Traditional 401K or Roth 401K When You Might Move Back to India? The Math Most H-1B Holders Never See

Seven years of maxing out a 401K. One conversation with a colleague. And the realization that she'd built her retirement assumptions on something she'd never actually read.

Meera had been doing everything right. Senior engineer at a cloud infrastructure company, seven years in the Bay Area on an H-1B. She maxed her 401K every year without thinking about it. Her company matched 4%. Her financial picture felt clean.

Then she had lunch with a colleague who'd just come back from a meeting with a cross-border CPA. The colleague mentioned something in passing: "Did you know India taxes your 401K distributions as ordinary income?"

Meera said she'd assumed the US-India tax treaty covered it. The colleague nodded. "It does. But not the way you think."

That evening, Meera sat with the actual text of the treaty. She had a law degree from India. She could read it. Article 20. Pensions and annuities. She read it three times. The treaty gives India the right to tax retirement income of Indian residents. The US doesn't tax you twice. But India taxes you once. At the marginal rate.

Seven years of contributions. Three possible futures (stay in the US, return in five years, return in fifteen). And she'd never modeled any of them with actual India tax rates. She'd assumed the treaty made it work out. It does prevent double taxation. It doesn't prevent Indian taxation.

The 401K decision for H-1B holders who might return to India is not complicated once you understand it. But understanding it requires reading one treaty article, running one set of numbers, and asking one question you've probably never been asked to ask.

What Article 20 Actually Says

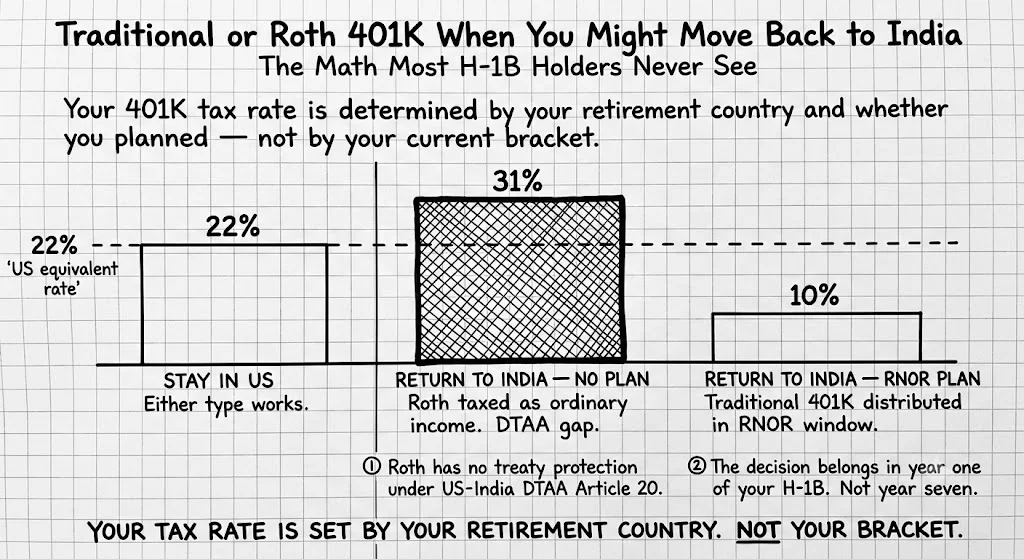

The US-India Double Taxation Avoidance Agreement (DTAA), Article 20, covers pensions and annuities. The structure is straightforward: the country of residence has the primary right to tax pension income. For an Indian resident receiving 401K distributions, India has the right to tax those distributions as ordinary income.

The US also has the right to tax distributions from 401K plans, but the treaty prevents double taxation. In practice: you pay one, not both. If you're resident in India, India taxes the distribution. The US withholds 10% under the treaty (the reduced withholding rate for pension income). You claim a credit in India for the US withholding. India taxes you at your marginal rate, minus the 10% US credit.

If your Indian marginal rate is 30% (the top rate for income above approximately INR 15 lakh), you effectively pay 30% on distributions. The US withholds 10%. India takes the remaining 20%. Your effective rate is 30%.

