NRE and NRO Accounts: What Changes the Day You Become a US Tax Resident

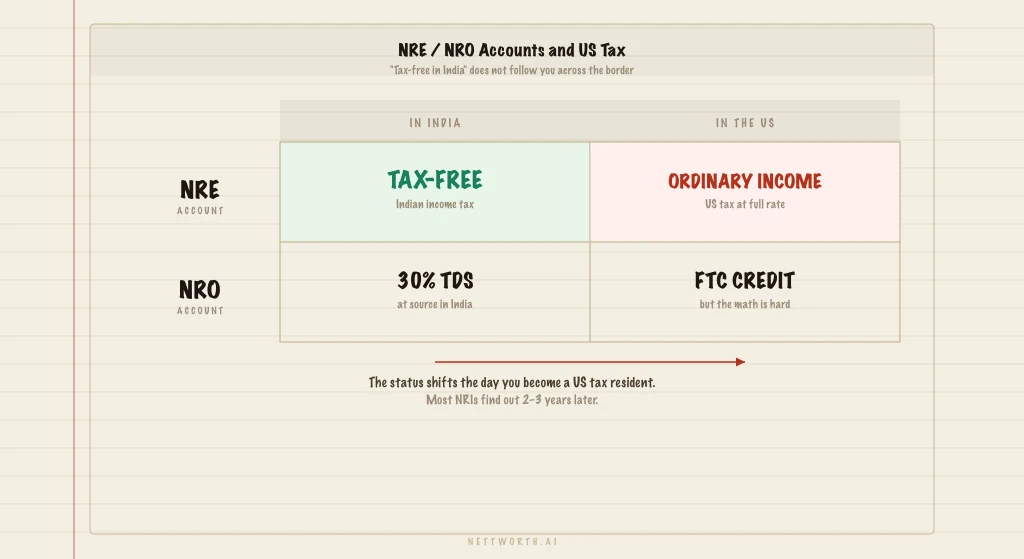

The NRE account's tax-free status applies to Indian income tax. It does not follow you to the US. The day you become a US tax resident, NRE interest becomes US taxable income — and most people find out two or three years late.

Priya had been on an H-1B for two years. She was diligent about her taxes. She filed a 1040 every year. She used a CPA. She never reported NRE account interest because her bank in India called it "tax-free interest" and she assumed that applied everywhere. Her US CPA had never asked about it specifically.

In year three, she switched CPAs. The new one asked about foreign accounts. She listed her NRE account. He asked about the annual interest. She showed him the amount — roughly $4,200 annually from the NRE fixed deposits her family had structured before she left India. He told her it should have been reported as ordinary income on her US returns since the first year she met the substantial presence test. Three years of unreported income. An amended return situation.

This is the most common NRI tax mistake in the India-US corridor. Not a complicated mistake. Not a gray area. A gap that exists because the Indian CA says "tax-free" and the US CPA never asks.

NRE and NRO: What They Are

NRE (Non-Resident External) accounts are Indian bank accounts designed for NRIs to hold and manage foreign earnings in India. The key features: the principal and interest are fully repatriable (you can move the money out of India without RBI approval). Interest is exempt from Indian income tax. The account is denominated in Indian rupees but funded from foreign currency conversions.

NRO (Non-Resident Ordinary) accounts hold income earned in India — rental income, dividends from Indian investments, proceeds from the sale of Indian property. NRO interest is taxable in India at 30% (TDS is deducted at source). Repatriation from NRO accounts is subject to annual limits (currently $1 million per financial year, with documentation).

The Indian tax treatment is exactly what the bank and your Indian CA tell you: NRE interest is tax-free in India. NRO interest is subject to 30% TDS. This is accurate and complete — for Indian tax purposes.

What Changes on the Day You Become a US Tax Resident

The substantial presence test determines when you become a US tax resident. If you are present in the US for 31 or more days during the current year, and 183 or more days counting all days in the current year plus one-third of days in the prior year plus one-sixth of days in the year before that — you are a US tax resident for that calendar year.

For most H-1B holders who arrive in the US in the first half of the year, the substantial presence test is met during the first calendar year. For those who arrive mid-year or late in the year, the test may not be met until the second year. Your dual-status year (the year you transition from non-resident to resident) is particularly complex.

From the first day you are a US tax resident, US worldwide income tax applies to all income, regardless of source or country. NRE interest, which was tax-free in India, is now foreign interest income subject to US income tax at ordinary income rates. The Indian tax-free status is an Indian rule. It doesn't cross borders.

The practical consequence

An NRE fixed deposit earning 7.5% on ₹50 lakhs generates approximately ₹3.75 lakhs (~$4,500 at current exchange rates) in annual interest. Every rupee of that is US-taxable as ordinary income from the year you become a US tax resident. At a 24% marginal federal rate, that's about $1,080 in additional US tax per year. Over three years, $3,240 — plus interest and potential penalties if the income was not reported.

NRO Interest: The Flip Side

NRO interest has a different structure. India taxes it at 30% TDS. The US also taxes it as ordinary income. This appears to be double taxation — and structurally, it is. But the Foreign Tax Credit (Form 1116) provides the mechanism for relief.

The Indian TDS of 30% on NRO interest generates a foreign tax credit you can apply against your US liability on that same income. If your US marginal rate is 24%, the Indian 30% TDS exceeds your US liability, which means the NRO interest may generate zero additional US tax and may even produce excess credits. The excess credit can be carried forward or back under the FTC rules.

The catch: if your NRO account has TDS deducted at 30% but you are only in the 22% US bracket, the FTC fully covers your US liability on that income. If you are in the 37% US bracket, the FTC covers 30% and you owe the remaining 7% to the US after the credit.

