The 15-Year Tax Setup I Wish Someone Had Told Me

I pulled up my 2009 W-2 not to look at the number. I knew the number. I pulled it up to look at the decisions I hadn't made yet. The ones that would cost me for the next fifteen years.

I came to the US in 2008 on an H-1B. I had a good salary for a first job. Not extraordinary, but solid. I opened a checking account. I enrolled in the 401(k) because HR said to. I filed my taxes in April using TurboTax. I thought I was doing it right.

I wasn't doing it wrong exactly. I wasn't breaking any rules. But I was making a series of choices, many of them by default, that locked in a tax structure I'd be living inside for the next two decades. Each choice was small. Together they cost me hundreds of thousands of dollars in tax that I didn't need to pay.

The wrong account type. The wrong entity structure when I started consulting on the side in year three. The wrong residency classification for some of my investments. The wrong timing on my first equity exercises. None of it was illegal. All of it was expensive.

The thing that stings isn't the money. It's the fixability. Every one of those decisions had an alternative that would have been better. The information existed. I just didn't have access to it in year one, year two, year three, when it would have mattered.

If I had known in 2009 what I know now, I would have been poorer in years 1-3. But I would have had more money to invest, and it would have grown faster. The gap over fifteen years is not theoretical.

Why Tax Architecture Matters More Than Tax Filing

Most people think about taxes as a filing problem. Every April, you gather documents, enter numbers, and submit a return. Maybe you pay a CPA to do it. The goal is accuracy and compliance. That's tax filing.

Tax architecture is different. It's the set of structural decisions you make in advance that determine how much you'll owe when April comes. The accounts you open. The entity you use. The timing of your income. The classification of your investments. The state you live in. These decisions are made months or years before the tax return is ever filed. By the time the return is due, most of the outcome is already locked.

A CPA filing your return is an excellent practitioner of tax compliance. Most CPAs are not in the business of building 20-year tax architecture. The conversation with your CPA in March is about last year's situation. The conversation that would have helped you most was the one you didn't have in year one about the next 20 years.

The practitioner gap

CPAs are trained and incentivized to file accurate returns. Tax attorneys structure specific transactions. Financial planners model retirement scenarios. Nobody sits with a 28-year-old immigrant in year one and says: "Here are the five decisions you need to make in the next 24 months that will determine your tax bill for the next two decades." That conversation doesn't happen. Not because it's not valuable. Because nobody's paid to have it.

