Your FIRE Spreadsheet Doesn't Work When Your Assets Live in Three Countries

The spreadsheet made sense until it didn't. The problem wasn't the math. The problem was that the math assumed a world that doesn't exist.

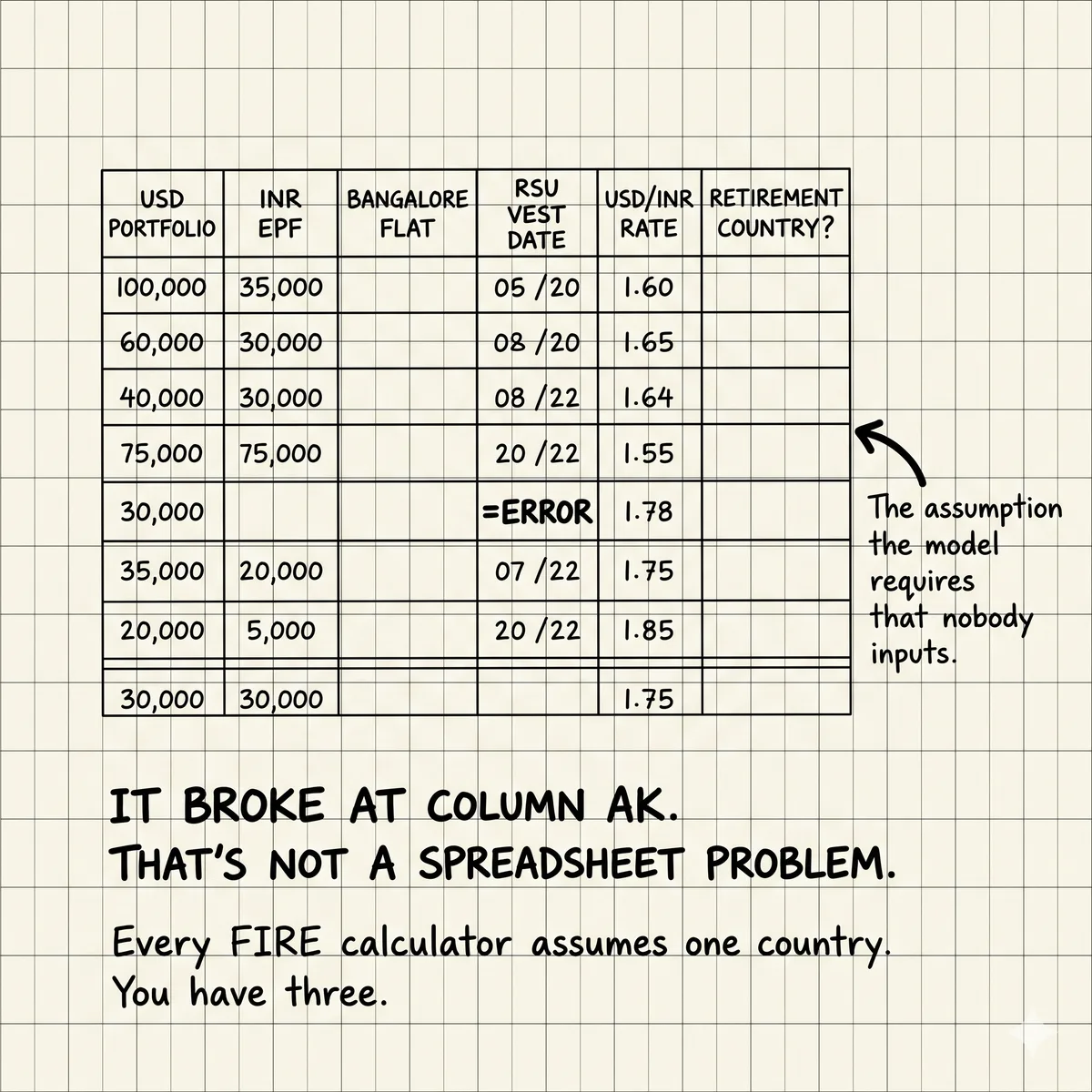

I built the spreadsheet in 2022. Two tabs. Portfolio value on the left, projected withdrawal rate on the right. 4% safe withdrawal. Expected annual return of 7%. Time horizon of 35 years. Simple, elegant, honest.