The math on India's top marginal rate

India's highest income tax bracket (income above approximately INR 50 lakh) carries a 30% base rate plus surcharges, plus a 4% health and education cess. The effective top marginal rate is approximately 42.7% at the highest surcharge levels. Even at the base bracket (INR 15 lakh to 50 lakh), you're looking at 30% plus 4% cess. For most returning H-1B holders with a 401K built on US tech salaries, distributions will push well into the top bracket.

The treaty is working as designed. It prevents you from paying both US and Indian tax. What it cannot do is reduce the tax India levies on your income as an Indian resident. That rate is India's to set, not the treaty's to cap.

The Math on a Traditional 401K When You Retire in India

The case for a traditional 401K rests on a single premise: you'll be taxed at a lower rate when you withdraw than when you contributed. If that's true, tax deferral wins. If it's not true, you've deferred a tax bill and paid the carry cost in exchange for nothing.

Most H-1B holders at US tech companies are contributing at a 32% or 37% federal marginal rate. The case for traditional is: retire at a lower rate, pocket the difference. If you retire in the US, this logic holds for most people. The US rate at retirement, for a moderate distribution level, is likely 22% to 24%. The deferral wins.

If you retire in India with the same 401K, you're distributing at the Indian marginal rate. That rate for a 401K of meaningful size is 30% plus cess, effectively 31.2% at the base top bracket. If you contributed at 32% to 37% and withdraw at 31.2%, you've captured a small deferral advantage and nothing more. The decades of tax-deferred compounding help, but the rate differential you built the strategy on is much smaller than it looked in year one.

The employer match complicates this in a good way. Take the match. Always take the match. That's a 4% to 6% return before the money is invested in anything. No rate differential can eliminate that. The question is whether to contribute beyond the match, and at what rate, given an uncertain retirement location.

A rough scenario: $500K traditional 401K, retiring in India

This is for illustration. Actual India tax depends on your total India income including other sources. Surcharges increase the rate for income above INR 50 lakh equivalent.

Whether this is better or worse than alternatives depends on your specific income level and India tax bracket. What it is not is the clean win that "max your 401K" implies.

The Roth Problem: Why the "Smart" Move Is Actually Worse

The natural follow-on question is: if traditional 401K loses some of its advantage for India returnees, doesn't that make Roth 401K better? You've already paid US tax on contributions. Withdrawals are US-tax-free. You escape the India tax problem.

This is the intuition. The treaty does not support it.

India does not recognize Roth accounts as tax-exempt. The US-India DTAA has no Roth provision. From India's perspective, a Roth 401K distribution is ordinary income, subject to Indian income tax at your marginal rate. The Indian government did not agree to exempt income streams that the US happens to have labeled "Roth."

The outcome: with a Roth 401K and retirement in India, you've paid US income tax on contributions and you'll pay Indian income tax on distributions. The treaty prevents the US from also taxing the distributions (they're already post-tax in the US). But India taxes the whole amount. You've effectively been taxed twice: once in the US on the way in, once in India on the way out.

With a traditional 401K and retirement in India, you pay India tax on the way out. One time. At your Indian marginal rate, with a 10% US withholding credit.

Roth IRA has the same problem

The Roth IRA is subject to the same treaty gap. India does not recognize Roth IRA withdrawals as US-tax-free income that should be exempt from Indian tax. If you return to India with a Roth IRA balance, distributions will be treated as ordinary income for Indian tax purposes. The tax-free growth you accumulated in the US is not protected by treaty when you become an Indian resident. The Roth IRA is an excellent vehicle if you stay in the US. It is not an efficient vehicle if India is your retirement country.

The standard financial planning advice (max your traditional 401K if you're in a high bracket now, consider Roth if you expect higher rates later) is built for US-resident retirees. For H-1B holders with genuine India return uncertainty, both options have complications. Neither is cleanly optimal without knowing your retirement country.

The RNOR Window: The Only Path to a Low-Rate 401K Distribution

There is one scenario where 401K distributions from India land at a significantly lower tax rate than either analysis above suggests. It requires planning, advance notice of your return, and a specific status that lasts 2 to 3 years.

When you return to India after an extended stay abroad, you qualify for Resident but Not Ordinarily Resident (RNOR) status for a period defined by how long you've been abroad. For most H-1B holders who've been in the US for 9 or more of the last 10 years, this window is 2 years. For very long-term US residents (over 9 consecutive years abroad), it can be 3 years.

