H1B Homebuying: The 20-Year Math Nobody Runs

In 2016, Raj showed me a Zillow listing on his phone. $450K. Nice street in Sunnyvale. He wanted it. You could see it in his face. Then he put his phone down and said "not yet, still on H1B." I didn't say anything.

That was eight years ago.

Last spring, I went to his place for dinner. Same rental. Same landlord. The neighbor's house had just sold for $648K. The house two doors down sold for $612K. The whole street had moved up $180K to $200K while he watched.

He talked about buying like he always does. "Once the green card comes through." His voice sounded confident. His body didn't. He refilled glasses, changed the subject. He's been saying "once the green card comes through" since Obama's second term.

I don't blame him. The advice he got in 2016 was probably right for 2016. Don't buy on H1B. Too risky. What if you get laid off? What if visa gets denied? What if you have to go back?

The problem is that advice was never recalculated. Nobody ran the 20-year math. They just repeated the rule.

The rule isn't wrong. But the math behind the rule is more complicated than most people admit.

Why Standard Homebuying Math Breaks for H1B Holders

When a citizen buys a house, the math is roughly: purchase price, down payment, monthly cost vs. rent, appreciation, build equity over 30 years, retire with a paid-off asset. Simple frame. Works well.

When an H1B holder buys a house, there's a variable that frame ignores: the probability of forced exit.

Forced exit isn't just deportation. It's layoff combined with the 60-day grace period. It's visa denial at the renewal. It's the EB-2 India priority date slipping again and the attorney saying "we're looking at 2031 now." It's the policy change nobody saw coming. It's the company getting acquired and the new entity not sponsoring visas.

Any of these events, in the wrong year, turns a home from an asset into a fire sale.

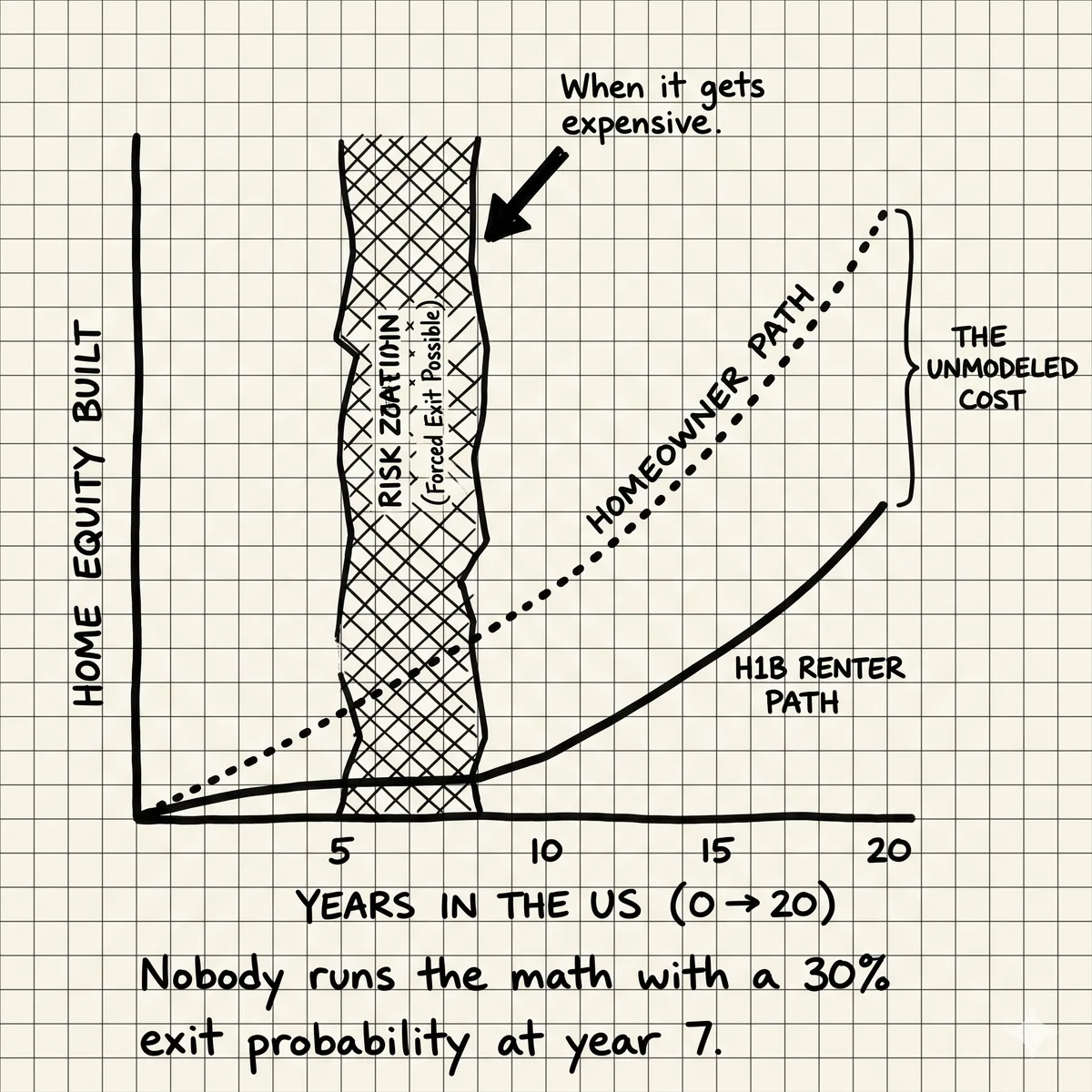

The problem isn't risk. It's timing.

