Geography Arbitrage

A motion to vote on California's billionaire tax triggered the exodus. Larry Page, David Sacks and others are moving now—because their lawyers told them to. You don't have an army of lawyers. You need a different timeline.

January 2026 hit and the headlines exploded.

California's motion to vote on a wealth tax targeting billionaires. Suddenly, Elon's moving to Texas. Bezos to Miami. The exodus is real. The urgency is real.

And here's what I realized while watching the announcements roll out: Billionaires can move fast because they have suites of lawyers and accountants on speed dial. They can restructure domiciles, update documentation, and move assets in weeks.

But you can't.

If you're watching this unfold and thinking "maybe I should move too," you're 6-12 months too late to do it properly.

Why Billionaires Move Fast (And You Can't)

Here's what separates billionaires from HENRYs: resources. When a tax motion hits the table, Elon can hire three tax firms, two estate planning firms, and a litigation team to restructure his entire tax footprint in 6-8 weeks. He has that capacity.

You don't.

Residency changes aren't quick. They require 6-12 months of deliberate preparation before you can lock in a new tax status. Which means if you're watching Elon move and thinking "I should do that too," you're already months behind schedule.

The Real Numbers

The math is straightforward.

California's Millionaires Tax. 13.3% state income tax on top of federal rates. It doesn't matter if you're making $400K or $40M—that rate doesn't change. Apply that across a $10M gain in capital appreciation, and you're talking $1.33M in pure state tax.

Texas? Zero state income tax. Florida? Zero state income tax. Nevada? Zero.

The savings aren't abstract. We're talking north of $1M a year in ongoing tax reduction if you're generating real income. For someone like Elon or Bezos, with massive capital gains and income events, the multi-year savings are tens of millions.

But here's where most people get it wrong.

They think the move is the announcement. "Oh, I'll move to Texas and save on taxes." So they look at houses in Austin, maybe buy one, keep paying California income tax on California business income, and then wonder why their tax bill didn't change.

That's not how residency works.

What Actually Determines Residency

Residency is intent plus documentation plus presence.

Primary Residence (Days Test)

Where you spend the most days. If you spent 200 days in California and 165 days in Texas, California is your primary residence—even if your house is in Texas. The IRS has sophisticated tools for tracking this (credit card usage, cell phone records, social media check-ins).

Documentation

- Driver's license (which state?)

- Voter registration (which state?)

- Property deeds (where's your real estate?)

- Business registration (where's your company incorporated?)

- Bank accounts and investment accounts (where are they domiciled?)

These create a paper trail. Change them consistently, and you've established intent. Leave them inconsistent, and you've created an audit flag.

Community Ties

- Where do you vote (or intend to vote)?

- Where are your kids' schools?

- Where are your business interests?

- Where do you maintain social/family ties?

The IRS isn't looking for perfection. They're looking for consistency. Does everything point toward Florida, or does the evidence get confusing?

The Trust Location Problem

Here's the thing most people miss: Residency affects you, but what about your trust?

If you have a revocable living trust that's situs (domiciled) in California, and you move to Texas, does the trust move with you?

Technically, trusts don't have citizenship. But their situs matters for tax purposes.

If your trust is California-situs and you become Florida-resident, you've created a mismatch. The trust might still be taxed by California. Your personal income is taxed by Florida. You've introduced complexity without solving the actual problem.

The real move requires:

- Personal domicile change (driver's license, voter registration, primary residence in new state)

- Trust domicile change (retitle the trust assets, update the trust itself, potentially create a new trust in the new state)

- Asset location alignment (make sure trust assets are in the new state, or at least not creating California exposure)