During the RNOR period, Indian income tax law exempts foreign-source income and income from a business or profession not controlled from India. A 401K distribution from a US retirement account, held at a US financial institution, qualifies as foreign-source income. Under the current interpretation of Indian tax law, 401K distributions taken during your RNOR window are not taxable in India.

The US will still withhold 10% under the DTAA treaty rate. That 10% is your final tax on those distributions. Not 30%. Not 31.2%. Ten percent.

The RNOR calculation: do you qualify?

You qualify for RNOR if you've been a non-resident (NRI) for 9 of the last 10 years before the year you return, OR if your total stay in India in the 7 years before the year you return has been 729 days or less. Most H-1B holders who've spent significant time in the US will qualify on the first test. The RNOR status lasts for 2 to 3 years depending on your specific residency history.

The clock starts from the date you return to India as a resident, not from the date you leave the US. Your Indian CA needs to confirm the status on your first Indian tax return after return.

The strategic implication: if you have a large traditional 401K and you're planning to return to India, the RNOR window is the most valuable planning lever you have. Maximize distributions during the window. That means planning years before you leave, not after you arrive.

The RNOR window closes. After it expires, you're an Ordinary Resident. Distributions return to Indian marginal rate taxation. Whatever 401K balance remains at the end of year 2 or 3 becomes subject to full Indian tax for the rest of your retirement.

The Decision Framework: Three Paths

The right strategy depends on your honest answer to one question: where do you expect to retire? Not "where might you retire" or "where would be nice to retire." Your working assumption, today, based on what you know.

The treaty prevents double taxation. It does not prevent Indian taxation. The RNOR window is the only path to a substantially lower rate.

Path 1: You're Staying in the US Permanently

If you have genuine permanence (green card, naturalization underway, family anchored in the US, career fully US-based), standard 401K advice applies. Maximize traditional if you're in a high bracket now. Add Roth contributions or conversions if you want tax diversification in retirement. The India treaty analysis is not relevant to your situation.

Take the employer match. Max the 401K if your income supports it. Consider a backdoor Roth IRA for additional tax-free growth. The standard playbook is right for you.

Path 2: You Might Return in 0 to 5 Years

This is the hardest path because it requires the most deliberate action right now.

Take the employer match. That is always worth doing. Beyond the match, think carefully before maximizing contributions to a traditional 401K. You're contributing at a 32% to 37% US marginal rate today. If you return to India in three years and immediately start drawing, you'll pay 30%-plus Indian marginal rate. The deferral benefit on contributions above the match is small.

Do not build a large Roth 401K or Roth IRA balance. The treaty gives you no protection when you become an Indian resident.

Instead: consider building taxable brokerage assets. Long-term capital gains from a US brokerage account are more flexible than retirement accounts when you leave. You're not locked into distribution rules. You can structure sales to manage India tax. You have more options.

Also: if you know you're returning in 0 to 5 years, start planning your RNOR window now. How long will your window be? How much can you realistically withdraw per year without exceeding India's lower tax brackets? A two-year window at $40,000 per year clears $80,000 at 10% tax. That math changes what you should be doing today.

Path 3: You Might Return in 6 to 15 Years

The longer time horizon gives you more flexibility. Continue contributing to the traditional 401K. The tax-deferred compounding over 6 to 15 years adds meaningful value even if the eventual tax rate in India is comparable to your current US rate.

Do not build a large Roth balance with the intent to retire in India. If you do Roth conversions, do them in low-income years (sabbatical years, low-equity years) and size them so you can actually retire in India if you choose, not so that the Roth assumption locks you into a US retirement.

Start modeling your RNOR window 3 to 5 years before you plan to return. The calculation is straightforward but requires knowing your 401K balance at return time, your expected India income from other sources, and India's bracket structure at that time. A cross-border CPA should run this for you 18 to 24 months before departure.

Two More Things That Affect the Math

The Roth Conversion Before Departure

One move that actually does help India returnees: a Roth conversion done before you return to India, in a low-income US tax year, for an amount sized to stay in a reasonable US bracket.

Here's why this works: the Roth conversion happens while you're a US resident. You pay US income tax on the converted amount. The converted amount grows tax-free in the Roth account. If you later return to India and India taxes Roth distributions as ordinary income, you're paying Indian tax on the converted amount. But the growth that occurred after the conversion (potentially years of compounding) was not subject to US tax, and India taxes only the distribution, not separately the growth.

