividends, Indian rental income) is fully taxable during RNOR.

Model Your 401K Distribution Strategy

Your RNOR window gives you a 2 to 3 year corridor where 401K distributions from the US are effectively taxed at 10% (the US treaty withholding rate under DTAA Article 20) and 0% in India. After the window closes, distributions are taxable at your Indian marginal rate, which for a 401K of meaningful size will likely be 30% plus cess.

The question to answer 12 months before departure: how much of your 401K can you realistically distribute during the RNOR window, and at what bracket? Taking $40,000 per year for 2 years clears $80,000 at 10%. Taking $80,000 per year may push you into higher India brackets even during RNOR if you have other India income sources. The right number depends on your total India income picture.

Model this now. Don't wait until you're in Pune and your CA asks why you didn't structure this before you left.

Decide on Roth: Convert Before You Leave, Not After

The US-India DTAA has no Roth provision. India taxes Roth distributions as ordinary income. If you have Roth balances, the tax-free treatment applies only in the US. Once you become an Indian resident, Roth distributions are taxable in India at your marginal rate.

This creates a specific window: if you want to do Roth conversions (converting traditional 401K to Roth), do them in the US, in a low-income year before departure. Any Roth balance you build in the US grows tax-free in the US. If India later taxes distributions, you've at least captured the tax-free growth period. That is better than doing the conversion in India, which serves no purpose.

If you're on track to leave in 12 months and your current year will have lower income than usual (stock market down, equity cliff not vesting, between jobs), this is the year to convert. The window closes when you return to India as a resident.

Decide on Unvested RSUs

Unvested RSUs that vest after you become a non-resident alien are subject to 30% US withholding (or the treaty-reduced rate, which is 15% for periodic income under the US-India treaty for most income types). This is significantly higher than the graduated rate you pay as a US resident.

The question: is it worth staying through the next vest date? Or negotiating an accelerated vest before departure? Or accepting the 30% withholding because the unvested amount is large enough that staying another 6 months is not worth it for other reasons?

This decision requires your actual unvested RSU schedule, your employer's willingness to accelerate, and your personal timeline. Make the decision with numbers, not assumptions.

30 Days Before Departure

Form 8854 If You're a Green Card Holder

If you're abandoning a green card (Lawful Permanent Resident status), you must file Form 8854 (Initial and Annual Expatriation Statement) with the IRS. This triggers the expatriation rules, which can include the exit tax if your net worth exceeds certain thresholds or if you've been a long-term resident.

A long-term resident is defined as someone who held the green card for 8 of the last 15 years. If you're in this category, the exit tax analysis is non-trivial and requires a cross-border CPA before departure, not after.

FBAR: Document Account Maximums for the Year

FBAR (FinCEN Form 114) requires reporting the maximum balance in each foreign financial account at any point during the calendar year. Your final FBAR as a US resident covers the entire calendar year of departure, including months you've already spent abroad if you were still a US resident for part of the year.

Document the maximum balance reached in each Indian account during the year. This includes NRE, NRO, Indian savings accounts, and any brokerage or mutual fund accounts with aggregate balance over $10,000 at any point.

If you're a US citizen (not just a green card holder or H-1B), FBAR continues to apply after you return to India. The obligation follows citizenship, not residence.

US Brokerage: Keep It Open, Don't Transfer

Keep your US brokerage account open after returning to India. Do not close it. Do not transfer assets to an Indian account or an Indian brokerage.

Indian mutual funds, Indian ETFs, and Indian fixed deposits held as a US person (if you retain US citizenship) create significant compliance complexity and often create PFIC exposure. Your US brokerage account, holding US-listed ETFs and individual stocks, has none of that complexity. Keep the US assets in US accounts.

Reactivate NRE/NRO Accounts

If your NRE or NRO accounts have been dormant during your US stay, reactivate them before departure. Upon returning to India as a resident, you will eventually need to convert NRE accounts to resident savings accounts (since NRE accounts are only for Non-Resident Indians, and your status in India will change from NRI to RNOR to ROR over time).

During RNOR, your NRI status in India is a specific transitional category. Your Indian bank needs to be informed of your return so they can manage account designations correctly.

First 90 Days in India

Confirm RNOR Status With Your Indian CA

Your Indian Chartered Accountant needs to determine your RNOR status for the first Indian tax year after your return. This is not automatic. The CA must calculate it based on your years abroad and residency history.

The RNOR status is reported on your Indian income tax return. If your CA files you as an ordinary resident instead of RNOR, you will pay Indian tax on foreign income that should be exempt. This is a filing error with a material cost. Confirm the status explicitly with your CA before your first return is filed.

Begin 401K Distributions

Once RNOR status is confirmed, begin 401K distributions at the rate you modeled before departure. The US will withhold 10% under the treaty. Your Indian CA should file the Indian return showing these as exempt foreign-source income during RNOR.

Do not delay. Every month inside the RNOR window where you don't take distributions is a month of 10% tax rate left unused. The window does not extend. It does not pause. When it expires, it expires.

US Tax Filing Continues

If you're a US citizen, you continue to file a 1040 from India. Worldwide income basis applies to US citizens regardless of residence. Your US return will report 401K distributions (even though India is your primary residence), US brokerage income, and any other US-source income.

If you abandoned your green card and are now a non-resident alien, you file a 1040-NR covering US-source income only. The 401K distributions you take will appear on this return.

The Vikram scenario, replayed correctly

If Vikram had known 12 months before departure: he would have modeled $35,000 per year in 401K distributions during a 2-year RNOR window. He had $340,000 in traditional 401K. At $35,000 per year for 2 years, he clears $70,000 at approximately 10% effective tax. The remaining $270,000 stays invested and grows. He's not locked into India's 30% rate until he's drawn the $70,000 at the discounted rate.

Instead: he took two distributions without knowing about RNOR, paid India's marginal rate on both, and found out about the window 14 months after it opened. He still has his remaining window. But the first two distributions are gone.

Related Reading

- Traditional 401K or Roth 401K When You Might Move Back to India? The Math Most H-1B Holders Never See

- The RNOR Window: Why Your First 2–3 Years Back in India Are Your Most Valuable

- Green Card Exit Tax When Returning to India: What Triggers It and What Doesn't

- The H-1B Financial Playbook: What the Tax Firms Cover and What They Leave Out

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

You're Returning to India. Your RNOR Window Is Open. Here Is the Exact Sequence of Decisions.

Sunita returned to Bengaluru and knew about the RNOR window. Her CA explained the sequencing options. She had all the information. Nobody had synthesized it into a sequence. The difference between taking 401K distributions during RNOR versus after: 10% effective rate versus 30%+. On $200K of distributions, that's $40,000.

Before You Leave the US for the UK: The Financial Checklist (Not the One About What to Pack)

Claire moved to London meticulous about logistics. Six weeks in, she found out she'd missed the UK's Foreign Income and Gains election window — the one that exempts US portfolio income from UK tax for up to four years. The window is 30 days from arrival. This is the checklist organized by deadline.

Leaving the US for the UK: The Financial Decisions That Have Hard Deadlines Before Your Flight

Olivia landed in London on a Sunday and started work on Monday. Week seven: she found out about the UK's Foreign Income and Gains regime — introduced April 2025, exempts foreign income from UK tax for four years, must be elected in the first UK tax year. She'd missed the 30-day window by five weeks. This is what she should have known before she boarded the flight.