The years when forced exit risk is highest (years 5-9 on H1B, while the green card is in process) are also the years when a home purchase has the lowest equity and the highest transaction cost exposure. You're most at risk right when selling would hurt the most.

If you buy in year 1 of H1B and sell in year 6 under duress, here's what happens to a $500K home purchase:

- 6% realtor commission: $30K gone immediately

- Years 1-3 of a 30-year mortgage are almost entirely interest (minimal equity built)

- If the market is flat or down even 5%, you're underwater on transaction costs alone

- If you have to sell quickly, you lose negotiating power and typically land 3-8% below market

In a forced sale at year 6, it's not unusual to walk away with less cash than you put in. That's not a mortgage. That's an expensive rental with extra paperwork.

The 5-7 Year Problem

The EB-2 India backlog is measured in decades. The EB-3 India backlog is also measured in decades. If you're Indian, on H1B, and relying on employer-sponsored GC, your realistic timeline from H1B filing to green card approval is 15 to 25 years for most people in the queue right now.

That means years 5, 6, 7, 8, 9 on H1B are not "getting close to the green card" years. They're mid-process years. The I-485 isn't filed. The priority date isn't current. You're fully dependent on your employer's willingness to keep sponsoring.

And this is exactly when the forced-exit scenarios are most dangerous:

- The employer has started the GC process but can revoke it with layoffs

- The 60-day grace period after layoff is real and short

- A new employer means restarting parts of the process

- Policy changes (and there have been several) can freeze processing or change rules mid-stream

For EB-1 holders or people with older priority dates, this calculus is different. For the median Indian tech worker on H1B, years 5-7 are the years of maximum immigration uncertainty. They're also the years when, if you bought in year 1, your equity is still thin and your exit costs are still brutal.

That's not a coincidence. That's the trap.

The Real Numbers: A Worked Example

Let's model it. $500K home in the Bay Area, 2024 purchase. 20% down ($100K). 30-year mortgage at 7.2% (current rates). 7-year horizon. 30% probability of forced relocation by year 7.

Scenario A: You stay 7 years, no forced exit

- Home appreciates at 4% annually: $500K becomes ~$657K

- Equity built in 7 years at 7.2%: approximately $48K principal paid

- Total equity at sale (unrealized): ~$205K ($657K - $400K mortgage - closing costs ~$52K)

- Net gain vs. $100K down: approximately $105K over 7 years

- Rental comparison: $3,200/month rent for equivalent = $268K over 7 years

- Mortgage P&I + taxes + insurance (PITI): approximately $4,100/month = $344K over 7 years

- Owning cost premium over renting: $76K. Net of equity gain: negative $29K vs. renting.

At 4% appreciation, 7-year hold, owning barely beats renting on a pure cost basis even in a best-case scenario.

Scenario B: Forced exit at year 7 (the 30% probability event)

- Same home, now worth $657K

- Forced sale with 60-day timeline: you accept $625K (5% discount for speed)

- Realtor fees: $37.5K

- Remaining mortgage: $452K

- Net proceeds: $135.5K

- You put in $100K down plus 7 years of owning premium over rent (~$76K) = $176K total

- Net financial outcome vs. renting and investing: negative $40K+

The forced exit scenario destroys value vs. renting and investing the difference.

Blended expected value (70% stay, 30% forced exit)

- 70% × (-$29K) = -$20.3K

- 30% × (-$40K) = -$12K

- Expected value of buying vs. renting: negative $32K over 7 years

This flips at higher appreciation rates (5-6%+) or longer hold periods (10+ years). But the standard advice doesn't run this model. It just says "buy if you can."

This math changes significantly if you have an O-1 visa, an EB-1A in process, or a priority date that's actually current. The forced exit probability drops dramatically. The 30% assumption is for the median Indian tech worker on H1B with EB-2/EB-3 sponsorship in the standard queue.

What Changes the Math

The calculation above assumes you're renting and investing the difference. That's the comparison that matters. The $100K down payment invested in a diversified index fund at 8% annual return over 7 years becomes $171K. Your $1,100/month owning premium over rent, invested monthly over 7 years at 8%, is another $116K.

That's $287K in liquid, portable capital vs. $135K in locked-up equity with a forced-sale discount and transaction costs baked in.