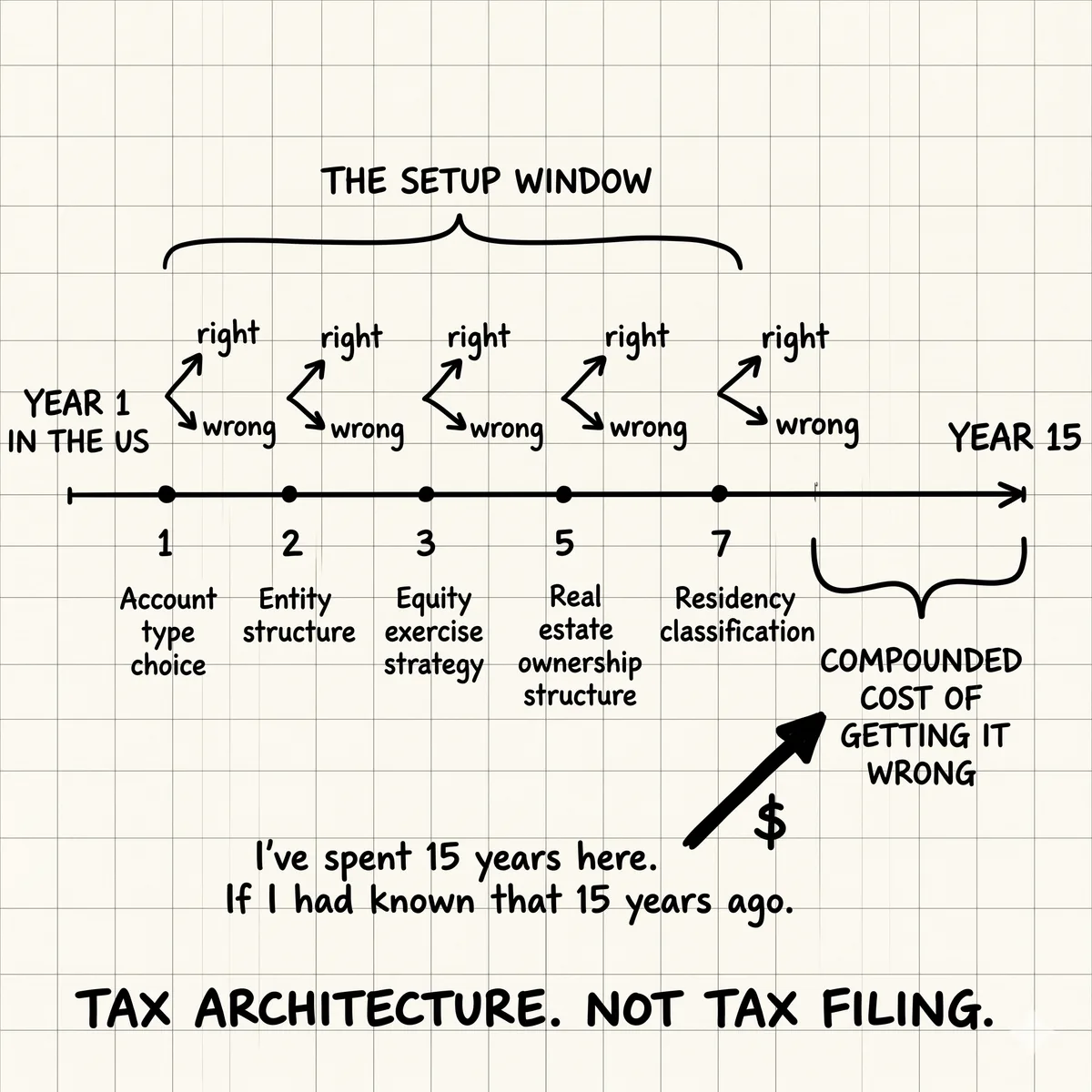

The Five Decisions Made in Years 1-5

There are five structural decisions made early in a US career that determine the tax picture for the following 20 years. Every one of them can be made well or made by default. Default is almost always more expensive.

1. Account Types and Contribution Strategy

The 401(k) enrollment decision HR presents to you is not neutral. You're choosing between traditional (pre-tax contributions, taxed on withdrawal) and Roth (after-tax contributions, tax-free withdrawal). For most people in year one of a US tech career, Roth is almost certainly better. You're not at your peak income yet. Your marginal rate now is lower than your marginal rate will be in 10-15 years. Pay tax now at 22%. Don't pay tax at 32% later on both the contribution and 20 years of growth.

The default is often traditional 401(k) because employers set it that way and the immediate tax reduction feels good. It's the wrong choice for most early-career immigrants.

The HSA is the other decision most people make by default. If your employer offers an HSA-eligible high-deductible health plan, the HSA is the triple-tax-advantaged account with no comparison. Contributions go in pre-tax, grow tax-free, and come out tax-free for qualified medical expenses. Most people in year one choose the PPO because it feels safer. The HDHP plus HSA combination is almost always better if you're young and healthy.

The compounding cost of wrong 401(k) choice over 20 years: on $20K annual contributions, getting Roth vs. traditional wrong (assuming your marginal rate rises from 22% to 32% over the period) costs roughly $180-220K in additional lifetime taxes. That's one decision.

2. Entity Structure for Side Income

Many people in year 2-3 of a US career start doing consulting work, freelance work, or building small side projects. The entity decision at that point has significant tax implications.

Sole proprietorship (the default if you do nothing) means Schedule C income. Self-employment tax (15.3%) applies on top of income tax. A single-member LLC treated as an S-Corp can allow you to pay yourself a reasonable salary and take the rest as a distribution, avoiding self-employment tax on the distribution portion. At $50K in side income, the S-Corp election can save $5,000-8,000 per year in self-employment tax.