Then I added a tab for the EPF account in India. The one my employer had been contributing to for six years before I moved to the US. The one I couldn't touch without triggering Indian income tax. The one where the interest rate changes every year based on government notification. That tab didn't fit the model. I left it in a corner and kept going.

Then I added a row for the apartment in Bangalore. My parents' name is on the deed alongside mine. Its value in USD changes every time the rupee moves. Selling it would take 3-6 months, trigger Indian capital gains tax, and require a CA in Bangalore who understands NRI disposition rules.

Then the RSUs vesting in the company that might IPO in 2027. Hard to value. Hard to model. Locked out of the safe withdrawal math entirely.

Then I needed exchange rates. Which rate? The current one? A 10-year average? The one my parents actually get when they try to sell property? Each choice changed the output by 15-20%.

Then I realized I was planning to retire in two countries. Winters in India, summers here, or maybe there. Each country has different healthcare costs, different inflation rates, different tax treatment of foreign income.

The spreadsheet stopped making sense somewhere around column AK.

What FIRE Math Assumes

The standard FIRE framework is genuinely useful. The 4% rule (or 3.5% for longer horizons) is backed by real research. The safe withdrawal rate literature is some of the most rigorous personal finance work out there. Bill Bengen's original 1994 paper and the subsequent Trinity Study held up across multiple market cycles.

But the research assumes specific things. Things that aren't true for most NRIs building multi-country wealth.

- 01Single currency: All assets denominated in USD. All expenses in USD. No currency conversion friction.

- 02Single jurisdiction: US tax law applies. No foreign income. No treaty interactions. No FBAR requirements.

- 03US equities only: Historical returns are based on US stock and bond market data. Different markets have different return profiles and correlations.

- 04Linear withdrawal: You withdraw the same amount each year, adjusted for US inflation. No lumpy expenses, no currency-driven spikes.

- 05Retirement in one place: Your cost of living is determined by one geography. Not split across two countries with different inflation rates.

If you're an NRI with assets across three countries, a vesting RSU schedule, an EPF balance in India, and plans to split your retirement between geographies, exactly zero of these assumptions hold.

The Six Things That Break Standard FIRE for Multi-Country NRIs

1. EPF Rules and Withdrawal Complications

The Employee Provident Fund earns around 8-8.15% annually (rate set each year). For most NRIs, it's the highest-returning fixed-income asset in their portfolio. But you can't include it in a US safe withdrawal calculation without solving three separate problems.

First, you can only withdraw EPF under specific conditions. Leaving India for employment abroad is one valid trigger, but the process requires specific forms, NRE/NRO account routing, and often a CA who knows the rules. Second, EPF withdrawal above a certain threshold triggers TDS (Tax Deducted at Source) in India and possibly taxable income in the US, depending on your treaty position. Third, the timing of EPF withdrawal doesn't map to a clean annual withdrawal schedule. It's a one-time event with significant planning requirements.

2. DTAA Complexity on Retirement Income

The India-US Double Taxation Avoidance Agreement covers most income types but has gaps and ambiguities that become real problems in retirement. US social security benefits, IRA distributions, and investment income are each treated differently under DTAA. If you're spending time in India during retirement, the classification of your tax residency in any given year changes which country has primary taxing rights over which income.

The r/nriFIRE community has documented this problem clearly. One poster built a detailed breakdown showing that the same $80K annual withdrawal, depending on which accounts you draw from and how many days you spend in each country, could have an effective combined tax rate anywhere between 11% and 34%. That spread is too wide to ignore.