The variables that flip this to favor buying:

- Appreciation rate above 5% annually. At 6% annual appreciation, the math tilts toward buying even with the forced-exit probability. Bay Area has historically delivered this, but past performance and all that.

- 10+ year horizon. The longer you hold, the more transaction costs get amortized, equity compounds, and the forced-exit risk (as a percentage of total hold) decreases.

- Low forced-exit probability. If you have a realistic path to green card in 3-4 years, your 30% becomes 10%. The math changes.

- Rent vs. buy gap in your market. In some markets, rent is so high relative to purchase price that owning actually saves money monthly. This changes the breakeven.

The honest answer nobody gives you

The right question isn't "should I buy on H1B?" It's "what is my realistic forced-exit probability at year 5-8, and what does my market's appreciation rate have to be for buying to beat renting-and-investing over my actual horizon?"

For most Indian tech workers in the EB-2/EB-3 queue with 10+ years to green card, buying in years 1-3 of H1B is a worse financial decision than renting and investing the difference, unless you're in a market with 5%+ annual appreciation and you're confident you won't need to sell under duress.

What Your Peer Cohort Actually Does

Here's the pattern from people who've been through this decision. Not a survey. Not data. Conversations.

The people who bought early (years 1-3 of H1B) and stayed fall into two camps. The ones who got lucky on appreciation (Bay Area 2012-2019, for example) made out well. They'll tell you to buy. The ones who got unlucky on timing or got laid off tell a different story. They usually don't bring it up.

The people who waited until GC approval are split too. Some waited 12 years, watched appreciation leave them behind, and are now buying in their late 30s with more financial capital but also more life complexity (kids in school, aging parents, job changes). They bought at higher prices but with no forced-exit risk.

The third group is the one nobody talks about: people who did the math, decided renting made more sense given their specific immigration timeline and market, invested the difference deliberately, and ended up with more liquid wealth than the buyers in their cohort. Not because they got lucky. Because they ran the actual numbers.

Raj is in the second group, sort of. He kept waiting without making an active decision. The difference between "waiting strategically" and "perpetually deferring" is whether you ran the math or just kept saying "not yet."

If you want to understand what people in your actual situation, with your actual immigration timeline and your actual market, decided and how it turned out, that's the kind of peer benchmark that actually helps. The cross-border complexity moment usually arrives when the decision has already been made. Running the math before that moment is the whole game.

The Framework (Run This Before You Decide)

Four inputs. That's all you need to know whether buying makes sense for you.

- Your realistic forced-exit probability at years 5-8. Not worst-case. Not best-case. Realistic, given your employer's track record, your visa type, your priority date, and current policy environment.

- Your market's historical appreciation rate. Not national average. Your specific metro. The last 10 years, not just the last 3.

- The rent vs. own monthly delta in your specific market. What does the equivalent rental cost vs. what does PITI cost on the home you'd buy?

- Your actual holding horizon. Not "until green card someday." If green card comes in 15 years and you're buying now, you have a 15-year horizon minimum if you're planning to stay. If you're planning to return to India in 8 years regardless of green card status, your horizon is 8 years.

Run those four inputs through the model. The answer isn't always "don't buy." Sometimes it's clearly "buy now." But the answer should come from the math, not from the rule.

The tax implications of a forced early sale also matter here. If you sell a primary residence within 2 years, you don't get the $250K/$500K capital gains exclusion. That's another variable most people ignore until it's too late. And if you're selling in a year when you're also transitioning visa status, the 180-day window and tax residency status can add another layer of complexity to what should be a simple transaction.

Raj's dinner was fine. The food was good. He's doing well. But when I left, I kept thinking about what he said about the listing he'd seen that week. "Not yet." Same words, eight years later.

The math on "not yet" has changed. The green card timeline has changed. His equity situation has changed. His career stability has changed. His parents' situation in India has changed. But the decision frame is still the same one from 2016. Nobody updated it.

The most expensive financial decisions aren't the ones made wrong. They're the ones never made at all.

NettWorth

Wondering how to act on the insights in the article? Click here to apply this framework to your own wealth portfolio.

NettWorth reads your actual documents and applies what you just learned to your specific accounts, balances, and timeline — not a hypothetical.

No charge if you cancel. Your data stays yours.

Continue Reading

How to Actually Invest an Inheritance (Without a Finance Degree)

Low-cost index funds outperform most actively managed alternatives over any 15-year period. The three-fund portfolio and target-date funds are not cop-outs — they are the approach most economists would actually use. Here's the jargon-free version.

Smart Debt at Scale

When you own $3M in paid-off assets, borrowing at 2.8% beats liquidating appreciated stock. Here's the math that changes the conversation about debt.

Concentrated Tech Equity: The Diversification Decision (With Math)

Your advisor says diversify. But diversification has a real cost. Here is the math on when holding wins, when selling wins, and what wealthy founders actually do.