For a conversion done in a year when your US taxable income is low (career transition, sabbatical, deliberate income reduction before departure), the US tax on conversion may be 22% to 24%. If India then taxes distributions at 30%, you've paid 22% on the base and 30% on what comes out later. That sounds bad, but the alternative (traditional 401K taxed entirely in India at 30%) may be worse if the Roth had more decades to grow.

The Roth conversion before departure is not a magic answer. It's a lever that needs to be modeled for your specific situation. The window is: any low-income year before you return to India.

The Early Withdrawal Penalty If You Leave Before 59.5

H-1B holders who return to India before age 59.5 face a potential 10% early withdrawal penalty on 401K distributions. The 10% is in addition to income tax (US withholding plus India marginal rate).

There is a partial exception: the "substantially equal periodic payments" rule (Section 72(t)) allows penalty-free distributions if you take distributions in equal annual amounts calculated by your life expectancy. This requires specific calculations and a commitment to the schedule. If you break the schedule, the IRS retroactively applies the penalty to all prior distributions. It is not a casual strategy.

For most H-1B holders returning to India before 59.5 with meaningful 401K balances, the RNOR window strategy is superior to trying to access the 401K early. Take less in the first 2 to 3 years (maximizing the 10% treaty rate), and leave the remainder to grow until 59.5 when distributions are penalty-free.

What Meera Did

Meera had two years before her planned return. She'd been contributing $23,500 per year to a traditional 401K (the 2026 maximum) plus employer match. She had $410,000 accumulated.

She ran the math. Her RNOR window would be 2 years. At $40,000 per year in distributions, she could clear $80,000 at approximately 10% tax rate. After that, her 401K balance would still be $330,000 and growing, subject to full India tax when she drew from it after the RNOR window closed.

She stopped contributing above the employer match. She shifted the additional savings to a taxable brokerage account. She scheduled a Roth conversion for the year she planned to take unpaid leave before her return, when her income would drop. And she started tracking what her India income from other sources would be, to know whether the top bracket was realistic or whether she could manage distributions to stay in a lower bracket.

None of this required a revolutionary move. It required knowing what Article 20 said and asking what that meant for her.

Her CPA had never brought it up. Not once in seven years. His job was to file her return correctly. What to contribute and where was not in his scope.

Before acting on this analysis

The RNOR window calculation, the treaty application, and the India tax bracket math all depend on your specific situation: years of US residency, expected India income from other sources, and your 401K balance at the time of return. A cross-border CPA who knows both US and Indian tax (not just one side) should model your specific path before you make any changes to your contribution strategy. The framework here is yours to understand. The numbers for your situation are for a professional who knows both sides.

Related Reading

- The H-1B Financial Playbook: What the Tax Firms Cover and What They Leave Out

- The RNOR Window: Why Your First 2–3 Years Back in India Are Your Most Valuable

- The Roth IRA Trap for NRIs: Why the Tax-Free Account Has an India Problem

- Before You Leave the US for India: The Financial Checklist

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

NRE and NRO Accounts: What Changes the Day You Become a US Tax Resident

NRE interest is tax-free in India. The day you become a US tax resident, it becomes US taxable income at ordinary rates — and most NRIs find out two or three years late. NRO interest has a different problem: 30% TDS generates a Foreign Tax Credit, but the credit math depends on your US bracket. FBAR applies to both accounts from year one. The gap exists because the Indian CA says 'tax-free' and the US CPA never asks.

Before You Move to the US from India: The Financial Checklist Your CPA Won't Give You

Preethi kept her NRE account when she moved to San Jose — her Indian CA said it was tax-free. It is, in India. From the day she became a US resident alien, the interest was US income. Three decisions have hard deadlines before your flight: your Indian mutual funds (likely PFICs the moment you land), your PPF contribution strategy, and the Roth vs. Traditional 401K choice that has a specific non-obvious answer if you might ever return to India.

Before You Leave the US for Singapore: What FEIE Doesn't Cover and What You Need to Do

Jason took the Singapore role thinking he'd finally escape US tax on investment gains. Singapore has no capital gains tax. He assumed his RSUs would be covered by the Foreign Earned Income Exclusion. His US CPA: RSUs are compensation, not foreign earned income. FEIE doesn't apply. You owe US ordinary income tax on every vest.