Most people doing side consulting work don't know this option exists in year one. By year three, when they've been paying full SE tax for three years, they find out. The window to correct wasn't closed. But the money they overpaid in those early years is gone.

Wrong entity structure for $50K in consulting income over 5 years costs roughly $25,000-35,000 in unnecessary self-employment tax. That's before the compounding effect of what that money could have grown to.

3. Residency Classification for Investments

H-1B holders go through a period of being Resident Aliens for tax purposes (after passing the Substantial Presence Test) and Non-Resident Aliens before that. The classification affects how different types of income are taxed, which foreign income needs to be reported, and what treaty benefits apply.

The mistake most people make: they don't know when they crossed from NRA to RA status, so they don't know which year's income should be classified which way. Getting this wrong on the transition year can mean either overpaying or underpaying taxes and then dealing with amendments. It can also mean missing treaty benefits that apply only to NRAs.

For people with assets in India, the residency question also determines FBAR and FATCA reporting obligations. Miss an FBAR filing and the penalties are severe. File incorrectly and you've created a compliance problem. The cross-border moment covers this transition in detail.

4. Equity Exercise Strategy

For people in tech, the first equity grant often arrives in year 1-2. ISOs, NSOs, RSUs — each has a different tax treatment, and the exercise decisions made with that first grant set the pattern for everything that follows.

ISOs have an 83(b) election that must be made within 30 days of grant. Miss the window and it's gone. Most people in year one of a tech job have never heard of an 83(b) election. Their company doesn't explain it. The accountant filing last year's return doesn't mention it because there's nothing on last year's return about it.

NSO exercises trigger ordinary income in the year of exercise. Timing the exercise to a lower-income year can save 10-12 percentage points of tax. Most people exercise NSOs when they can afford to buy the shares, not when the tax picture is optimal. The difference on a $200K NSO exercise at the wrong time vs. the right time can be $20,000-25,000.

The mega backdoor Roth is another equity-adjacent decision that most people discover years too late. If your employer's 401(k) plan allows after-tax contributions with in-plan Roth conversion, that's up to $43,500 per year in additional tax-advantaged savings. Many people work at companies with this benefit for 3-4 years before anyone tells them it exists.

5. Real Estate Ownership Structure

When people buy their first home in the US, they buy it in their personal name. That's standard and usually correct. But for people with income properties or planning to own investment real estate, the ownership structure question matters early.

Holding investment property in an LLC provides liability protection. It also creates a slightly different tax treatment for depreciation deductions and can affect how the property transfers to heirs. The decision of whether to buy in personal name or in an entity should be made before the purchase, not after.

For NRIs with property in India, the question is different. Property in your name in India, once you become a US tax resident, generates rental income that must be reported on a US return. The ownership structure of that Indian property also affects the FBAR threshold calculation and the DTAA credit available.

What Nobody Tells Immigrants in Year 1

The US tax system is complex for everyone. For immigrants, it's complex plus unfamiliar. The concepts, the account types, the election windows, the treaty rules — none of it is intuitive for someone who grew up in a different tax system.

In India, the tax system has different account types, different investment vehicles, different timing conventions. The ELSS and PPF knowledge you brought from India doesn't map to US tax structures. You're starting from scratch in a system that assumes you've been here your whole life.

The CPA you hire in year one is probably focused on getting your return filed correctly. They're not sitting with you for two hours explaining the 25-year implications of your 401(k) contribution election. That's not what you hired them for.

Your employer's benefits team will enroll you in the 401(k) and explain the match. They won't explain the Roth vs. traditional tradeoff in the context of your specific income trajectory. That's not their job.

Your colleagues are useful sources of crowdsourced wisdom. But their situation is different from yours. The US citizen who grew up here doesn't have the FBAR complication, the DTAA question, the Indian property reporting issue.