3. USD/INR Volatility as Retirement Risk

The rupee has depreciated against the dollar at roughly 3-4% per year on average over the past two decades. If your expenses in retirement are denominated in rupees but your portfolio is in dollars, this depreciation works in your favor. Your dollars buy more rupees over time.

But the direction isn't guaranteed. And the volatility is significant. The rupee moved from 83 to 87 in a three-month window in late 2024. If a meaningful portion of your retirement spending is in India, you've added a currency risk dimension that a US-centric safe withdrawal model doesn't account for. Your real spending power in India can swing 5-8% in either direction within a single year based on exchange rates alone, independent of your portfolio performance.

The currency asymmetry problem

Most NRIs mentally separate their portfolio (in USD) from their lifestyle costs (partially in INR). That separation is false. Every rupee you spend in India is a USD-to-INR conversion event. Your effective withdrawal rate isn't fixed. It fluctuates with the exchange rate. A 4% withdrawal rate in USD years could be a 2.5% or 5.5% drawdown in purchasing power terms, depending on the rupee.

4. Split-Country Lifestyle Cost Modeling

The standard FIRE model uses a single cost-of-living number. For someone planning 6 months in Bangalore and 6 months in the Bay Area, you need two cost-of-living estimates, two inflation assumptions, and a model that handles the transition costs between geographies (flights, temporary housing, re-establishment costs each time you move).

Bangalore is cheaper than the Bay Area for most lifestyle categories. But not everything. International schooling (if kids are involved), imported goods, and certain healthcare treatments can be more expensive in India. The naive model that says "I'll spend 40% less when I'm in India" isn't necessarily accurate.

5. Healthcare Cost Differences and Coverage Gaps

US healthcare in early retirement is one of the largest FIRE planning variables. If you retire before Medicare eligibility at 65, you're buying private insurance or using ACA marketplace plans. Costs run $800-2,000+ per month for a family, depending on age, location, and coverage level.

India has good quality private healthcare at a fraction of US costs. But US health insurance generally doesn't cover you in India, and Indian health insurance has its own qualification and coverage rules for NRIs. If you're splitting time between countries, you need a coverage strategy for both. The healthcare horizon post goes deeper on this specifically for pre-65 FIRE planners.

6. Property Illiquidity and Tax Complexity

The apartment in Bangalore is an asset. It's also illiquid in a way that US real estate isn't. Selling it requires NRI-specific documentation, can take months to complete, triggers Indian capital gains tax (with indexation benefits for long-held property), requires repatriation through specific channels if you want the money in the US, and may or may not be covered under DTAA for credit against US taxes.

Including it in your FIRE number as liquid capital is a mistake most people make. It's an asset. It's not cash.

The Safe Withdrawal Rate Problem

4% safe withdrawal rate assumes a US-market portfolio, a US-inflation cost structure, and a 30-year retirement horizon. Each of those assumptions adjusts for multi-country NRIs.

If your portfolio includes Indian assets (EPF, NRE FDs, Indian equities), the return profile is different. Indian equities have historically had higher returns than US equities in nominal terms but with higher volatility and political risk. Indian fixed income returns are higher in nominal terms but largely offset by rupee depreciation.

If your expenses split between India and the US, your inflation exposure splits too. Indian consumer inflation runs 4-6% currently. US CPI runs 2.5-3.5%. Your blended inflation rate depends on what percentage of expenses are in each country.

The geography arbitrage argument cuts both ways. Yes, living part of the year in India reduces your absolute spending. But it also means your effective withdrawal rate is being calculated against a portfolio that carries currency, political, and market risks not captured in the standard safe withdrawal rate research. The geography arbitrage post covers the cost-of-living modeling in detail.

The Core Problem

4% in the US isn't 4% in India. And 4% of a three-country portfolio with correlated currency risk and illiquid real estate isn't 4% of a US brokerage account. The number that looks the same on paper has fundamentally different risk properties.