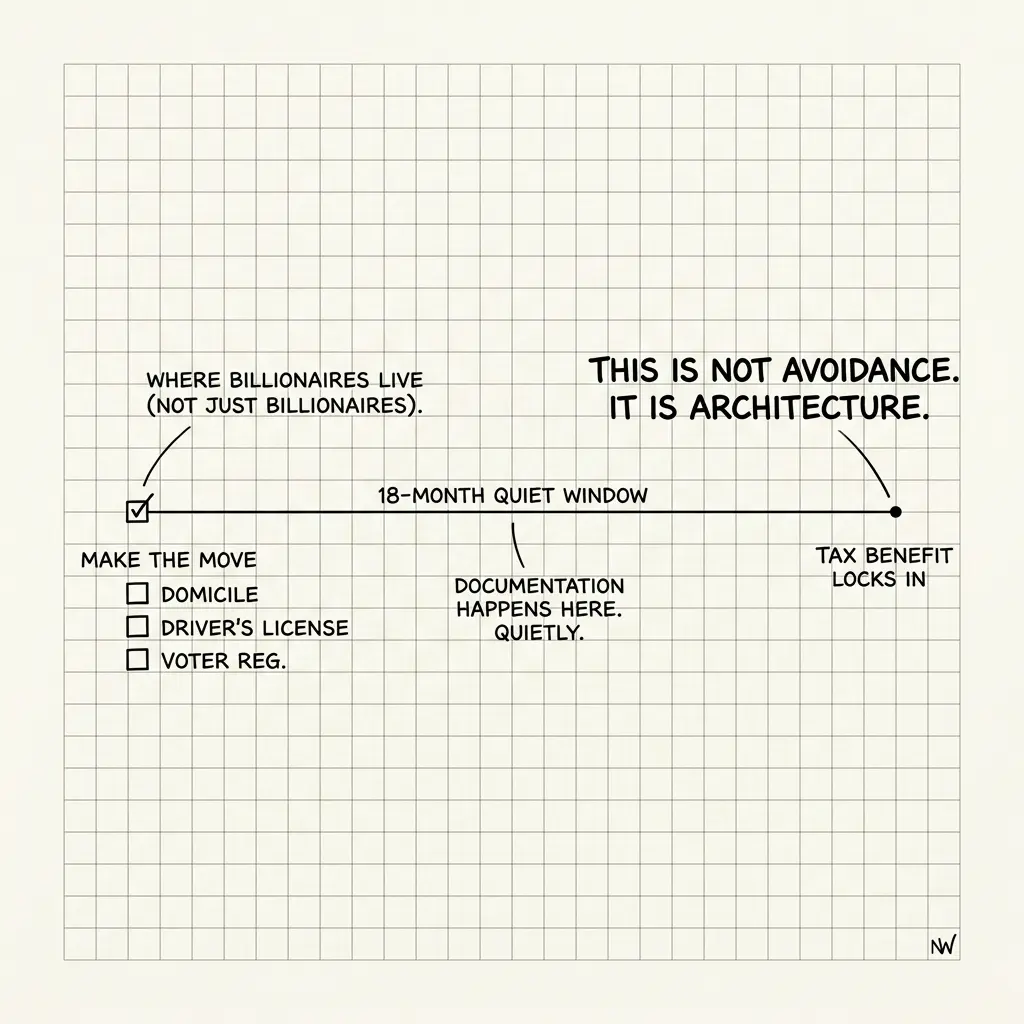

This takes 18 months because:

- Month 1-6: Establishing personal residency (documentation, presence, intent)

- Month 6-12: Moving trust assets and updating trust location

- Month 12-18: Getting consistent documentation from banks, accountants, etc.

Miss this window and you're locked into your old state's tax treatment for years.

The Planning Timeline You Actually Need

Elon watches a tax motion, calls his lawyers, and moves. He has six weeks of lawyer time to burn and the computational power of a war room behind him.

You need 6-12 months of preparation before you can move and actually lock in the tax treatment.

Which means if you're reading this in January 2026 and thinking "I should move to Texas," you're not moving in 2026. You're planning for 2027.

The actual 18-month timeline:

Months 1-3 (Decision Phase)

- Decide on new state

- Research actual tax impact (not headlines, actual numbers)

- Understand documentation requirements

- Identify which assets need to move with you

Months 4-9 (Setup Phase)

- Update driver's license in new state

- Update voter registration

- Begin property transfers (if relevant)

- Start spending significant time in new state (establish presence)

- Update business location (if relevant)

Months 10-15 (Consolidation Phase)

- Move bank accounts/investment accounts

- Update trust domicile (if you have a trust)

- Consolidate assets to new state

- Ensure 183-day presence threshold is met

Months 16-18 (Documentation Phase)

- Get consistent documentation from banks, accountant, lawyer

- Update all remaining inconsistencies

- File taxes claiming new residency

- Document intent for IRS

Month 18+: Locked In

- Your residency status for the previous 18 months is now established

- Tax treatment is retroactive to when you moved domicile

- You're committed to maintaining the move (changing back creates new complications)

The HENRY Disadvantage

Here's the hardest truth: You cannot move like a billionaire moves. You don't have the lawyer budget, the accountant availability, or the legal infrastructure. What takes Elon six weeks takes you six months.

Which means the moment a tax threat emerges, you're already behind schedule.

If you want to actually execute a geography move—if you want to change residency legitimately and lock in tax treatment—you need to have started the process months before the pressure arrives.

You need to plan your domicile shift 6-12 months before anybody famous announces they're leaving.

Elon didn't decide to leave because of the January 2026 motion. His lawyers told him to move because they'd already seen this coming, and a proactive reposition in late 2025 was the only way to lock in favorable treatment for the transition.

The lesson for HENRYs isn't "follow Elon's lead." It's "plan like Elon's lawyers plan." Which means thinking about residency changes 12-18 months before they become necessary.

If you're watching the billionaire exodus and thinking "I should move too," that's the emotional instinct. But the smart move is already behind schedule for this year. Start planning for 2027.

External References

- IRS Residency Rules — Official guidance on domicile and residency definitions

- California Franchise Tax Board Billionaire Tax — Current CA tax rates and residency rules

- NCCUSL Uniform Act on Domicile — Legal standards for determining tax domicile

- Kiplinger State Tax Rates — Current state-by-state tax comparisons

Related Reading

For context on how residency planning fits your broader tax strategy:

- The Cross-Border Moment — International tax complexity (same principles, higher stakes)

- The HENRY Tax Stack — How residency decisions affect your full-year tax sequencing

- The Complexity Tax — How multi-state complexity multiplies costs (and why consolidation matters)

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

Should I Pay Off My Mortgage With an Inheritance?

There is no universal right answer, but there is a framework. The psychological value of no mortgage payment is real and doesn't show up in any spreadsheet. And there's a third option — partial paydown — that most people don't consider.

Concentrated Tech Equity: The Diversification Decision (With Math)

Your advisor says diversify. But diversification has a real cost. Here is the math on when holding wins, when selling wins, and what wealthy founders actually do.

The Expat Financial Checklist: What Mid-Senior Professionals Get Wrong Before They Relocate

Everyone checks the cost-of-living calculator and the school ratings. Almost nobody reviews the financial decisions that need to be made before they leave — the ones with hard deadlines that disappear when the moving truck arrives.