The Year-1 Information Problem

The people who grow up in the US absorb this knowledge over 30 years of observation. Parents, schools, casual conversations. You arrive at 28 with a high income, an unfamiliar system, and no roadmap. The tax architecture decisions that matter most get made by default.

What the Right Year-1 Setup Looks Like

The goal isn't to be a tax expert in year one. It's to make the right structural decisions early so that the architecture you're building inside is working for you, not against you.

In the first 6 months of a US career, there are five questions worth getting answered explicitly, not by default.

- Traditional or Roth 401(k)? For most early-career immigrants, Roth. The answer depends on your current marginal rate vs. your expected rate at retirement. Get the number, not the default.

- HSA-eligible plan if offered? If you're young and healthy, almost certainly yes. Model the cost difference between the HDHP and the PPO including the HSA contribution benefit. The math usually favors the HDHP.

- When does my Substantial Presence Test clock start? Know your residency status for tax purposes and the date you crossed over. It affects which year's income gets which treatment.

- Do I have FBAR or FATCA obligations? If you have foreign accounts above $10K at any point in the year, FBAR applies. Get this right in year one. The penalties for non-filing are severe and not forgivable on ignorance grounds.

- If I start earning side income, what entity should I use?Even if you're not doing it yet, know the answer before you start. The default (Schedule C sole prop) is almost never optimal.

The HENRY tax stack is the framework for the ongoing tax optimization work at higher income levels. But the foundation is set in those early structural decisions.

The Honest Part: It's Not Too Late

Most of the decisions in years 1-5 aren't fully reversible but they're not permanently catastrophic either. Some things you can fix now even if you made them wrong then.

You can start doing backdoor Roth contributions today regardless of what you contributed in past years. The future tax-free growth starts from whenever you start.

You can make an S-Corp election for your consulting income going forward even if you were a sole proprietor for years before. The savings begin immediately.

You can do Roth conversions on existing traditional 401(k) balances during lower-income years, partially correcting the account type decision made early in your career.

You can't undo years of overpaid self-employment tax. You can't reclaim the 83(b) window that closed 10 years ago. Some decisions are past. But the architecture going forward is still being built.

What I wish someone had given me in 2009 wasn't a comprehensive tax course. It was a two-hour conversation with someone who had already been through the system and could tell me: here are the five decisions that matter most in your first two years. Here's the default option and here's the better option. Here's why.

That conversation didn't exist as a product. It still barely exists. The people who got it were lucky enough to know someone who'd already been through it. Most immigrants didn't know someone like that.

The peer knowledge problem

The US citizens who grew up here absorbed this knowledge over decades. The immigrant who arrives at 28 with a $180K salary needs the same knowledge compressed into months. It exists in peer communities, in r/personalfinance, in the H-1B groups on Facebook. But it's fragmented, often wrong, and rarely calibrated to the specific cross-border complexity that NRIs face. NettWorth is being built to make the peer knowledge that already exists accessible in a form that's actually usable.

The 2009 W-2 is a fixed number. I can't change it. But someone starting their US career today doesn't have to make the same choices by default. The information exists. The question is whether it reaches them in year one, when it matters, or in year fifteen, when it's mostly retrospective.

Tax architecture built right in years 1-5 compounds silently for two decades. Tax architecture built wrong compounds too. The decisions are the same size. The outcomes are not.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

Inherited IRA: The 10-Year Rule That Most People Get Wrong

Since the SECURE Act, most non-spouse inheritors must empty an inherited IRA within 10 years. The mistake is waiting until year 10 and taking a massive tax hit all at once. Spreading thoughtful annual withdrawals across the decade can save tens of thousands of dollars.

Liquidity Event Sequencing: Pre-Exit Tax Planning for Founders

Real exit tax savings (15-25% of proceeds) come from decisions 12-18 months before close. Master charitable structures, entity optimization, QSBS timing, and option planning.

The RNOR Window: The 2-3 Year Tax Opportunity Most NRIs Miss

Your first 2-3 years back in India, foreign income is largely tax-free. It's the window for Roth conversions and asset restructuring. Almost nobody plans for it before they leave the US.