What a Real Multi-Country FIRE Plan Needs to Model

The r/nriFIRE thread that sparked this post asked: "Agentic approach to FIRE planning instead of spreadsheets?" The person had USD/INR/THB assets, RSU vesting schedules, and was trying to model safe withdrawal across multiple countries. 43 comments. Most of them agreed the spreadsheet approach was breaking down.

Here's what a real multi-country FIRE plan needs to model that standard tools don't handle:

- Asset liquidity classification: Which assets are truly liquid vs. locked (EPF, deferred comp, unvested RSUs, real estate). Your "net worth" and your "retirement corpus" are different numbers.

- Currency scenario modeling: What does the plan look like if USD/INR goes to 90 over the next 5 years? What about 100? What about a reversal to 75? The plan should have explicit scenarios, not one exchange rate assumption.

- Tax jurisdiction optimization by year: In retirement, your tax residency in any given year may be discretionary. A plan that optimizes which country you're tax-resident in during high-income years vs. low-income years can save tens of thousands of dollars annually.

- Healthcare cost modeling for two countries: Separate projections for US and India healthcare costs, with explicit coverage gap analysis for the years between early retirement and Medicare eligibility.

- Lumpy withdrawal events: EPF liquidation, Indian property sale, and equity vesting events don't fit into smooth annual withdrawal models. They need event-driven modeling.

- Estate planning across jurisdictions: Indian inheritance law, US estate tax thresholds, and property succession rules interact in ways that require specific planning if you have significant assets in both countries.

Why Spreadsheets Fail

Spreadsheets fail multi-country FIRE planning for a structural reason. They model inputs. They don't model correlations.

The relationship between USD/INR exchange rate and your Indian stock portfolio returns and Indian inflation and the cost of your Bangalore apartment and your DTAA tax position is not a series of independent variables. They're correlated. A global risk event that weakens the rupee also typically weakens Indian equities and increases the cost of imported goods in India, while simultaneously affecting your US portfolio.

A spreadsheet treats each variable as a row. It can't capture the scenario where multiple variables move together in a correlated risk event. That's exactly the kind of scenario that breaks FIRE plans.

The model you need isn't a spreadsheet. It's a simulation that understands the correlation structure of your multi-country asset base and runs scenarios with correlated risk factors.

What this means practically

The first step isn't building a better spreadsheet. It's a clean accounting of what you actually have: which assets are in which currencies, which ones are truly liquid, what the tax treatment is on each one if you touch it in retirement, and what a realistic split-country lifestyle actually costs. Most people haven't done that inventory honestly. Until you have, any withdrawal rate calculation is built on assumptions that haven't been stress-tested.

The column AK moment isn't failure. It's the spreadsheet being honest with you. Your financial situation is more complex than a single-currency, single-jurisdiction tool can model. The right response isn't to force the complexity into the wrong tool. It's to use the right model.

NettWorth's multi-country modeling handles the currency scenarios, the liquidity classification, and the DTAA interactions that standard FIRE tools assume away. The goal isn't a prettier spreadsheet. It's an honest answer to whether you can actually afford to stop.

The cross-border moment changes your tax structure. It also changes your retirement math. Run the right model.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

You Can't Share This With Anyone Who Won't Make It Weird

You typed the text. Then deleted it. The people who most need peer context are the ones most isolated from it — family has baggage, friends have context mismatch, advisors have incentive misalignment. This is the problem NettWorth was built to solve.

AI Knows the Market. It Doesn't Know You.

Every Davos panel is a purchased narrative. AI amplifies those narratives. But the S&P hitting new highs tells you nothing about whether you should sell your RSUs or refi your mortgage.

You're Probably Planning for the Wrong Retirement Country

If you assume India but stay in the US (or vice versa), every number in your retirement plan is wrong. The most important assumption in your plan is unspoken.