The NRO interest must still be reported on your US return. The FTC is not automatic — it requires Form 1116 and accurate documentation of the Indian tax paid (your bank's TDS certificate, Form 16A in India).

FBAR Obligations: Both Accounts

Both NRE and NRO accounts are foreign financial accounts subject to FBAR reporting. If the aggregate balance of all your foreign financial accounts (NRE, NRO, EPF, PPF, savings accounts, fixed deposits, mutual funds held in demat form) exceeds $10,000 at any point during the calendar year, you file FinCEN Form 114 by April 15 (with an automatic extension to October 15).

The FBAR threshold is aggregate, not per-account. If you have three accounts — NRE at ₹8 lakhs, NRO at ₹4 lakhs, and an Indian savings account at ₹2 lakhs — the aggregate in USD likely exceeds $10,000. FBAR applies. Each account is listed separately on the form.

Penalties for non-willful failure to file FBAR start at $10,000 per account per year. For Priya's two accounts over three years of non-filing, that's potentially $60,000 in penalties before the IRS even looks at the underlying tax. The Streamlined Filing Compliance Procedure is available for taxpayers who were non-willfully non-compliant — which covers most NRIs who simply didn't know. The Streamlined process reduces the penalty structure significantly, but it still requires amended returns and penalty payments.

FBAR vs. Form 8938 (FATCA)

Both FBAR and Form 8938 may apply to your NRE and NRO accounts. FBAR (FinCEN 114) is filed separately from your tax return with FinCEN, with a $10,000 aggregate threshold. Form 8938 is filed with your 1040 with higher thresholds ($50,000 on the last day of the year or $75,000 at any point, for single filers in the US). Both can apply to the same accounts, both have separate penalties, and missing either is a separate violation. Your CPA needs to be aware of both obligations.

What to Do Before You Leave India

The NRE account structure decisions are most efficient when made before you trigger US tax residency. Once you're a US resident, you can restructure, but you're paying US tax on the income during any transition period. The decisions to evaluate before departure:

Evaluate whether to continue holding NRE fixed deposits. If you have substantial NRE fixed deposits earning 7–8% annually, the interest will be US-taxable from year one. At US marginal rates of 22–37%, this reduces the effective yield meaningfully. The question is whether you need the liquidity in India or whether the capital could be deployed into US investments with more tax-efficient treatment.

Consider converting some NRE to FCNR(B) deposits. Foreign Currency Non-Resident (Bank) deposits hold money in foreign currency (USD, GBP, EUR) rather than INR. FCNR interest is also tax-free in India, and also US-taxable — but FCNR eliminates the currency risk on the Indian-side deposit. Whether FCNR makes sense depends on your view of INR/USD and your intention to eventually repatriate.

Establish your FBAR baseline. Before the day you become a US tax resident, document the account balances. Your FBAR for the year of arrival covers the period from when you became a US resident — you need the starting balances to accurately report the high-water mark during the year.

Liquidate Indian mutual funds if they are PFICs. Virtually all Indian mutual funds are PFICs for US tax purposes. Liquidating before triggering US tax residency avoids the punitive PFIC tax treatment. The decision window is narrow — and closing it by acting while you're still in India is far easier than navigating a PFIC cleanup from the US side.

After You Arrive: The First Filing Year

Your first US tax year may be a dual-status year if you didn't arrive on January 1. Dual-status means part of the year you were a non-resident alien and part of the year you were a resident alien. The rules for what income is reportable differ between the two periods. This is a complicated return. Most CPAs who specialize in Indian-US cross-border taxes have handled them; most general-practice CPAs have not.

For NRE interest: report it for the period of the year during which you were a US tax resident. If you became a resident on May 1, you report NRE interest from May 1 through December 31. The pre-residency period NRE interest is not US-taxable.

For FBAR: even if you only became a US resident partway through the year, you file FBAR for the full year if you met the threshold at any point during your residency period. The FBAR covers "any time during the calendar year" — which includes the months you were already a resident.

Going forward: every year you file a 1040, you report NRE interest as foreign interest income on Schedule B. You file FBAR if your aggregate foreign account balances exceeded $10,000 at any point. You file Form 8938 if your specified foreign financial assets exceeded the applicable threshold. These are annual obligations, not one-time events.

The full framework — 401K traditional vs. Roth decision for H-1B holders with uncertain India timelines, PFIC exposure on Indian mutual funds, and the first-year filing decisions — is in the H-1B financial playbook. For NRIs beginning the return to India, the financial checklist for leaving the US for India covers the RNOR window sequencing and the 401K distribution strategy.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

Traditional 401K or Roth 401K When You Might Move Back to India? The Math Most H-1B Holders Never See

Meera maxed her 401K every year for seven years. Then a colleague mentioned something: India taxes 401K distributions as ordinary income. She'd assumed the tax treaty covered it. It does — but not the way she thought. The treaty prevents double taxation. It doesn't prevent Indian taxation. And Roth 401K is worse.

Before You Move to the US from India: The Financial Checklist Your CPA Won't Give You

Preethi kept her NRE account when she moved to San Jose — her Indian CA said it was tax-free. It is, in India. From the day she became a US resident alien, the interest was US income. Three decisions have hard deadlines before your flight: your Indian mutual funds (likely PFICs the moment you land), your PPF contribution strategy, and the Roth vs. Traditional 401K choice that has a specific non-obvious answer if you might ever return to India.

Before You Move to the US from Europe: The Financial Checklist for German, Dutch, and French Professionals

Thomas had been contributing to his German bAV for nine years. His cross-border accountant explained: Germany's pension tax deferral is a German decision. The US didn't agree to it. His employer's contributions were still taxable US income in the year contributed. Three countries, one checklist.